The IQOS Investment Thesis Is Still Robust

Philip Morris International (NYSE:PM) has reported a mixed report card for FQ1’23, in our opinion. It reported revenues of $8.02B (-1.2% QoQ/ +3.6% YoY) and an adj EPS of $1.38 (inline QoQ/ -11.5% YoY), suggesting a minimal contribution from Swedish Match despite the eyewatering $16B price tag.

On the one hand, its combustible tobacco net revenue remains somewhat stable at $5.22B in FQ1’23 (+1.5% QoQ/ -1.5% YoY), compared to its tobacco peer, Altria Group, Inc. (MO) at -6.6% QoQ/ -3.2% YoY.

On the other hand, PM has underperformed compared to British American Tobacco (BTI, OTCPK:BTAFF). While the latter has yet to report its bi-annual H1’23 results, its H2’22 results showed an impressive cadence, with an +13.8% increase from H1’22 and +6.6% YoY from H2’21.

Then again, investors need not fret, since the PM management already guided a second-half weighted top and bottom line expansion in FY2023, likely to accelerate from FQ2’23 onwards.

The optimism is already visible in its forward guidance, with FQ2’23 adj. EPS of $1.44 at the midpoint (+4.3% QoQ/ -2.7% YoY) against the consensus estimate of $1.60. This number includes a forex impact of -$0.13, without which may have raised its bottom line expansion to +13.7% QoQ/ +6% YoY instead.

PM’s FY2023 guidance may seem disappointing as well, with organic revenue growth of +7.7% and adj. EPS of $6.16 (+3% YoY). However, we must also highlight that the latter also includes another forex impact of -$0.30, without which may have triggered a “currency-neutral adj. EPS growth of 7% to 9%.”

This cadence is impressive indeed, in comparison to its historical cadence of +3.8% in FY2019 and normalized CAGR of 4.84% between FY2019 and FY2022. This is especially given the rising inflationary pressure and supply chain issues impacting its gross margins to 62.3% in the latest quarter (+2 points QoQ/ -4.4 YoY), with operating expenses further increasing at the same time (inline QoQ/ +18.3% YoY).

Therefore, while the Swedish Match acquisition may not be notably top and bottom-line accretive yet, with the PM management qualifying that it may only be “low single-digit accretive” in 2023, we suppose things may improve from 2024 onwards once the inflation peaks, the Fed pivots, and the forex headwinds normalize. Only time may tell.

For now, the tobacco company continues to record excellent revenue growth in the smoke-free products to $2.71B (+17.3% QoQ including Swedish Match) in FQ1’23, while growing its IQOS users to 25.8M (+3.6% QoQ/ +44.1% YoY). These numbers suggest its brilliant smoke-free strategy, as witnessed through the reassignment of the US IQOS rights.

Its US peer, MO, has suffered significant cigarette volume declines by FQ1’23, by -7.3% QoQ and -11.4% YoY, triggering the notable headwinds in its revenues as discussed above. Perhaps this is why the tobacco company has gone on several investment/ acquisition sprees over the past few years, in order to grow its smoke-free approaches, with the latest being NJOY, a vaping/ e-cigarette company.

In addition, market analysts already expect the US smoke-free market to grow in value from $10.90B in 2021 to $42B in 2030, at an accelerated CAGR of 16.1%. As a result of the sustained transition toward smoke-free products in the US and PM likely to re-enter the domestic HTP market from May 2024 onwards, we may see the tobacco company potentially achieve moderate success indeed.

This cadence will be significantly aided by the US FDA marketing authorization for three new Marlboro heated tobacco products (used with the IQOS device) in early 2023. Combined with its earlier plan to manufacture IQOS in the US to sidestep the ongoing import ban, there appear to be minimal regulatory hurdles ahead, accelerating its “ambition to become a majority smoke-free business” by 2025.

So, Is PM Stock A Buy, Sell, Or Hold?

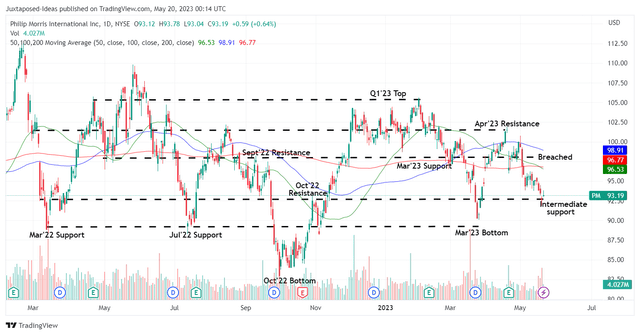

PM 1Y Stock Price

Trading View

PM has already breached its previous March 2023 support levels and is about to retest its intermediate support levels at $93, if not at the March 2023 bottom of $90.

While that may usually be bearish news, we must also highlight that PM is by no means a high-growth stock, since it is better viewed as an income stock instead. Over the past five years, its dividends per share have grown at a sustainable CAGR of 3.70%, with an average payout ratio of ~85% at the same time.

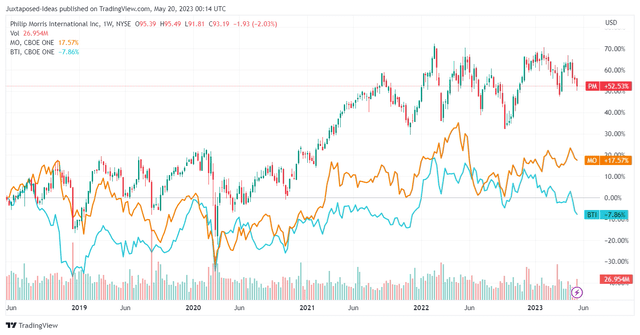

PM, BTI, and MO 5Y Returns (Adjusted For Dividends)

Trading View

In addition, PM outperformed with a 5Y return of +65.70%, compared to its peers such as BTI at -3.11% and MO at +19.43%, after adjusting for dividends. Given that its performance nears the SPY at +65.70%, we are impressed indeed.

Hence, income investors may welcome the chance to DRIP and/or dollar cost average below its 50-day moving averages, while also unlocking an expanded forward dividend yield of 5.57%, exceeding its 4Y average of 5.46% and improved than the sector median of 2.41%.

This is based on our projection of annualized dividends of $5.20 (a raise to $1.33 for FQ3’23 and FQ4’23), comprising nearly 85% of its projected FY2023 EPS and current stock prices. Combined with the factors discussed above, we continue to rate the PM stock as a Buy here.

Then again, investors also need to temper their expectations accordingly, since it is unlikely that the tobacco company may embark on any share purchases and/ or aggressive dividend hikes in the near term, due to the massive growth in its long-term debts to $40.41B by FQ1’23 (+15.8% QoQ/ +68.7% YoY).

However, with an annual Free Cash Flow generation of $9.7B in FY2022, PM still appears to be well capitalized for now.

Read the full article here