Thesis

In Oct 2022, I published an article entitled “Duke Energy And XLU: Still Worst Time To Buy Since 2008”. My main thesis was their expensive valuation when adjusted for risk-free rates. At that time, the utility sector, represented by the Utilities Select Sector SPDR ETF (NYSEARCA:XLU), was the most expensive market sector. And its leading stock Duke Energy (NYSE:DUK) is even more expensive than XLU by historical standards. And I cautioned readers that the interest rates uncertainties can further pressure their profit and valuation.

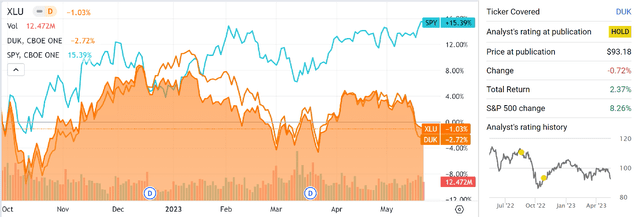

A few things have developed since then and motivated this updated article. First, their price actions and valuation change. As you can see from the chart below, since my previous article, both DUK and XLU have indeed lagged the overall market by a large margin (both in terms of price return and also total return when dividends are adjusted).

Source: Seeking Alpha

Second, DUK has also released its Q1 FY23 earnings report (“ER”) in early May (May 9, 2023). Its Non-GAAP EPS indeed missed consensus estimates ($1.20 vs. $1.26) due to some of the headwinds I analyzed. However, what’s of fundamental relevance to me is that its management reaffirmed its 2023 full-year guidance in a range of $5.55 to $5.75. Its FWD dividends are also stable. Such an outlook implies a long-term growth rate of 5% to 7% off the midpoint of the 2023 range. Later, we will see that such a stable growth rate, combined with the price actions mentioned above, made DUK a much more favorable investment opportunity than back in Oct 2022.

Finally, interest rates. Treasury rates indeed rose since my last article and pressured the valuation and profits of both DUK and the whole sector as approximated by XLU. However, at this point, I expect the interest rates to stabilize around their current levels. And furthermore, my analysis shows that the pressure has created a larger valuation impact on DUK than on XLU. As a result, DUK has also become much more attractive relative to XLU.

In the remainder of this article, I will elaborate on all the above points one by one.

XLU and DUK

Before going into the details, just a quick word about DUK and XLU in case there are readers new to them. XLU is a highly popular fund focusing solely on utility companies. Its top holdings are shown below and as seen, DUK is a top holding with a large weight of 7.45% of its total assets.

It is always a good idea in my view to compare a leading stock in a sector against the sector average. There are many good reasons including performance benchmarks (like what we’ve already done in the first chart), identification of sector trends and risks (like the impact of interest rates I mentioned), and also the assessment of relative valuation – which is what I will do next.

Source: Seeking Alpha

Impacts of rising interests

As argued in my earlier article, a main concern for my pessimistic view in Oct 2022 involves the impact of rising interest rates. Quote:

Utilities have been helped by the secularly low-interest rates in the past decade. And now interests are on the rise and will pose a headwind. All utilities heavily depend on delta financing (and hence utility funds like XLU depend on debt financing too subsequently). And rising rates will cause increased interest rates and pressure their profits.

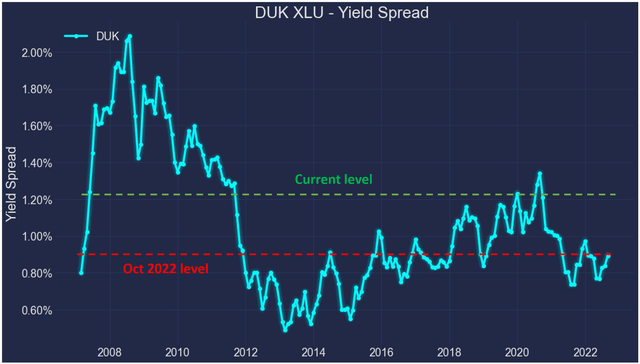

The impact did come as aforementioned. However, the impact was unevenly distributed and DUK’s valuation was contracted more than XLU’s. For readers familiar with our approach, you know that a good way to evaluate the impact of rate changes is by examining the yield spread (“YS”), especially for stocks/ETFs that pay stable dividends like XLU and DUK. The next chart shows the YS between DUK and XLU. This is a key chart that we used to caution our readers against DUK in Oct 2022.

Again, at the time, the valuations of both DUK and XLU were at the most expensive level since 2008 when adjusted for risk-free rates. And the chart shows that the risk premium of DUK compared to XLU was also among the peak levels since 2008 (shown by the red dashed line).

Now, due to the combination of price action and business fundamentals, the YS between DUK and XLU has expanded to a much more favorable level shown by the green dashed line. To wit, the YS is about 1.21% (4.35% dividend yield from DUK minus 3.14% from XLU). By historical standards, this level of YS is among the thickest level in the past decade, signaling a much more favorable risk premium for holding DUK.

Source: Author based on Yahoo Finance data

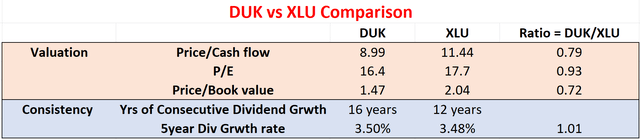

The above analysis can be easily reinforced by other metrics such as those summarized in the following table. This table compares the valuation metrics of DUK and XLU in terms of common metrics such as P/E, P/cash flow, and P/BV ratios.

The data is compiled from various sources (Seeking Alpha, Yahoo!, and also XLU’s webpage). As seen, DUK is heavily discounted from XLU even though its scale and financial strength make it safer and better positioned than the sector average in my view. You can see this by its longer and more consistent (and also slightly faster) dividend growth rates in the past. To wit, DUK has a lower price-to-cash flow ratio (8.99x) compared to XLU (11.44x), indicating a relative undervaluation of 21%. In terms of P/E, the discount is not as large but still a sizable 7% (16.4x compared to XLU’s 17.7x). And finally, in terms of the Price/Book ratio, the discount is even larger. DUK has a P/BV ratio of 1.47x. Compared to XLU’s 2.04x, this implies an undervaluation of 28%.

Source: Author

Risks and final thoughts

The risks of owning utility stocks in general and DUK in particular have been detailed in my earlier article already. To recap, these risks include their sensitivity to interest rates (after all, the future change of interest rates is uncertain), Intensive requirement of capital and infrastructure investment (which further compound the interest risks because most of these requirements are met by debt financing), and also regulatory and political risk. Here I want to elaborate on a risk specific to the approach of benching marking a stock against the sector average (either via the YS I used above or other methods). Such an approach can generate relative outperformance but cannot guarantee a positive absolute return. For example, my October 2022 article concluded that XLU is relatively better than DUK. And indeed, it outperformed DUK on a relative basis, but both suffered negative price returns.

To conclude, a few developments in the past ~1 year have changed my assessment of DUK and the utility sector in general. These developments include the valuation contraction, Duke’s stable guidance for the full-year 2023 and long-term growth rates, and my expectation that interest rates should stabilize under current conditions. After analyzing these changes, my conclusion is that the utility sector is still expensive as a whole (as indicated by our market dashboard below). But I see DUK as a much more favorable candidate now.

Read the full article here