Introduction

When dealing with regulated utilities, I cannot say that I’m very passionate about the companies I cover. I consider electric utilities to be extremely boring companies that don’t excite me, like railroads, aerospace companies, or fast-growing high-tech companies.

However, that’s fine, as investing doesn’t need to be exciting all the time. I have incorporated utilities into my dividend growth portfolio right from the beginning, as I believe high-quality utilities not only add satisfying dividends to juice up the average portfolio yield but also stability in times of turmoil.

Atlanta-based Southern Company (NYSE:SO) is one of these companies. It’s far from exciting, yet one of the best utility stocks on the market. The company has a decent 4% yield and a business model that benefits from the near completion of new nuclear capabilities.

Now, the company has room to rapidly reduce leverage and boost long-term dividend growth while (likely) outperforming its peers on a prolonged basis.

Now, let me walk you through the details!

Nuclear Energy & Secular Tailwinds

I own Duke Energy (DUK), one of Southern Company’s peers. However, a number of people who I advise own Southern Company, as I believe it is just as good as my DUK investment.

I discovered Southern Company over a decade ago while studying the coal supply chain in North America. At that time, Southern Company was one of the biggest users of thermal coal.

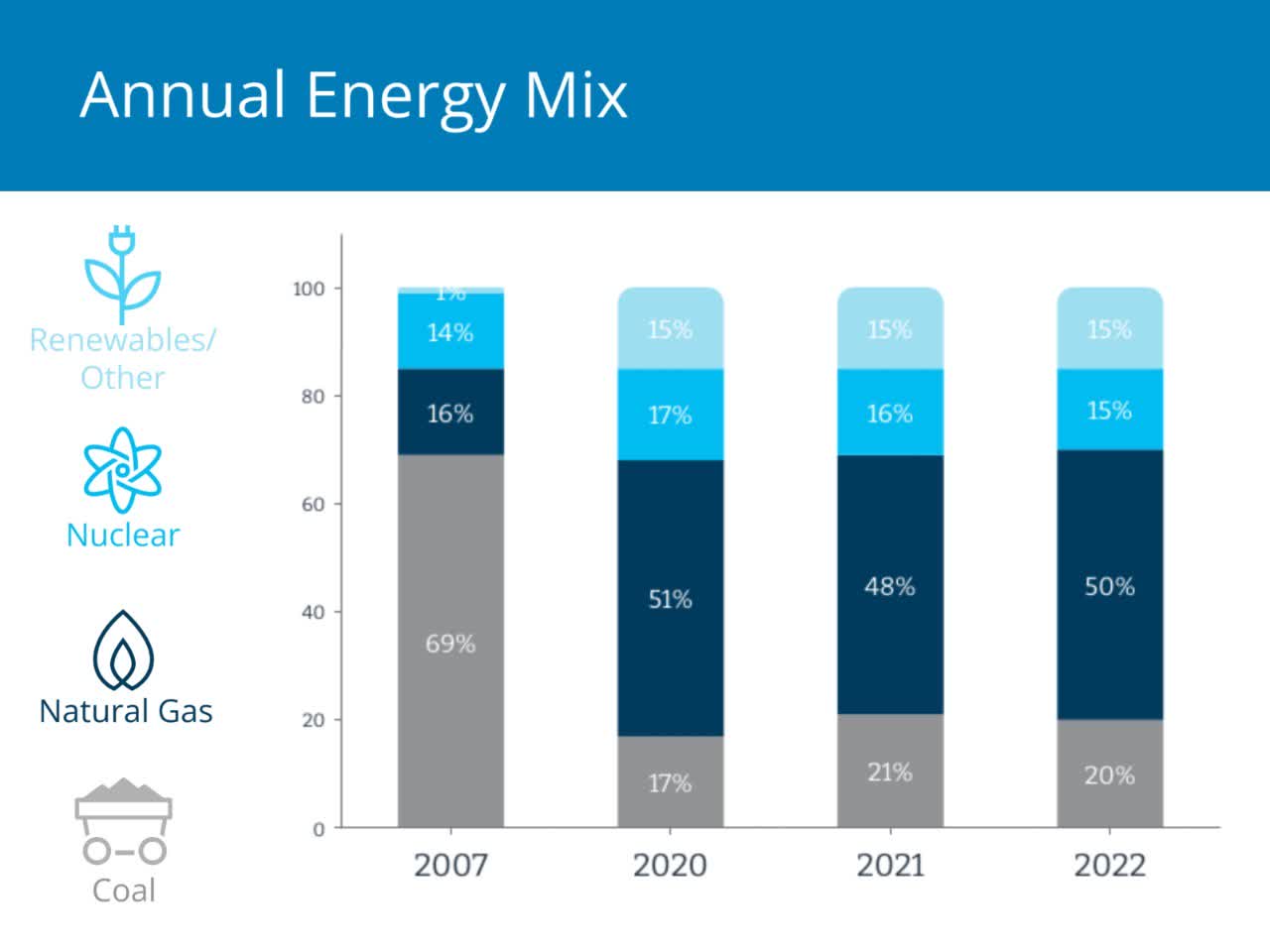

While the company is still a major user of coal, it has reduced its coal mix from 69% in 2007 to 20% in 2022. Natural gas has risen to 50%.

Southern Company

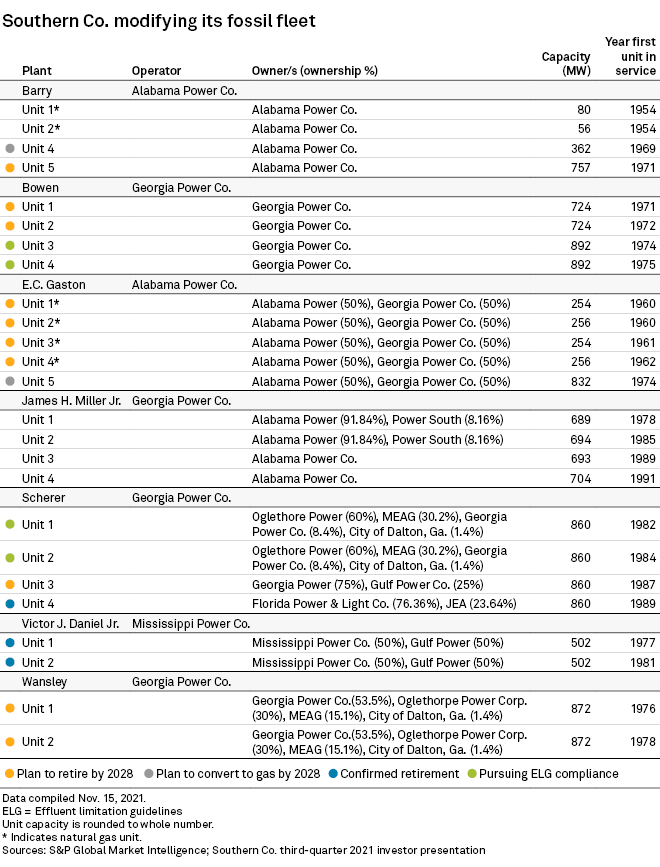

On its way to becoming net zero by 2050, Southern Company is retiring a large number of coal plants.

As reported by S&P Global:

With these expected changes … Southern Co. will have announced total decreases in its coal generating capacity from more than 20,000 MW across nearly 70 generating units to less than 4,500 MW of coal capacity remaining at eight generating units,” Southern Co. Chairman, President and CEO Thomas Fanning said Nov. 4, outlining some of the company’s planned changes during its third-quarter earnings call. “This equates to a reduction of nearly 80%.”

By 2028, the company expects to retire at least ten major plants. Most of these plants were constructed in the 1960s and 1970s. At least two plants will be converted to natural gas.

S&P Global

Nuclear energy plays a significant role in its decarbonization strategy, and I fully support it. I firmly believe that nuclear power is the sole solution for reducing pollution without compromising energy reliability. While wind and solar power have their place in creating a cleaner future, I believe they are more effective on a smaller scale.

Right now, Southern Company is the only company expanding America’s nuclear footprint by adding Vogtle Units 3 and 4. This project started in 2006 when the company applied for permits.

Construction started in 2009. Initially, both reactors were expected to be operational by the end of 2017. Total costs are close to $11 billion.

As much as I love nuclear power, Vogtle is a great example of the costs and efforts tied to nuclear energy.

The good news is that Vogtle 3 & 4 are now close to being completed.

Southern Company

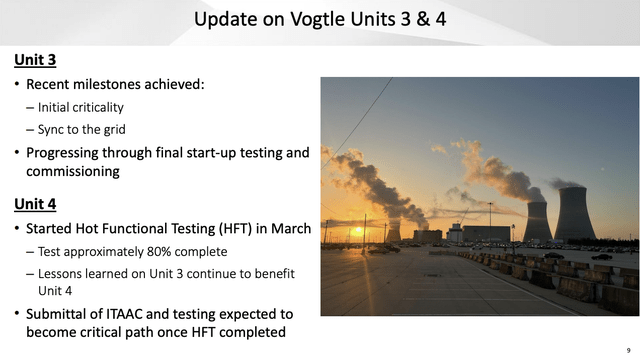

Plant Vogtle Units 3 and 4 are progressing according to the company’s expectations. The projected completion timeline and capital cost forecast for both units remain unchanged from previous updates.

Unit 3 achieved initial criticality in March, successfully synchronized to the grid, and is currently undergoing final startup testing and commissioning. The unit is expected to enter a brief maintenance outage window before returning to full power.

Unit 4 has made substantial progress, with hot functional testing approximately 80% complete. Planned inspections, surveillance, and other final steps are to follow, and the unit is projected to enter service between the late fourth quarter of 2023 and the end of the first quarter of 2024.

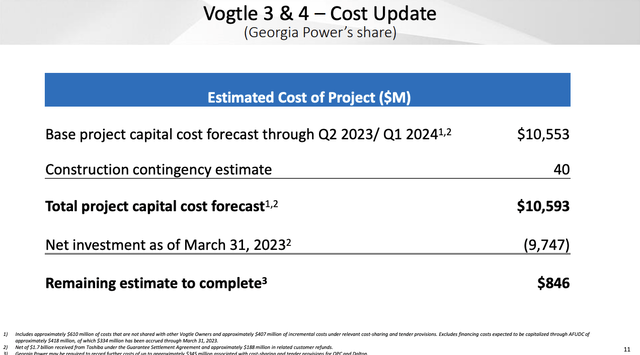

Furthermore, and related to the cost forecast, the company expects that it will require roughly $850 million to finish the nuclear expansion.

Southern Company

Additionally, while it won’t have a major impact on the company’s bottom line, the company is benefiting from secular growth in the form of supply chain re-shoring (one of the topics I cannot stop talking about).

In its 1Q23 earnings call, the company mentioned that the Southeast service territories witnessed record levels of economic development activity during the first quarter, supported by job creation and capital investment announcements.

Notably, the automotive industry contributed to this trend with supplier announcements related to the Rivian (RIVN) and Hyundai electric vehicle manufacturing facilities in Georgia, supporting job creation and capital investment.

Related to this, QCells announced the establishment of a new solar panel and component manufacturing facility in Georgia, expected to generate 2,000 jobs.

The Port of Savannah also experienced growth, expanding its capacity and reducing emissions with the addition of electric cranes. It’s interesting that SO brought this up, as this is something I have discussed with a number of supply chain experts in the past few months. The East Coast is gaining market share from the West Coast, especially when it comes to manufacturing and trade.

Again, this isn’t turning SO into a growth stock – it is way too large for that. However, it is likely to provide healthy topline growth for many more years.

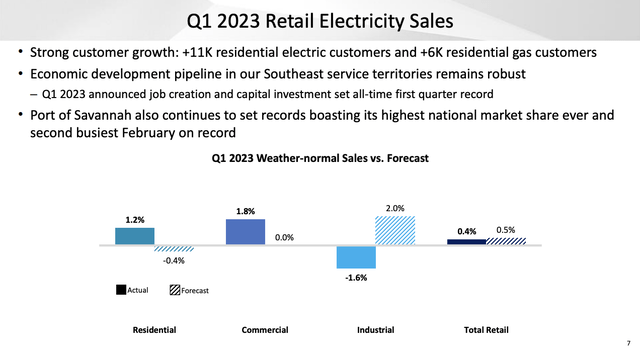

Based on that context, electric retail sales for weather-normal conditions in the first quarter were 0.4% higher than in the same period in 2022.

This increase reflects the aforementioned growth in residential and commercial sales due to robust net in-migration, a strong labor market, and a return to normal business trends.

Southern Company

However, industrial sales declined by 1.6%, primarily driven by weakness in housing-related sectors affected by inflationary pressures and higher interest rates.

The SO Dividend

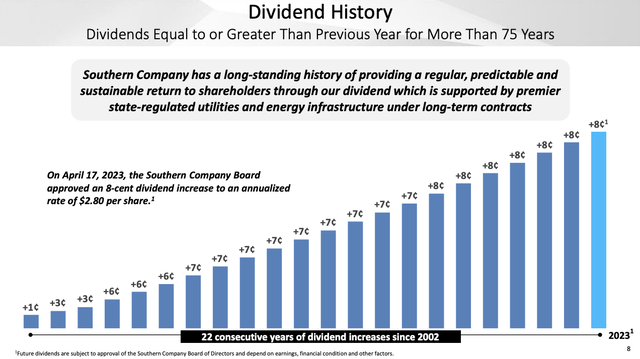

If you like decent dividend yields and consistent growth, SO is the right stock for you. The company has 22 consecutive years of dividend increases. The company hasn’t cut its dividend in more than 75 years.

Southern Company

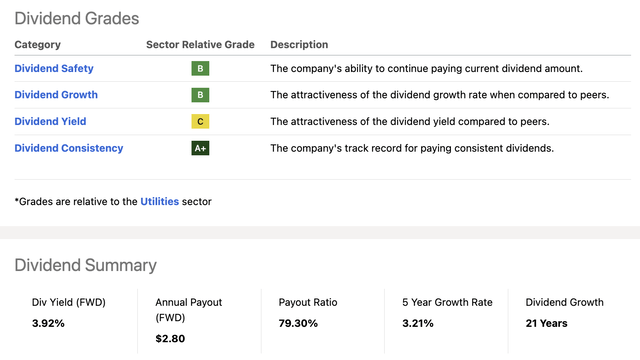

The company’s current dividend yield is 3.9%, which is slightly above the sector median yield of 3.7%. The dividend payout ratio is 79%. That’s elevated, yet nothing unusual in the mature electric utility industry.

Seeking Alpha

The average annual dividend growth rate of the past five years is 3.2%.

On April 17, the company announced a 2.9% hike, which explains why the table above says 21 years of dividend growth instead of 22. It hasn’t been updated yet.

While these dividend growth rates aren’t life-changing, they allow income to grow in line with inflation (unless inflation runs hot like we’re currently witnessing).

Furthermore, the company is soon in a good spot to accelerate dividend growth. Prior to 2023, Southern Company had deep negative free cash flow as a result of funding for the energy transition and regular maintenance capital requirements.

This year, free cash flow is expected to be $1.4 billion. In 2025, that number could rise to $1.9 billion.

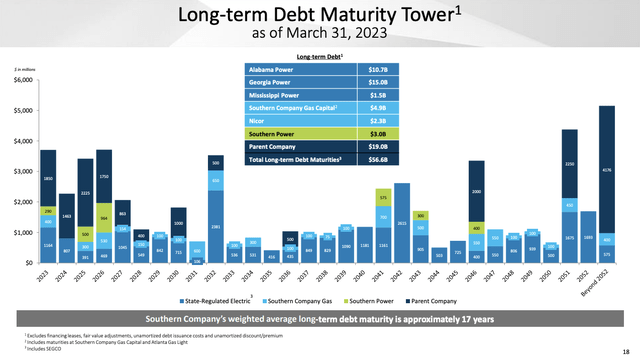

Southern Company has $56.6 billion in long-term debt. That’s a big deal. However, its balance sheet is healthy. Net debt is expected to be $59.9 billion by the end of this year. This translates to a net leverage ratio of 5.8x.

Southern Company

On top of that, the company has $6.0 billion in available liquidity. $7.6 billion of this is unusual credit from its credit lines. The reason why available liquidity is lower than available credit is due to outstanding commercial paper and related short-term liabilities.

Outperformance & Valuation

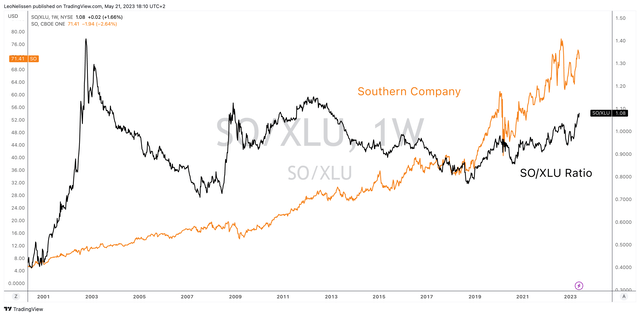

Southern Company has underperformed its peers between 2012 and 2019. That underperformance made sense. SO was struggling with higher-than-expected costs, while others benefited from low rates and sentiment that benefited companies with significant investments in renewables. In this case, I’m using the SPDR Utilities ETF (XLU) as a benchmark.

TradingView (SO, SO/XLU)

Now, SO is outperforming again.

Not only does Southern Company come with a high yield, but its nuclear power headwinds are also turning into tailwinds, giving the company an edge.

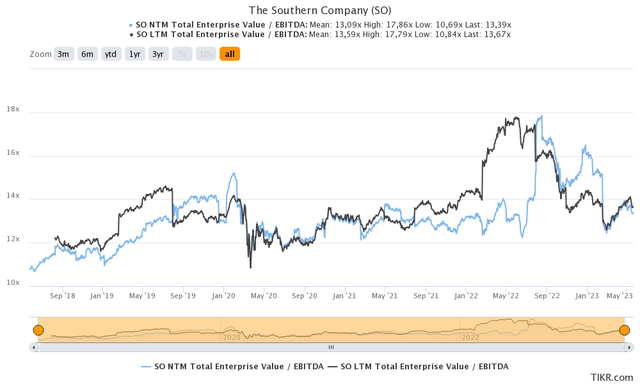

With regard to its valuation, SO is trading at 13.4x NTM EBITDA. This is basically the long-term median.

TIKR.com

While economic headwinds could pressure the stock price in the months ahead, I believe that the price offers buying opportunities.

Takeaway

Southern Company is a stable and reliable utility stock with a decent 4% yield. The company is actively reducing its coal usage and transitioning to natural gas and nuclear energy, aiming to become net zero by 2050.

It is nearing completion of the Vogtle Units 3 and 4 nuclear expansion project.

The company is also benefiting from the growth in the Southeast service territories, thanks to supply chain re-shoring.

Southern Company has a strong dividend track record with 22 consecutive years of increases, and although the growth rate is not significant, it provides inflation-adjusted income.

Related to that, the company’s free cash flow is expected to improve, enabling potential acceleration of dividend growth.

While it has a sizable debt, its balance sheet remains healthy, with ample available liquidity.

After a period of underperformance, Southern Company is now outperforming its peers. With a reasonable valuation, it presents potential buying opportunities, although economic headwinds could impact the stock price in the near term.

Read the full article here