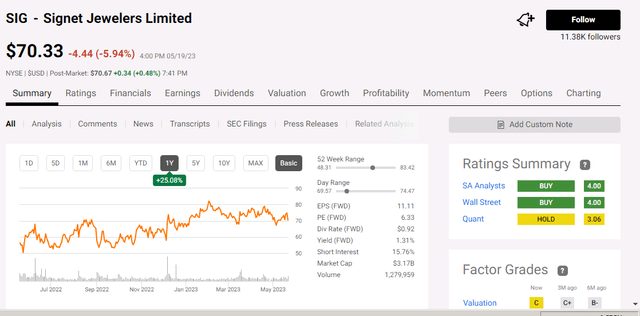

American leading specialty jewelry retailer Signet Jewelers’ (NYSE:SIG) stock is up 25% over the past year but still looks cheap with a forward P/E of less than 7.

Seeking Alpha

Although management’s efforts to grow market share could gain traction, sector headwinds owing to delayed relationship formation during the pandemic (which would take a few years to recover), a possible recession, and their relatively price-sensitive customer base make for a relatively unfavorable risk reward at this time.

Q4 2023 performance

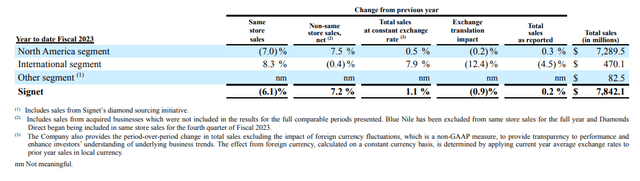

Signet Jewelers saw sales drop 5.2% YoY to USD 2.7 billion in Q4 2023 (quarter ended January 2023) a relatively soft performance during what is seasonally a busy quarter, partly driven by winter storm Elliott occurring during the peak selling period before Christmas (which caused almost a third of stores to close or operate at reduced hours), inflationary pressures (which led to consumers cutting back on discretionary purchases), as well as difficult comps (sales were up 28% YoY during the same quarter last year having benefited from a surge in consumer spending partly driven by government benefit programs). After two years of sales growth in jewelry sales during the holiday season, jewelry sales fell 5.4% during the 2022 holiday season according to data from MasterCard SpendingPulse. GAAP gross margin improved to 41.7% in Q4 2023, 70 basis points higher than the same quarter the previous year, driven by improving margins in their core business, growth in higher margin services business, offset by the expected dilution of Blue Nile whose merchandise generally carries lower margins.

Near-term headwinds from inflation, shifting consumer spending

Near term, the jewelry giant is expected to see continued challenges; jewelry sales in the U.S. is expected to remain sluggish due to inflationary pressures (management expects a mid single digit decline for the U.S. jewelry industry in FY 2024). Additionally, consumers are increasingly shifting spending away from goods such as jewelry and towards experiences, notably travel and entertainment as economies reopen around the world post pandemic. The U.S. is Signet Jewelers’ biggest market accounting for more than 90% of revenues and all of their operating profits.

Signet Jewelers

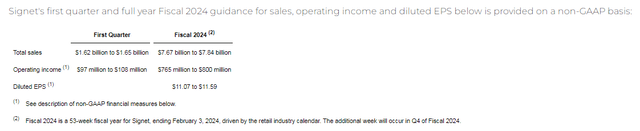

For FY 2024, management expects sales of USD 7.67 to USD 7.84 billion (from USD 7.8 billion in FY 2023), while non-GAAP operating income is expected at USD 765 – USD 800 million (from USD 850 million in 2023).

Signet Jewelers

Medium term: market share gains, shift up accessible luxury, expanding services business could offset limited industry growth prospects

Medium term, certain headwinds facing the industry currently could recede; inflation is on a downward trend, and bridal jewelry demand (Signet’s biggest business accounting for 49% of sales in FY 2023) could get a boost in the coming years as relationship formation (which was delayed during the pandemic) resumes. Nevertheless, jewelry is a mature market and macro conditions are expected to remain challenging, presenting headwinds to growth; Statista expects U.S. jewelry sales to grow less than 1% CAGR over the coming years.

There are however several company-specific factors that could potentially be positive for Signet Jewelers’ topline and bottom line performance medium term despite soft industry conditions. Signet’s position as America’s leading specialty jewelry retailer and their multi-brand strategy allows it to capture spending from a wide base of customer segments across a wide range of price points. Management is confident of growing market share as they embark on their next growth plan Inspiring Brilliance. Initiatives under this plan include expanding to the accessible luxury segment and expanding their digital commerce penetration, and ultimately grow revenues to USD 10 billion mid term. America’s jewelry market is highly fragmented which opens opportunities for consolidation and market share gains among stronger players. Signet’s market share rose to 9.7% in FY 2023 from 6.5% in FY 2020 on the back of management’s efforts to expand its addressable market by strengthening its brands’ positioning (particularly for its top three brands Kay, Zales, and Jared which collectively account for 71% of revenues), increase digital sales as part of an omnichannel strategy (in FY 2023 Signet’s online sales we up 5.8% YoY to USD 1.6 billion accounting for 20% of sales for the year, partly due to the Blue Nile acquisition) and grow its banner portfolio through acquisitions (Signet acquired Diamonds Direct in FY 2022, and Blue Nile in FY 2023).

Strategic initiatives that could be positive for Signet’s bottom line include their efforts to increase their service offerings to customers such as personalization (a USD 700 million opportunity according to management) and repair services as well as store rationalization efforts along with growing eCommerce sales. Services are generally a higher margin business and they have the added benefit of potentially increasing customer loyalty and therefore market share. As of FY 2023, services accounted for just 5% of Signet’s total sales.

Meanwhile, Signet’s store closures (the company reduced 21% of their store fleet) have led to increased cost efficiency and further store rationalization could have a positive impact on profitability going forward.

Financials

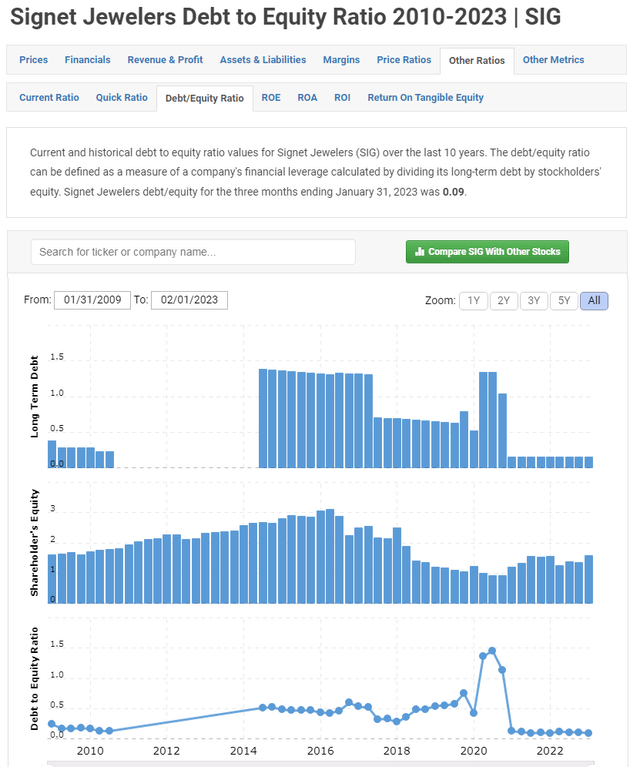

Signet has been paying down debt and their debt to equity ratio has declined significantly which gives them better financial flexibility to make acquisitions. Signet management does not see any major acquisitions down the road but may consider smaller targets.

Macrotrends

Operating cash flows sufficiently cover dividend payments (FCF amounted to over USD 650 million in FY 2023, well above dividend payments of USD 70 million). Share repurchases amounted to USD 376 million.

Risks

Execution risks

Anticipated market share gains may not materialize..

Prolonged recession

A prolonged and severe recession could be particularly negative for Signet Jewelers, not only given the highly discretionary nature of jewelry purchases, but also due to Signet’s middle market positioning which means its customers are more likely to be affected by economic downturns (in contrast to rivals such as Tiffany & Co or Cartier who cater to a more affluent and therefore relatively recession-proof demographic). It took seven years for America’s jewelry industry to recover to levels seen in 2007 i.e., the year prior to the Great Recession.

Signet’s stock has a high short interest of over 15% suggesting considerable investor pessimism over its prospects.

Conclusion

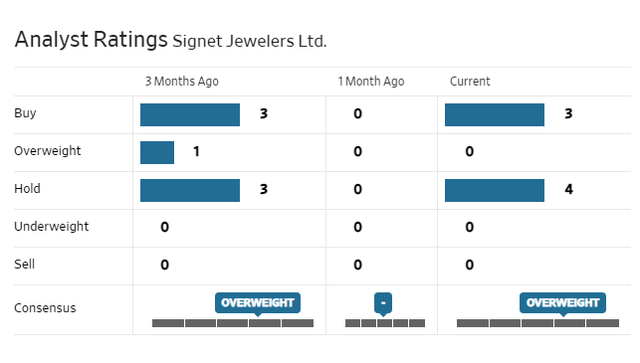

Analysts are split between buy and hold.

WSJ

With a forward P/E of 6.27, Signet Jewelers is looking quite cheap. With the industry not expected to see unusually attractive growth in the coming years (in Signet’s biggest and most profitable market America), Signet’s earnings prospects depend on management’s ability to execute their strategic growth initiatives and gain market share. Considering management’s most recent track record (three year transformation plan “Path to Brilliance” which ended FY 2021 delivered results in terms of market share gains), there are reasons to be optimistic about management’s ability to deliver on their current initiatives but a weakening demand environment due to an anticipated recession, the highly discretionary nature of jewelry as a product category, and Signet’s middle market positioning catering to a relatively price-sensitive customer base make for a relatively unappealing risk/reward at this time. Some may view the stock as a buy while others may view it as a hold.

Read the full article here