Executive Thesis

I recently covered TripAdvisor (TRIP) and estimated it was trading at a slight discount to intrinsic value, though macroeconomic uncertainty weighed on the future prospects of this consumer discretionary company. I wanted to take a closer look at the TRIP holding company, Liberty TripAdvisor (NASDAQ:LTRPA) (LTRPB), to see if this may be a better investment option than the subsidiary. I will assume that the reader is familiar with TRIP and will mainly focus on the capital structure of LTRP. Of note, LTRP has no significant holdings other than TRIP with an approximately 21% equity stake and 57% voting interest. I believe the current capital structure is similar to buying $20 March 2025 call options on TRIP, with significant upside implied if TripAdvisor can perform, but with the risk of total loss of capital if it cannot.

Cheaper Than It Looks

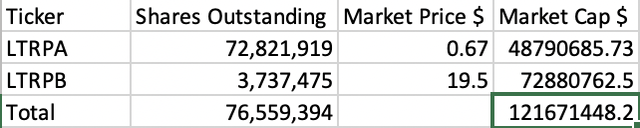

One thing that strikes me as interesting is if you take a cursory glance at the market capitalization, the total at time of writing is listed at around $120 million. This technically isn’t the price you’re paying for the company. To get the market cap, we multiply the A shares and B shares by their respective shares outstanding. The main difference between the two is that the B shares are thinly traded, mostly held by insiders, and have 10x the voting rights of the A shares. Pretty bizarre then, that you can currently buy 1 share of LTRPA for around $0.60 and one share of LTRPB for $19.50.

This Writer, Extrapolated from Company Data

As we can see above, LTRPB makes up a disproportionately low percentage of ownership but a high percentage of market capitalization. If we multiply the total A and B shares outstanding by the current market price of LTRPA, we find that by buying A shares, you are effectively paying about $50 million for the company.

The Bizarre Capital Structure

It seems like any time you want to get involved with a Liberty-related company, you need to be ready to dive into an odd capital structure. I think this provides opportunity, because many people will quickly throw the company in the too difficult to understand pile and not take a position. The easy part is the assets, with approximately $30 million in parent company cash and 29.2 million TRIP shares. Next, let’s dive into the debt.

Variable Prepaid Forward “VPF”

The first liability to look at is the $51 million TripCo variable prepaid forward contract. In short, it is a way for a company to raise cash with shares immediately, but the actual selling of the shares will not be officially finalized until a later date. This has some tax advantages and also offers some protection if there is a substantial loss in share price over the time period.

In LTRPA’s case, TRIP shares were pledged for cash, which when it matures will have a total liability value of $57 million. There is some downside protection though, so only 2.4 million shares are pledged as collateral for the contract maturing in November 2025, as there is a negotiated floor price of $23.64.

The Exchangeable Debentures

The company has $330 million outstanding in 0.5% senior exchangeable debentures due 2051, with a TRIP conversion price of $69.78. With the $30 million in parent company cash on the balance sheet, coupon payments on these debentures should not be an issue. Though they are long-dated, the debt holders appear to have the option to require the purchase of the debentures starting in March 2025. This may present a problem for LTRPA, as the value of their TRIP shares have dropped dramatically. If all debenture holders request payment in 2025, this would theoretically require sale of 20 million TRIP shares which could reduce total holdings to less than 10 million shares, and result in a potential loss of their controlling stake.

The Preferred Stock

There are 187,714 preferred shares outstanding as of the MRQ with a par value of $1000. The shares pay an 8% coupon annually in March, and can be in either LTRP stock or cash. These have standard preferred rules such as if a coupon is missed it will be added to the final redemption price of the shares. These preferred shares will mature in March 2025.

Putting it all Together

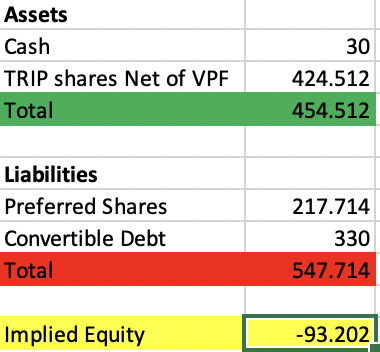

It is going to be a key few years for LTRP as all of their TRIP backed debt and preferred shares are maturing in 2025. If we take cash and TRIP stock net of VPF obligations at the current market price of $15.84, and subtract other obligations, the current NAV sits at around -93 million. Of note, in my calculation below, I added in the preferred coupon payments over the next 2 years to the preferred share liability section.

This Writer, Extrapolated From Company Data

Any TRIP price above $20 would swing the NAV positive, and if for example TRIP can reach the 2021 high of $60/share, NAV would swing all the way to $1 billion. I am skeptical that the company can do this in the near term though, considering the higher interest rate environment, looming macroeconomic slowdown, and discretionary spending nature of the company.

Conclusion

Buying LTRPA is similar to buying a call option on TRIP with a $20 strike price and an expiration in March 2025. If TRIP can return to $25/share before 2025, the implied equity calculation above would value LTRP at around $150 million, indicating 200% upside for investors in LTRPA shares. If TRIP cannot perform in the near term, though, LTRPA investors risk total loss of capital if debenture holders request payment when they have the option to do so and refuse to assist with refinancing. As I had previously calculated fair value for TRIP at around $21/share or $3 billion for the company, I don’t find investing in LTRPA shares to provide a fantastic risk/reward profile at this time. That being said, I did buy a small speculative position before performing my full analysis of the holding company. Risk averse investors interested in the company may prefer TRIP shares over LTRPA.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here