I will never forget coming home from middle school, running up the steps to my house, and picking up the package left outside the door. It was GTA IV. It was the first Grand Theft Auto game I had ever played, and I will never forget how, unlike every other game it was… I felt like I was playing out a Hollywood movie. I missed the boat on Take-Two Interactive’s (NASDAQ:TTWO) stock because I was too young, however, let’s examine if this stock is still worth picking up…

Company Background

Take-Two Interactive is a video game developer that publishes titles through Rockstar Games, 2K, Private Division, T2 Mobile Games, and Zynga. The company sells its games physically and digitally on PCs, consoles, and mobile devices. Take-Two is widely regarded as one of the best, if not the best, video game developer in the world.

Q4-23 Results

Let’s take a look at some of the data from the company’s recent earnings report.

Higher Costs

Take-Two’s cost of goods sold was up a whopping 207% YoY, driven by a $465 million impairment charge regarding Zynga. Hiring of new developers for unreleased (and canceled games) also contributed to the company’s higher cost of goods sold.

Continuing down the P&L line, operating expenses were up 130%, primarily the result of costs associated with the Zynga merger.

Next, marketing expense was up 204% YoY. The company primarily attributes this to a change in the way they market their games. For example, rather than spending a large percentage of total game marketing leading up to launch, President Karl Slatoff stated, the company spaces the cost over time now.

Lastly, the company posted a GAAP loss of $(610) million or $(3.62) per share for Q4-23. For FY-23, Take-Two posted a GAAP loss of $(1.12) billion or $(7.03) per share. Unfortunately for shareholders, part of the huge loss for FY-23 stems from excessive stock-based compensation.

So, What Does All This Mean?

Overall, Take-Two delivered mixed results. I think investors will interpret these results differently depending on how they view the future of the company. Specifically, it seems to me that:

Take-Two, with (1) the acquisition of Zynga, (2) its previous quarterly reports, and (3) its future guidance, has intentionally changed its business model from lower-revenue/higher margins to higher-revenue/lower margins. From management’s actions, it appears they hope the latter strategy will be more lucrative despite the reduction in margins. In other words, according to their calculation, perhaps they believe they will generate higher free cash flow using this method.

It is an interesting choice to make because, on the one hand, the legacy games are delivering great results (think the GTA and Red Dead Redemption franchises), but on the other hand, expenses, have ballooned. The company’s Zynga merger, hiring of new developers, marketing spend, stock-based compensation, inflation, taxes, and interest payments are all driving up costs and driving down margins.

Looking forward, the company expects to reach $8 billion in net bookings in FY25, calling it a “highly anticipated” and “high profitable” year. Analysts have interpreted this as a hint GTA VI, the company’s most prized possession, might be released that year. I calculated the company’s past decade CFFO/revenue ratio to be an average of 21%. However, in the earnings call, management expects their CFFO/revenue ratio to be only 12.5% ($1 billion / $8 billion) despite 2025 being a “highly profitable” year (presumably due to hugely popular titles expected to be released).

To me, this is proof of my theory that the company is focused on revenue at the expense of margins. For example, if 2025 is supposed to be a record year for the company, shouldn’t the CFFO/revenue margins be higher? Management stated part of the higher costs in upcoming years is comprised of tax and interest payments, but I believe the primary culprit is the higher costs associated with bloat from the Zynga merger and developmental costs for upcoming games. As such, I believe it is prudent to conclude 12.5% CFFO/revenue margins, as opposed to 21%, to be the new norm.

Note: Maybe management is stuck in the low inflationary environment mindset that investors will continue to value companies using P/S ratios instead of P/E ratios. This switch in their business model would then benefit them greatly as the market would value the company higher (based on higher revenue, regardless of margins) and increase the value of their stock-based compensation.

Valuation

Let’s take five, come back, and calculate Take-Two’s (nice pun, I know) fair value using a discounted cash flow model based on the company’s guidance and my own estimates. It is important to note, no two investors will get the same valuation. This is an art, as much as it is a science.

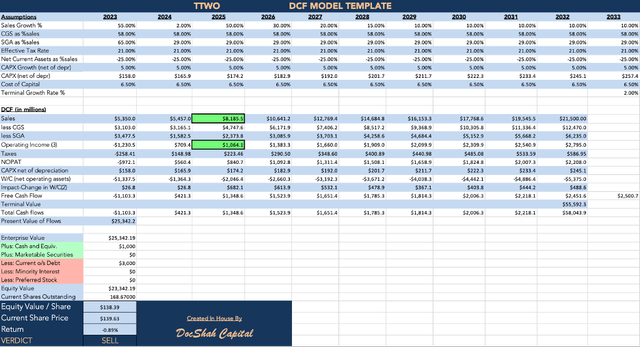

Sales

The company’s sales growth reflects management’s guidance until 2025 to account for the secret-massive titles rumored to be released, then gradually reduced over time. You will notice in 2025, I have accounted for management’s revenue of $8 billion in net bookings and $1B in operating income

Note: I know operating income is different from operating cash flow. For the purpose of this valuation, using $1B in operating income is perfectly fine.

Expenses

I reduced the company’s gross margins to 42% to reflect its recent degradation and increased SGA expense to reflect a reduction in operating margins to 12-13% going forward.

Tax Rate and Net Current Assets

The tax rate is set to 21% per the TCJA, but of course, this fluctuates depending on deferred tax assets/liabilities. Net current assets as a percentage of sales is set to -25%, which is based on historical averages. The company’s deferred revenue account balance remains elevated as a result of its business model, which causes net working capital to be negative.

Capital Expenditures

CAPX and CAPX growth rates are set by historical averages and forward guidance.

Cost of Capital and Terminal Value

The company’s WACC was hand calculated to be 6.5% and the TV is set to 2% to be conservative.

DocShah’s TTWO DCF

TTWO DCF 2023 (Author, DocShah Capital)

Based on company guidance and my own estimates, the stock is priced at exactly what it is worth. This is extremely rare and probably the only time I have seen a valuation tool be so exact, coincidentally. DCFs can be serendipitous when the future you predict happens to perfectly match reality.

Note: These projected future cash flows could be underestimating the impact of GTA VI. This was done so in order to be conservative.

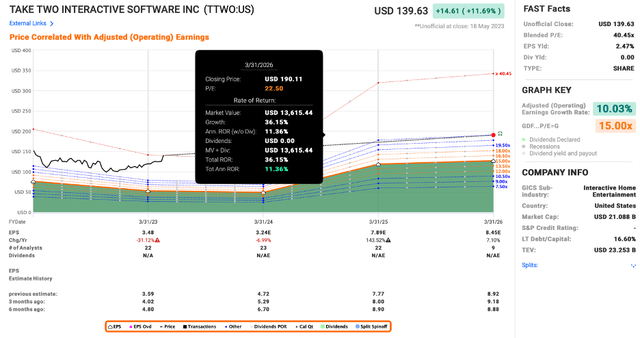

FastGraphs

TTWO Earnings Projections (FastGraphs)

FastGraphs values Take-Two significantly higher based on forward EPS estimates. Analysts expect the company to make $8.45 per share in 2026. Take-Two’s 20-year historical normal P/E has been about 21.5x earnings. If the market assigns that multiple to 2026 earnings, then the stock would change hands at $182 per share, which represents 31% upside from current levels.

Here is how the market would value the stock at different multiples:

- 21 P/E = $177 per share, 27% gain

- 18 P/E = $152 per share, 9% gain

- 15 P/E = $126 per share, (9)% loss

- 12 P/E = $101 per share, (27)% loss

My Final Thoughts on Valuation

The reality is Take-Two has the best asset class in all of gaming. GTA V alone, for example, is the single greatest selling piece of entertainment in history. Furthermore, it is a 10-year-old game that still generates millions of dollars in revenue, which is unprecedented. If you combine that with the other massive AAA, blockbuster smash hit titles like Red Dead Redemption, NBA 2K, WWE, etc, it is clear no gaming company is in the same league as Take-Two. The market recognizes Take-Two’s strength and has applied a growth level P/E to its stock.

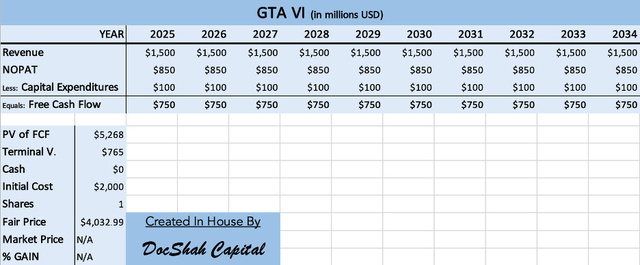

GTA VI

Here is how I think of roughly valuing GTA VI:

GTA VI Value (Author, DocShah Capital)

GTA V generated roughly $1B per year in revenue, when games were priced at $60. In this generation of console gaming, games are priced at $70, which represents a 17% increase. Therefore, all things equal, GTA VI would generate about $1.2B in revenue. When we consider that microtransactions, the consistent part of Take-Two’s earnings, will also be priced higher on average, $1.5B per year becomes a reasonable estimate of annual revenue generated by GTA VI.

Next, if we assume 50-60% margins, $100 million in capital expenditures, a 7% discount rate, 2% terminal value, and the rumored $2B of costs creating the game, then the value of GTA VI standing all by itself is $4B. Note, there are a lot of safe assumptions being made… the game could be worth even more than that.

If we put this into perspective, Take-Two’s entire market cap is $21B. Therefore, GTA VI currently represents 20% of Take-Two’s valuation. In other words, the other 80% of the Take-Two’s valuation is the sum of all its other games.

So, the obvious question is: Are all of Take-Two’s other games worth $17B? If they are, then the company is fairly priced. If the games are worth more, then the company is underpriced. Lastly, if the games are worth less, then the company is overpriced.

I believe Take-Two’s current catalogue of games and upcoming games are worth more than $17B. For example, RDR3 is likely worth $2B, based on RDR2 cash flows. NBA 2K and WWE are yearly releases, both probably worth about $500 million (50MM per year) based on their sales. If you factor what Take-Two paid for Zynga ($12.7B) and reduce it by the impairment recognized by the company, Zynga is still technically worth roughly $12B. Therefore, simply adding up RDR3 + NBA 2K + WWE + Zynga = about $17B.

The Characters Are Assets Too

Take-Two has so many more assets on the balance sheet than what meets the eye. The company could be undervalued when looking at the potential value of the characters on the balance sheet… aka the intangibles. Take-Two’s characters and video games are iconic and could transition over to Hollywood films or Netflix series’. In fact, I wrote this specifically in my last article on Take-Two:

“Interesting side note: Peter Lynch once talked about hidden assets on a balance sheet. The example he used was Disney and its plethora of iconic characters which become monetized by feature films, theme parks, merchandise, etc. At the time, most investors did not calculate the true value of Disney’s assets since the characters were hiding (in plain sight) on the balance sheet waiting to be brought to life. Take-Two has an outstanding cast of characters that might transition over to mainstream entertainment in a similar fashion one day. Considering Mickey Mouse alone is worth more than some companies entire market cap, Take-Two might have a similar avenue to generate additional profit.”

Risks

There are numerous risks to consider when purchasing shares of Take-Two Interactive.

- The Zynga merger does not realize synergies and results in further impairment

- Five games make up 83% of the revenue

- Video game sales do not recover to pandemic levels in the near future

- GTA VI becomes a poorly received game

- Inflation reduces margins even further than expected

- For the company’s set of risks, please click here

Takeaway

Take-Two is an interesting case depending on how you view the company. If you believe its strategic change to switch from lower-revenue/higher-margins to higher-revenue/lower-margins will pay off, then the company could be undervalued. Otherwise, it would be overvalued as margins erode profitability faster than revenue can produce enough cash flows.

Furthermore, my DCF might be underestimating the impact of GTA VI (in order to be conservative) and therefore, the stock could be undervalued. Lastly, when looking at the value of all assets, it appears the market might not be valuing them to their full potential.

Personally, I do not own shares as there are better risk/reward opportunities in the market. However, I would rate Take-Two a buy for investors who have a long-term horizon (10+ years) and a hold for investors who have short-term horizons.

Read the full article here