Paycom (NYSE:PAYC) operates in B2B SaaS software with many of the markers I look for in the highest quality businesses. I own shares and continue to add as the stock has dropped around 18% since the last time I covered the business. With the initiation of a dividend, continued exemplary management, and a long runway for growth, Paycom is a core holding for my long-term portfolio and is a strong buy today.

Earnings Call

Recent earnings gave me no cause for concern. Revenues grew 28% YOY, with 98.4% of those revenues recurring. The company has $506M in cash on the balance sheet against $29M in total debt, and guidance for the full year 2023 is for 25% revenue growth.

One of the most noteworthy growth prospects for the business was highlighted on the earnings call:

Raimo Lenschow

Thank you. Congrats on a number of strong quarter and dividend introduction. Two quick questions for me. First, on the global initiative, Chad, can you help us understand a little bit like how a global or like what’s the extent of what you’re trying to do here? Is this like helping existing customers that have subsidiaries? Is this like a whole sea change in strategy that you become like more international? Just help us understand a little bit there and then I have one follow-up?

Chad Richison

Sure, and so right now, Raimo, we have several clients who currently use our domestic software, and they use it internationally, they rigged the system a little bit so that they can store employees in other countries, and then oftentimes, they’ll work with a third-party for payroll.

So our current clients, they don’t have to do this any longer. Because the Paycom system now does have Global HCM product that’ll work in 180 countries in 15 languages. And Global HCM for us is everything, minus the payroll side. And so, we’ve looked at integration opportunities, we’ve looked at working with third-parties, and even potential acquisitions. But the fact is everyone else does it the old way, and payroll and HR departments send data for processing. And we’re not going to be putting any development into the old way. So for us, BETI is packing her bags, and we’ll be going around the globe, as we develop it out.

Paycom serves many companies with international operations, but the expansion into the international market could provide a greenfield opportunity for growth. The company’s market share (~5%) is still a small slice of the TAM, but other cloud software companies have found great success with international expansion. Retailers and consumer products are more difficult than a software offering to tailor to different countries, so this will be something for investors to watch going forward. Notably, Paycom has rarely acquired its way into new offerings. Management is confident in the company’s ability to create software, and they seem to prefer to build in-house. This lowers the overall risk, in my view, of value-destructive acquisition.

Market Position

Taking a look at the G2 grid for payroll software offerings, Paycom still has some space to catch up to Automatic Data Processing (ADP), the incumbent, but remains among the sector’s leaders. In momentum, the company also falls out as a leader, but the market is incredibly crowded. There are a ton of offerings here in a highly fragmented space. For a top-tier offering like Paycom, I see that as an opportunity.

In Human Capital Management and Human Resources Management Systems software offerings, Paycom is again a leader, trailing slightly behind ADP. The company’s satisfaction is somewhat lower based on G2 scrubbing verified review data than some offerings by Paylocity and Rippling. However, there’s plenty of room in this market (every company does payroll and HR) for multiple winners. Again, on momentum, Paycom remains a leader, though Rippling is an interesting private offering that seems to have massive customer satisfaction among its user base.

I like to use G2 grids for cloud software companies, especially B2B ones, in order to get a feel for the marketplace. There’s a chance you see a company slowing its revenue growth and the reason is clear as day on customer satisfaction. Separately, I always want to be invested in the leaders vice those companies losing share in the marketplace.

The Dividend

As an investor, I’m excited about Paycom initiating a dividend, and I want to show some data as to why. Many companies, including Paycom, have used buybacks extensively in lieu of a dividend. However, poor timing in many cases on that buyback, debt-fueled buybacks, and those only compensating for massive share dilution have led me to favor a dividend paying company in a vacuum.

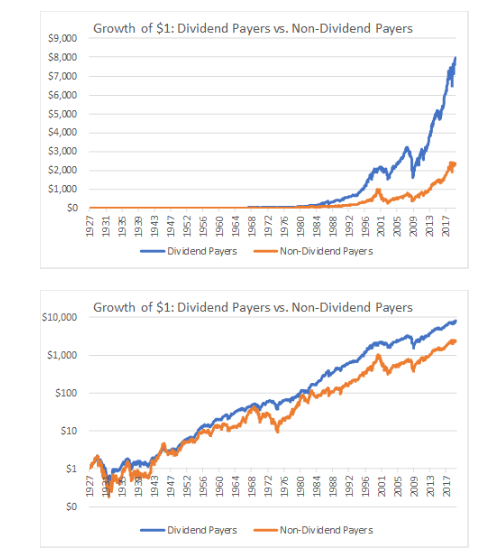

Ploutos Article on Seeking Alpha

It’s not just that I like dividend paying stocks more, however. It’s backed up by data, the graph above courtesy of SA author, Ploutos. Dividend payers have historically outperformed non-dividend payers over time. There’s likely several factors to consider here. In the data set Ploutos used, a dividend paying company was only included in the chart once it initiated a dividend, and then its performance was removed if it cancelled the dividend.

There are plenty of poor quality, poor performance dividend payers out there. However, in a vacuum, companies that can afford to initiate and pay out excess capital to shareholders are more stable and should outperform.

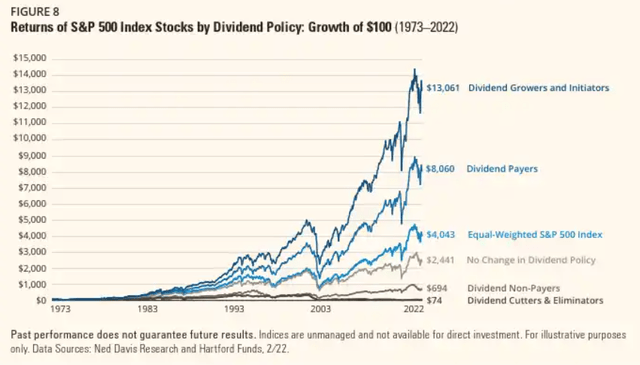

Hartford Funds

But, there’s a wrinkle. It’s not just dividend payers that perform the best. Companies that initiate and then grow the dividend are earlier in their business trajectory, and tend to be higher quality. These companies have outperformed companies offering a static or declining dividend. From the earnings call:

Robert Simmons

Got it. And then on the dividends, how do you think about it just seemed like going forward? Would it be as percent of GAAP EPS or free cash flow or some other metric?

Chad Richison

Now, I mean, right now, it’s — we’re looking at it as a fixed amount, the $50 over the next year, or $37.5 a quarter. I mean, right now, it’s, that — it’s basically a 50% to about a 50% or 0.5% dividend yield based on our start current share price. So, but we would look at it as that $50 and then adjust that as we see fit in the future.

So, Paycom hasn’t committed yet to growing its dividend, but the company has a ton of space to do so. The cash flow potential on an asset-light software business with well-maintained expenses like Paycom should be able to provide ample dividend growth for years to come.

I can’t guarantee anything, but I expect to see them start hiking it, and if I had to guess, it should be relatively in-line with the company’s 20%+ earnings growth. This is pure conjecture, as the above is the only perspective I’ve seen from management on their future plans.

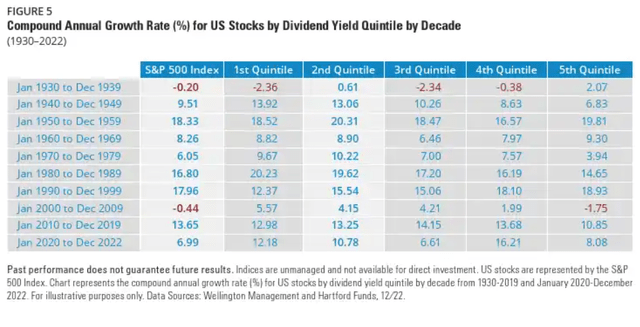

Hartford Funds

Many investors may turn their noses up at the payout. At $1.50 a share annually, the dividend isn’t going to move the needle today. That results in about a 0.53% dividend yield. However, the highest CAGR’s (total return) for companies actually resides in the lower quintiles of dividend payouts. If you’re looking at the long term and not for immediate income and focus yourself on total returns, the companies that leave themselves margin for continued investments in growth tend to outperform. Of note, these low yielding, low payout ratio companies also tend to be expensive on an absolute basis.

With a payout ratio of only around 16% on a forward earnings basis and earnings growth projections north of 20% for the next 3 years, Paycom should be well set to maintain flexibility and invest for growth while returning capital to shareholders.

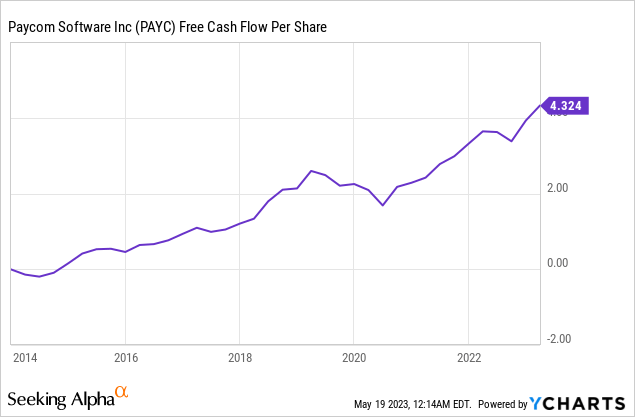

Free Cash Flow and Balance Sheet

I look for companies able to generate higher free cash flow per share over time. The “per share” helps see through some of the financial engineering commonplace with cloud software companies. These companies will pay employees with stock, which reduces their non-GAAP expenses and generates free cash flow. However, despite this being real cash flow, on a GAAP basis and from a real economic sense, the cash is funded via shareholder dilution.

In Paycom’s case, the trajectory is exactly what I want to see, and the FCF/share easily covers the company’s new $1.50/share dividend.

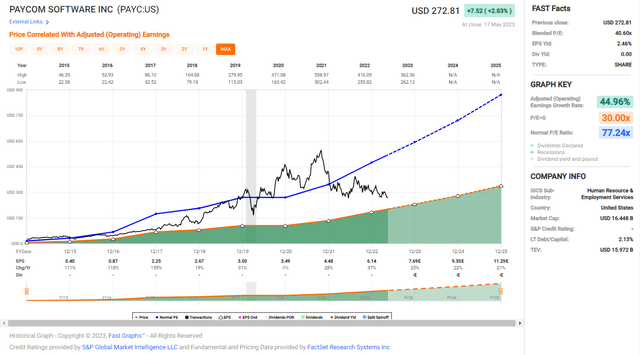

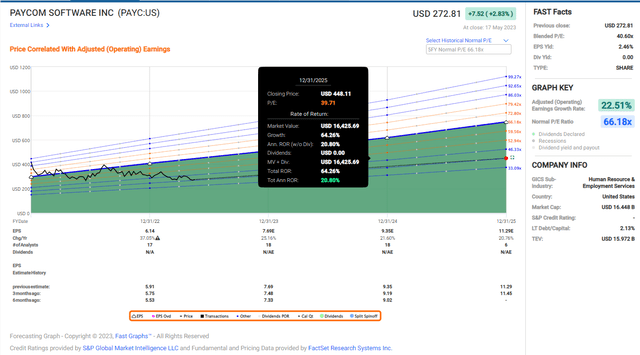

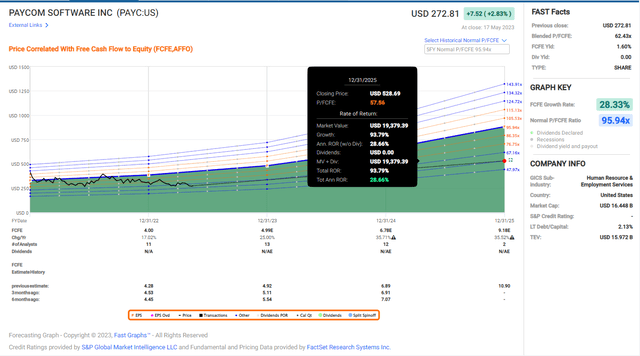

Valuation and Metrics

FAST Graphs

The earnings growth over time has been fantastic, at a 45% CAGR. The company’s valuation has come back down to earth and the share price is now in a similar spot to where it was in 2019, despite significant earnings growth since then.

FAST Graphs

Based on analyst estimates for earnings growth and maintaining the same valuation (40X earnings is still somewhat steep but seems fair to me considering the growth), investors could be looking at 20%+ annualized rates of return over the next few years. Obviously, multiple compression and expansion are likely, so this is just a useful thought exercise.

FAST Graphs

Looking at the company’s growth projections in free cash flow, and the picture is even rosier, with no change in the multiple resulting in closer to 30% annualized rates of return.

Paycom is taking the next step in its business in two ways. International expansion seems like a logical step for the company, and the initiation of a dividend sets the company apart from its peers and makes it even more intriguing for me. I’m adding on any weakness, and it’s a core high quality holding in my long-term portfolio. It’s a strong buy.

Read the full article here