This article was first posted in Outperforming the Market on May 21, 2023.

I will show in this article that Alibaba stock (NYSE:BABA) is trading at a significant discount to its SOTP valuation today, and that this discount does not seem to reflect reality. In reality, Alibaba is executing well on two fronts: Its business re-organization plan that will enhance shareholder value, as well as its initiatives to reduce costs and improve operating efficiencies of its businesses.

For members of Outperforming the Market, if you have not read my deep dive into Alibaba, I encourage you to do so here. I have also written other articles on Alibaba on Seeking Alpha, which can be found here.

Alibaba’s recent FY4Q23 quarter

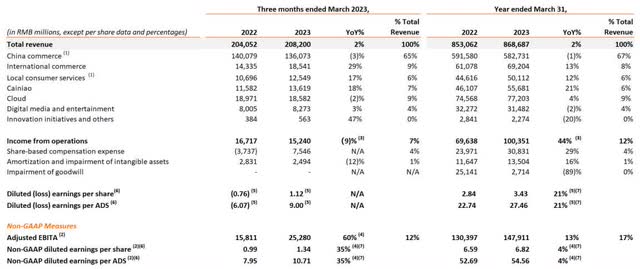

Alibaba’s FY4Q23 revenue was up 2% year on year, largely in-line with consensus of Rmb 209 billion.

In terms of revenue breakdown, China retail revenues, which makes up 65% of revenues, was down 3% to Rmb 132 billion, of which customer management revenues were down 5% year on year to Rmb 60 billion. The two other largest segments, international commerce and cloud segments, both of which make up 9% of total revenues, grew 29% and -2% respectively year on year. Cainiao and local consumer services segment, which makes up 7% and 6% of revenue mix respectively, grew 18% and 17% respectively.

Summary of Alibaba Mar Quarter (Alibaba IR)

Non-GAAP net income to ordinary shareholders was up 30% year on year to Rmb 28 billion, beating market consensus of Rmb 24.6 billion by 14%.

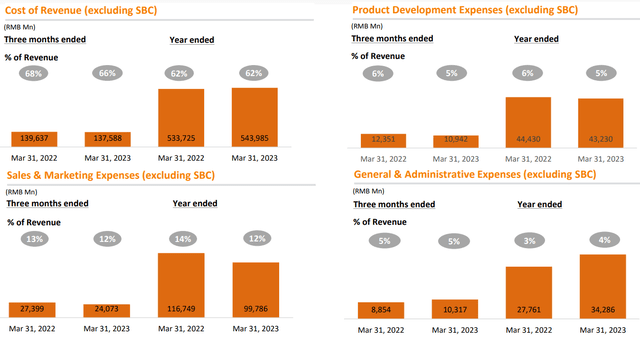

This was driven by improvements in gross profit margins, lower spend on R&D and sales & marketing. Cost of revenue fell to 66%, from 68% in the prior year, while product development expenses and sales and marketing expenses both fell by one percentage point.

Alibaba Mar Quarter cost metrics (Alibaba IR)

Adjusted EPS came in at $10.71, beating the market consensus of $9.44 by 13%.

Specifically, in the quarter, there was an improvement in the adjusted EBITA of China commerce while the local consumer services, international commerce and digital media and entertainment businesses narrowed adjusted EBITA losses. For the China commerce segment, EBITA margin expanded from 22.9% from the prior year to 28% in the current quarter. At the same time, international commerce saw EBITA margin improve to -13% in the quarter, from -18% from the prior year. The local consumer services segment also saw an improvement in EBITA loss margin to -33%, an improvement from the -53% from the prior year and Cainiao saw EBITA margin improve to -2% in the current quarter, an improvement from -8% in the prior year.

My thoughts on the quarter

I think that while overall revenue growth was soft at 2% growth year on year, the improvements we have seen in the profitability of each individual segment is commendable. It has significantly reduced costs through the year.

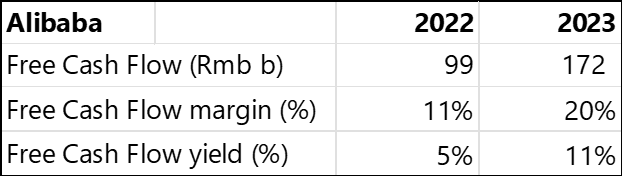

Just to highlight this: Free cash flow for FY2022 fiscal was Rmb 98.9 billion, which translated to 11% free cash flow margin. However, in FY2023, free cash flow increased 74% to Rmb 171.6 billion, and free cash flow margin improved to 20% for FY2023.

Alibaba Free Cash Flows (Author generated)

Focus on user growth in China commerce segment

Management commented that the business saw improvements in March and April, when users and GMV on the Taobao app achieved a positive growth year on year. This was driven by improvements in the recovery in the macro environment in China, the reaping of benefits of its cost optimization and efficiency enhancement initiatives, and the core strategy to put the emphasis on the user and build a strong ecosystem.

In the next three to five years, management’s focus will be on user growth and retention and to establish a strong ecosystem while continuing to drive innovation and increase the time a user spends on its platforms.

Ultimately, management’s key goal is to ensure that Taobao remains the number one consumption platform in China, serving the largest number of customers in the country while evolving with the different demands and needs of users over time.

Solid growth path for international commerce

In the recent quarter, we saw international commerce revenue grow 29% year on year while the order volume also grew 15% year on year.

Despite a challenging year, management stated that the international commerce segment business has recovered and is on a growth trajectory.

The focus in the near-term will be to invest in its cross-border plus local commerce model in the B2C retail sector. With the recent launch of the CHOICE service, management has seen improvements in the AliExpress user experience.

Alibaba committed to continue its investments in the Southeast Asia market while looking for additional opportunities in other regional markets for its local commerce business.

All in all, I think management remains focused on improvements in operating efficiencies while continuing to grow the business.

AliCloud

In the quarter, revenues from cloud computing were down 2% year on year, to Rmb 18.6 billion. This was a result of proactive measures that were taken to adjust its revenue structure, focus on high quality growth, and continuing declines in revenue from its top customer in its international business. It was stated on the earnings call that the revenue contribution from this particular customer, fell by 41% year on year.

For the adjusted EBITA of the cloud computing business, this was up 39% year on year and came in at an adjusted EBITA margin of 2%.

In the recent earnings call, management highlighted that its price reduction strategy has gathered strong interest from customers. Earlier, Alibaba Cloud announced that it was reducing the price of some of its core products by 15% to 50%, which was the largest price cut in its operational history. Management highlighted this was to attract interest from smaller and medium sized enterprises and to make computing power more accessible to them.

Despite different players entering the space, management believes that AliCloud will be able to retain its leading position. The main focus for AliCloud will be in the public cloud, AliCloud’s public cloud revenue contribution is much higher than its competitors.

With the recent talk about opportunities in AI, this brings a large market potential to Alibaba. The rise and increasing use of AI, LLM and other vertical models mean that AliCloud will be able to support the training of these models. In addition, AliCloud is looking to build a model-as-a-service (“MaaS”) on top of its IaaS and PaaS offerings.

When asked about long-term profitability, management believes that because AliCloud is still in its early days of development and has a long path ahead, there is room for AliCloud to grow its scale, and along the way, improve its economies and margins.

Local consumer services narrowing losses

Lastly, for its local consumer services segment, revenue growth was strong at 17% year on year due to strong GMV growth in Ele.me as a result of higher average order value.

The adjusted EBITA loss in the segment was due to the Ele.me business as the business saw improvements in unit economics per order as a result of lower delivery cost per order and higher average order value.

The unit economics for the local consumer services segment improved year on year and was positive in the quarter.

Re-organization plans

Cloud Intelligence Group

The Board of Alibaba approved the full spin-off of the Cloud Intelligence Group as part of its re-organization plan.

Management views the Cloud Intelligence Group’s business model, customer profile and stage of development fundamentally different from Alibaba’s ecosystem as most of their businesses are customer-focused businesses.

The spin-off of the Cloud Intelligence Group will be done via a stock dividend distribution to shareholders and pending the required approvals, is targeted to complete within the next 12 months.

External capital raising for International Digital Commerce Group

The Board also provided its approval of a process to explore external capital raising for Alibaba International Digital Commerce Group.

External Capital Raising for Alibaba International Digital Commerce Group – The board of directors approved the commencement of a process to explore raising external capital for the Alibaba International Digital Commerce Group to support its development and growth.

IPO of Freshippo and Cainiao

Management expects to execute the initial public offering of Freshippo and Cainiao, given that the Board has approved this.

These are the two businesses with management thinks has established a differentiated offering over time and has a visible path towards profitability.

The company expects that the initial public offering will be completed in the next 12 to 18 months for Cainiao and in the next six to 12 months for Freshippo.

Capital management plan

After the re-organization, Alibaba will have the primary role of a holding company with the duties of capital management. As a result, Alibaba has established a capital management committee to enhance shareholder return and oversee the capital management matters at the group level.

There are three priorities that management highlighted as their key framework for the capital allocation strategy:

- The focus will be on improving the return on invested capital in managing the assets of the company, given that Tmall and Taobao will continue to be 100% owned by Alibaba and its main source of funds.

- In addition, Alibaba looks to commit to execute activities that are EPS accretive and will execute on its $17 billion unutilized amount in its share repurchase program.

- Lastly, all options to enhance shareholder return will be explored by unlocking the value of its assets and then returning them to shareholders.

Valuation

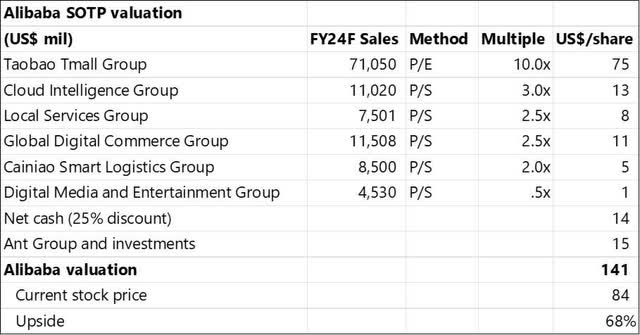

I created the following sum-of-the-parts (“SOTP”) valuation model for Alibaba. I have previously created an SOTP valuation for Alibaba in my earlier deep dive, which can be found here.

I would first note that the multiples I have applied are relatively conservative compared to that found in the deep dive, so the valuation of each Group has already been discounted conservatively to match the current market environment.

For most of its businesses, I applied a P/S multiple to my forecast of their FY2024F sales to derive their value. In addition, I assumed Ant Financial to be valued at $50 billion, which is lower than their recent $64 billion valuation by Fidelity.

As can be seen below, Alibaba’s SOTP valuation shows that the shares are worth $141 per share, implying a 68% upside from current stock prices. As I would highlight, my numbers and forecasts are meant to be conservative and as a result, there may be upside to these numbers on multiple fronts.

Alibaba SOTP valuation (Author generated)

Conclusion

All in all, I like that management is executing well on two things.

Firstly, it has executed well on its plans to cut costs and improve efficiencies from a year ago. I don’t think that the capital markets are rewarding Alibaba enough for these efforts today given the company is currently trading at 11% free cash flow yields.

Secondly, the company is executing well on its plans to be an allocator of capital and re-organize its business. Eventually, Alibaba will be able to be a holding company and with the re-organization plan, the company can then unlock its true value of its assets. What amazes me is the speed and steadfast execution of management on this front as Alibaba has been focused on its efforts to re-organize its company and enhance shareholder value.

At the end of the day, while the management team is executing well on its plans, the real opportunity relates to where the share price is trading relative to its true value. As shown in the SOTP valuation I have created, I think that the company is significantly undervalued, with an upside potential of 68% from current levels. I think that this significant discount to the SOTP valuation is not justified given the improvements in operating efficiencies and margins of its businesses, as well as its solid execution on its business re-organization plans.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here