Dear readers/followers,

Following my recent articles on Brookfield Asset Management (BAM) and Blue Owl Capital (OWL), both of which I’m very bullish on and both of which represent large positions in my portfolio, today I want to cover another promising alternative asset manager – Apollo Global Management (NYSE:APO).

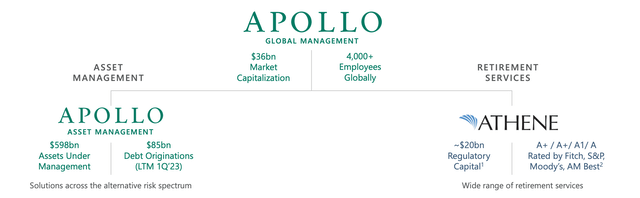

Apollo is a little different than other alternative managers in that the holding company which we are investing in has two distinct divisions. One is a traditional asset management business (similar to BAM) which is all about investing other people’s money into private equity, debt and real estate and charging a fee on the managed assets. This division generates fee-related earnings (FRE). The other is a retirement services business which is all about selling fixed annuities and investing the capital into higher return strategies (mostly private credit) which earns the company a spread. As you can probably guess, this division generates what’s called spread related earnings (SRE). What’s great is that FRE as well as SRE are very sticky because they’re mostly generated from long-term capital which cannot be easily recalled. The earnings are therefore highly visible and predictable and future performance is mostly about growing assets under management in each division. In addition, Apollo also earns Principal Investing Income (PII) which is similar to carry and essentially includes performance fees, which are inherently more volatile and are likely to suffer in an economic downturn.

Apollo Presentation

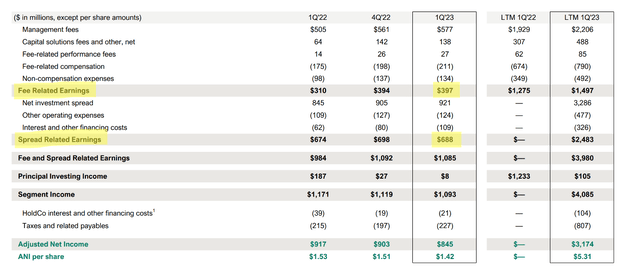

Looking at their most recent Q1 results, we see that fee and spread related earnings increased by about 10% YoY, but have been flat for the first quarter. This growth was entirely attributable to growth in asset management FRE which increased by 28% YoY to $397 Million – a very good result. Although net investment spread in their insurance business has increased by 9% YoY, Spread Related Earnings have been roughly flat for the last year, mainly due to growing interest costs and poor performance of Athene’s portfolio (see next paragraph). As expected in the current tough economic conditions, principal investing income was minimal at just $8 Million in Q1 (down from $187 Million last year) which hurt the bottom line, causing total segment income to drop 7% YoY, despite outstanding growth in their asset management business.

Apollo Presentation

Management also presents us with a “normalized” version of earnings which is the one they refer to on the earnings call. The normalization comes in the form of adjusting the return of Athene’s $12.1 Billion alternative investment portfolio to 11%. The argument here is that despite a return of only 6.1% in Q1 2023, on average the portfolio has historically returned at least 11% (10 and 5-year average) and as much as 13% if we average the past three years. This normalization inflates Q1 2023 and suppresses Q1 2022 so in essence it makes the YoY numbers seem much better. I’m not buying it and will use the numbers as reported, but at the same I recognize that this under-performance will likely be short-lived and the final numbers for 2023 will likely stand somewhere in between the reported and normalized numbers.

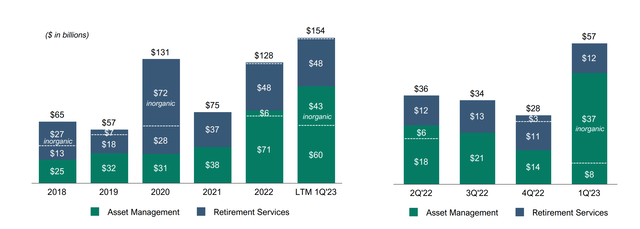

What’s important is that the company is able to grow its asset under management (AUM). During the first quarter Apollo experienced a record $57 Billion of inflows (though $37 Billion was inorganic including $20 Billion from Atlas which will earn a fee of just 0.1%) which increased its total AUM to $598 Billion. The company is well on its way to achieve its $130 Billion fundraising target for 2023. Since AUM is the key driver, I will be watching their fundraising closely over the next couple of quarters, because excluding inorganic inflows, it’s obvious that fundraising has slowed – just as it has slowed for BAM and OWL. So far, though, I see no reason to freak out.

Apollo Presentation

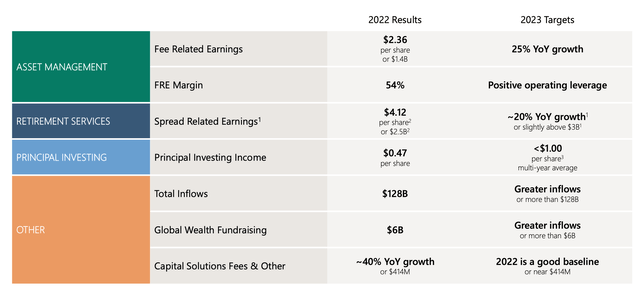

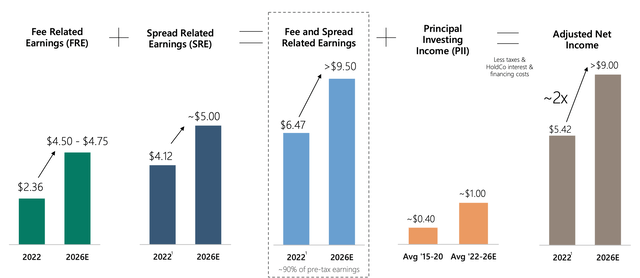

With regards to the rest of guidance, for 2023 the goal is to grow FRE to $2.36 per share (+25% YoY). To achieve this, APO needs to average FRE of $437 Million per quarter. That’s about 10% more than what they achieved in Q1 so there is some work left to do for sure, but management has confirmed that they feel good about achieving this target. As far as guidance for spread related earnings, they expect 20% YoY growth to $4.12 per share, implying about $750 Million per quarter in SRE. With $688 Million in Q1 ($811 Million normalized), this seems achievable, though again some work left to do. Principal Investing Income is expected to come in just below a multi-year average of $1 per share, but since performance fees will likely be minimal in an economic downturn (as confirmed by Q1 performance), I’m going to exclude PII from my valuation, essentially assuming no performance fees/carry are earned. That means that management is targeting Fee and Spread related earnings of $7.89 per share for 2023.

Apollo Presentation

Beyond this year we don’t have much to rely on for guidance, other than their 5-year plan, which assumes that AUM will reach $1 Trillion by 2026 with FRE and SRE combined at $9.50 per share. That’s 46% growth from 2022 levels, which seems quite achievable, especially if the company delivers on their guidance of 20% growth in 2023 alone. The plan is fairly similar to that of BAM and OWL, in essence we’re looking a double over the next 4-5 years if management delivers on their target. Since Apollo’s business is more asset-heavy than BAM’s and OWL’s, in addition to valuing the company at a multiple of FRE (+SRE in Apollo’s case), I’m also going to look at their adjusted net income (ADI), which deducts taxes and HoldCo interest and financing costs. ADI is expected to reach $9 per share by 2026. Ignoring performance fees/carry to stay extra conservative, ADI is likely to end up around $8 per share in 2026 (up 53% from $5.21 per share in 2022).

Apollo Presentation

Apollo has a decent track-record of rewarding shareholders. Although a dividend of 2.8% is on the lower end, the company has also repurchased a non-negligible amount of stock. In particular, last year they spent $319 Million on opportunistic share repurchases, which returned an additional 0.9 percentage points to shareholders, essentially increasing the dividend to 3.7% which is more in line with the 4% average that other asset managers target. In Q1, the dividend was increased by 7% to $0.43 per share and additional $160 Million was used for share repurchases.

Finally, in terms of valuation, assuming that management delivers on their 2023 targets and ignoring principal investing income for the reason discussed before, APO trades at just 8.1x forward FRE+SRE. That’s a lot lower than the asset-light the BAM and even OWL which trade at about 23x and 18x FRE, respectively. Frankly I think a pure asset management business deserves a much higher multiple than the insurance business. This was very well explained by a fellow SA author Alexander Steinberg in his article here. Even being extra conservative and assuming low end multiples for asset management and insurance of 20x and 10x, respectively and assuming PII of zero, APO is valued at $108 per share based on 2023 estimates. The most bearish outcome I can imagine is no growth in 2023 which would yield a value of $88 per share (based on 2022 number with no growth what so ever). That’s still above the current price of $64 per share. Any way you look it, APO represents a worthy addition to any alternative asset management portfolio which is why I rate the company as a BUY here at $64 per share.

Read the full article here