A Quick Take On Consensus Cloud Solutions

Consensus Cloud Solutions (NASDAQ:CCSI) reported its Q1 2023 financial results on May 9, 2023, missing both revenue and EPS consensus estimates.

The firm provides an array of information delivery technologies to organizations worldwide.

Management continues to hire employees and restructure its go-to-market organization to increase sales velocity.

Operating income is dropping and management sees a recession in 2023, so I’m Neutral [Hold] on CCSI in the near term.

Consensus Cloud Solutions Overview

Los Angeles, California-based Consensus Cloud was founded to provide communications technologies for a range of industry verticals including healthcare, finance, legal, insurance, manufacturing and real estate.

CCSI was spun off from J2 Global in October 2021 as part of J2’s plan to separate into CCSI and Ziff Davis.

The firm is headed by Chief Executive Officer Scott Turicchi, who was previously President of J2 Global and was a Managing Director at investment banking firm DLJ.

The company’s primary offerings include the following:

-

Workflow solutions

-

Event notifications

-

Robotic process automation

-

Natural language processing

-

Interoperability

-

Cloud fax

-

eSignatures

CCSI acquires customers via its direct sales and marketing efforts and through a robust partner network of resellers, solution providers, white-label partners and others.

Consensus Cloud’s Market & Competition

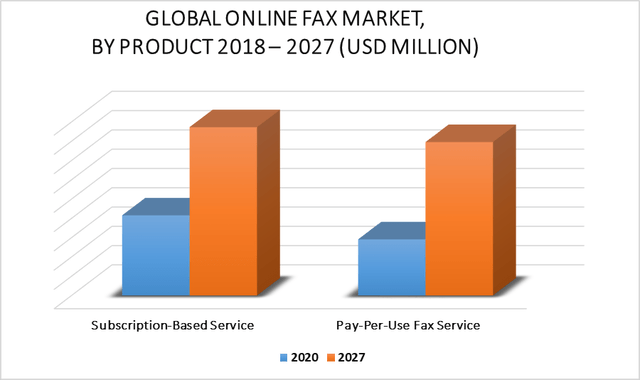

According to a 2021 market research report by Verified Market Research, the global market for online fax services was estimated at $$3.2 billion in 2019 and is forecast to reach $8.34 billion by 2027.

This represents a forecast CAGR (Compound Annual Growth Rate) of 13.06% from 2020 to 2027.

The main drivers for this expected growth are continued demand from the industries of healthcare, finance and manufacturing, among others.

Also, the chart below shows the global online fax market through 2027 by product type:

Global Online Fax Market (Verified Market Research)

Major competitive or other industry participants include:

-

OpenText

-

Century Link

-

Biscom

-

Retarus

-

Softlinx

-

DocuSign

The company operates in other software and technology industry segments.

Consensus Cloud’s Recent Financial Trends

-

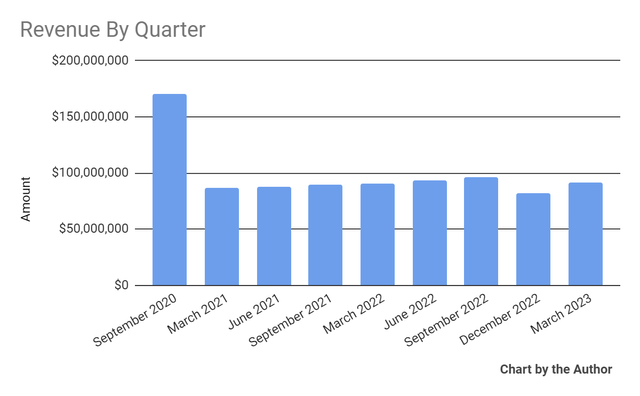

Total revenue by quarter has produced the following trajectory:

Total Revenue (Seeking Alpha)

-

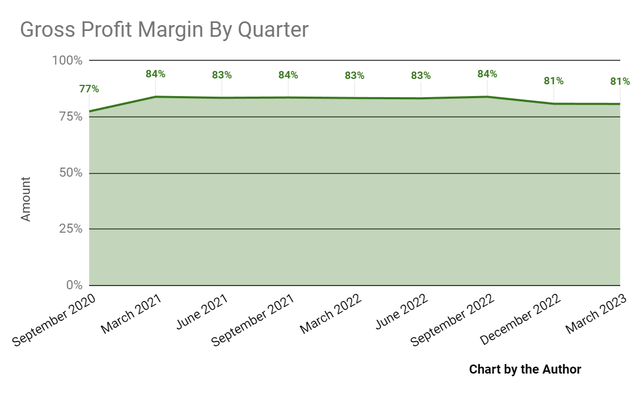

Gross profit margin by quarter has dropped in recent quarters:

Gross Profit Margin (Seeking Alpha)

-

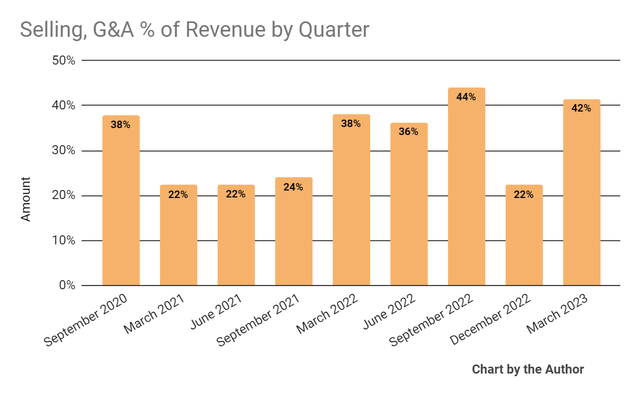

Selling, G&A expenses as a percentage of total revenue by quarter have risen more recently, as shown in the chart below:

Selling, G&A % Of Revenue (Seeking Alpha)

-

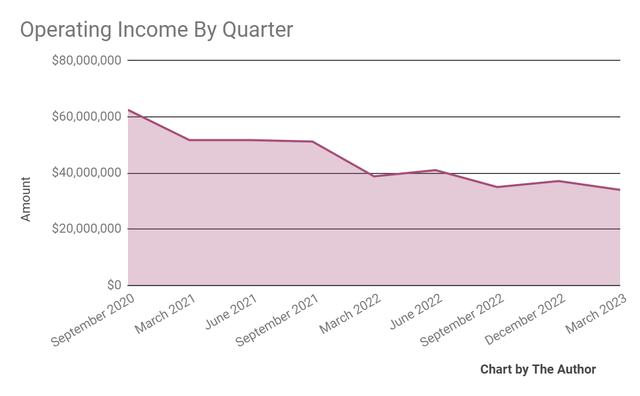

Operating income by quarter has trended lower materially in recent quarters:

Operating Income (Seeking Alpha)

-

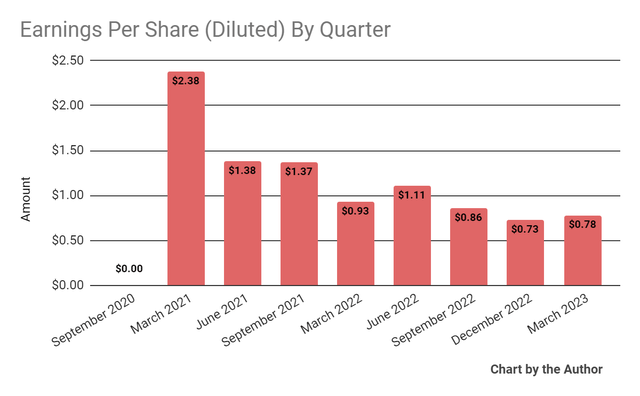

Earnings per share (Diluted) have dropped in recent periods:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

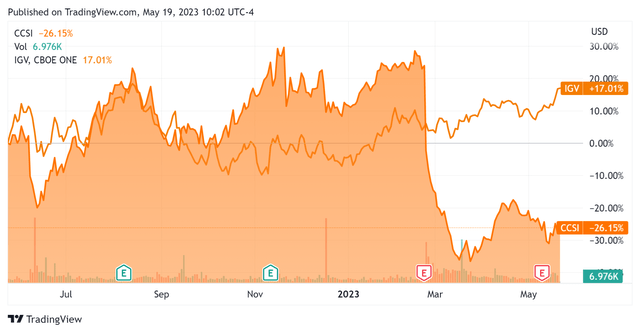

In the past 12 months, CCSI’s stock price has dropped 26.15% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) rise of 17.01%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $111.3 million in cash and equivalents and $794.3 million in total debt, none of which was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $40.2 million, of which capital expenditures accounted for $31.7 million. The company paid $19.8 million in stock-based compensation in the last four quarters, the second-highest figure in the last eleven quarters.

Valuation And Other Metrics For Consensus Cloud

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

3.8 |

|

Enterprise Value / EBITDA |

8.5 |

|

Price / Sales |

1.9 |

|

Revenue Growth Rate |

2.1% |

|

Net Income Margin |

19.1% |

|

EBITDA % |

44.8% |

|

Market Capitalization |

$681,400,000 |

|

Enterprise Value |

$1,380,000,000 |

|

Operating Cash Flow |

$71,210,000 |

|

Earnings Per Share (Fully Diluted) |

$3.48 |

(Source – Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

CCSI’s most recent Rule of 40 calculation was 46.9% as of Q1 2023’s results, so the firm has performed well due to high EBITDA results, per the table below:

|

Rule of 40 Performance |

Calculation |

|

Recent Rev. Growth % |

2.1% |

|

EBITDA % |

44.8% |

|

Total |

46.9% |

(Source – Seeking Alpha)

Commentary On Consensus Cloud

In its last earnings call (Source – Seeking Alpha), covering Q1 2023’s results, management highlighted its record revenue and fax volumes during the quarter.

However, the firm sees ‘slow decision-making by our largest prospects and slow implementation by those under contract. This has been driven by uncertainty in the economy and labor shortages that exist, especially in the health care space.’

Leadership believes this environment will continue throughout 2023.

Employee headcount has grown, but management is still seeking ways to reduce its non-employee costs as operating income continues on a downward trend.

The firm continues to execute its sales realignment into strategic sales and direct sales and has hired ‘new leadership for our direct sales team and are closing in on our targeted staffing level.’

Management said monthly churn rate was 1.4% during the quarter, down from a previous 2% result, with the company’s revenue retention rate being 102% and inline with expectations.

Total revenue for Q1 2023 rose only 0.7% year-over-year and gross profit margin fell 2.6 percentage points.

Selling, G&A expenses as a percentage of revenue increased by 3.5 percentage points and operating income fell sharply by 12.4% year-over-year.

Looking ahead, management reaffirmed its guidance for 2023 revenue of $380 million at the midpoint (4.9% growth rate, if achieved) and said it expects to generate adjusted non-GAAP EPS of $5.08.

The company’s financial position is moderate, with ample liquidity and some long-term debt. Free cash flow was over $40 million in the last four quarters.

Regarding valuation, the market is valuing CCSI at an EV/Sales multiple of around 3.8x.

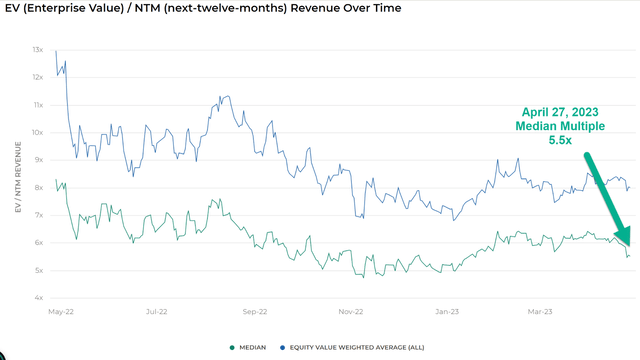

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.5x on April 27, 2023, as the chart shows here:

EV/Next 12 Months Revenue Multiple Index (Meritech Capital)

So, by comparison, although CCSI is not strictly a SaaS company, it is currently valued by the market at a discount to the broader Meritech Capital SaaS Index, at least as of April 27, 2023.

Risks to the company’s outlook include an economic slowdown that appears to be underway, reduced credit availability which may affect customer/[prospect spending plans and lengthening sales cycles which may reduce its revenue growth potential in the near term.

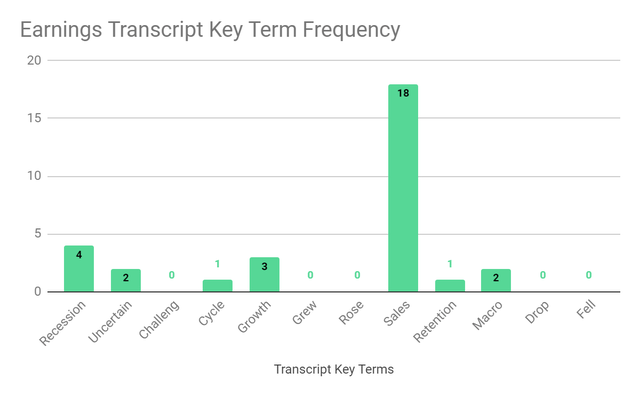

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Term Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management cited ‘Recession’ four times, ‘Uncertain’ two times, and ‘Macro’ two times.

The negative terms refer to management expectations of a 2023 recession and current macro uncertainty with the potential to weigh negatively on its business results.

In the past twelve months, the firm’s EV/EBITDA valuation multiple has varied widely and dropped a net of 9.6%, as the chart from Seeking Alpha shows below:

EV/EBITDA Multiple History (Seeking Alpha)

A potential upside catalyst to the stock could include a drop in cost of capital, reducing downward pressure on its valuation multiple.

However, with continued rising employee headcount and deteriorating operating income as we head into a likely recession, until management can reignite better revenue growth and stop the drop in operating income, I’m Neutral [Hold] for CCSI in the near term.

Read the full article here