Investment thesis

Datadog (NASDAQ:DDOG) is a relatively young company, demonstrating a stellar revenue growth rate and solid margins. The company has vast opportunities to sustain strong double-digit growth rates, but the extent of uncertainty is rather high for me to invest. I might invest in the future, but my valuation analysis suggests that there is little upside potential at the moment. Therefore, I will wait on the sidelines to see how the next few quarters will unfold.

Company information

Datadog is a software-as-a-service [SaaS] company offering customers observability and security solutions for cloud applications with built-in machine learning. According to the latest 10-K report, the company’s platform integrates and automates infrastructure monitoring, log management, and user monitoring for Datadog’s customers’ entire technology stack.

The company’s fiscal year ends on December 31. The company operates as a single reportable segment and disaggregates its revenue by geographic area. Revenue generated in North America represented more than 70% of the total in FY 2022.

Datadog’s latest 10-K report

Financials

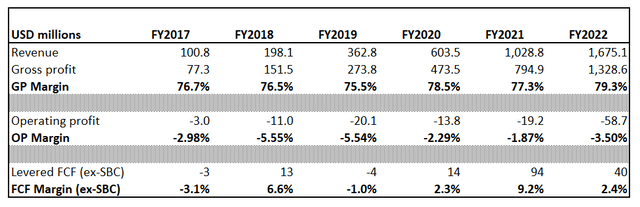

Datadog went public in September 2019, therefore we have historical financials available only for the previous six years. I usually zoom out to analyze the decade, but we have what we have.

Author’s calculations

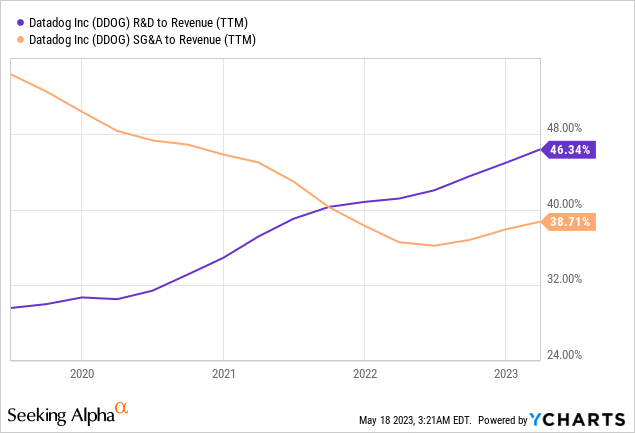

What I like here is the immense revenue growth at about 60% CAGR with gross margin expanding as the business scaled up. What is also crucial for me is that the company is not a cash burner and demonstrated the ability to generate positive free cash flow [FCF] even after the stock-based compensation [SBC] deduction. The operating margin has been stagnating because the company fueled its growth by investing heavily in R&D and SG&A, representing a notable portion of its revenues.

As we can see from the above chart, the SG&A portion is decreasing as the business grows and I expect this favorable trajectory to sustain. I am not concerned much about the extensive R&D given the company’s early stage of the business cycle, and as long the company maintains its impressive growth pace.

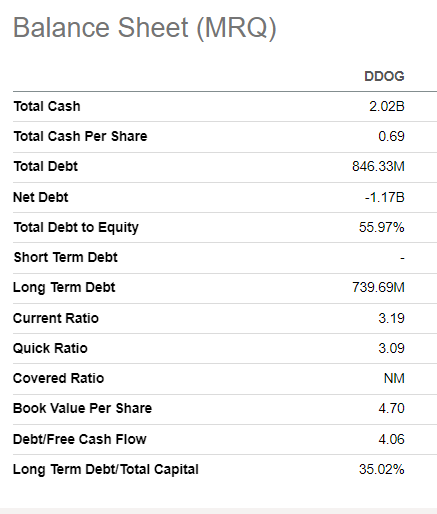

Generating positive cash flows enables the company to support its balance sheet, which I consider to be in good shape. The company is in a net cash position with high liquidity ratios. Leverage looks to be conservative as well, substantially below equity. Therefore, the company is strong enough, in my opinion, to weather short and mid-term storms, which can happen given the current harsh macro environment.

Seeking Alpha

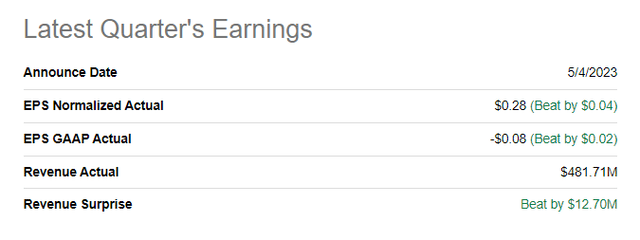

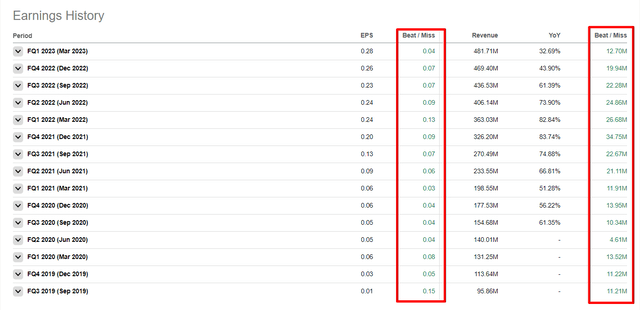

If we narrow down to recent quarters’ financial performance, the company released its latest earnings on May 4, delivering above-the-consensus results.

Seeking Alpha

Quarterly revenue was $481.7 million, which was 33% higher than a year ago and about 3% higher sequentially. The company’s customer base grew almost 30% YoY, including customers who joined as part of the Cloudcraft acquisition. The company remained on a solid free cash flow track, generating about $13 million levered FCF ex-SBC. What I also see as a very positive sign is that the company delivered expanded reach compared to a year ago. According to the company’s CEO, Olivier Pomel, the share of customers using multiple products increased:

As at the end of Q1, 81% of customers were using two or more products, in line with last year. 43% of customers were using four or more products, up from 35% a year ago, and 19% of our customers were using six or more products, up from 12% last year.

What also impressed me was the stellar retention rate. The trailing 12-month dollar retention rate was at a 130% level, meaning increased usage and adoption of more products. Another important metric for a SaaS company, the remaining performance obligations [RPOs] rose 33% YoY, suggesting a solid revenue pipeline.

Last but not least, I would also like to underline the company’s perfect earnings history with never missing consensus estimates during several recent quarters since the company went public. For me, it is a strong positive signal, though any winning streak will most likely end at some point in the future.

Seeking Alpha

I believe DDOG’s growth rate has been impressive, though it’s decelerating given the current harsh environment where customers are forced to cut spending, including IT spending. But I believe these headwinds are temporary, and growth rates will bounce back when macro environment conditions become more favorable for customers to increase spending.

Valuation

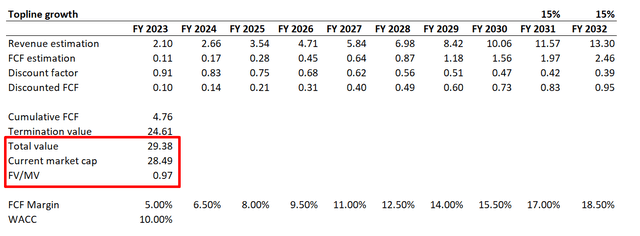

Datadog is an aggressive growth company, and we need to use an adequate valuation method to estimate the fair value. That discounted cash flow [DCF] approach would be perfect for a company like Datadog. I will start with underlying assumptions, the discount rate to be specific. Valueinvesting.io estimates Datadog’s WACC at approximately 10%, which I consider fair. I have earnings consensus estimates for future cash flows, which I should multiply by the FCF margin. As we have seen in the “Financials” section above, the company’s FCF margin is not stable yet and very volatile in recent years. Given the positive outlook, I believe a FCF margin of 5% for FY 2023 would be somewhat conservative. I expect the FCF margin to expand by 150 basis points yearly as the business scales up.

Author’s calculations

Given the above assumptions, my estimation of the business’ fair value is close to the current market cap with a slight 3% upside potential. Given the high uncertainty of future cash flows and FCF margin which is not stable yet, I think that the current share price level does not look attractive from the risks-to-return standpoint.

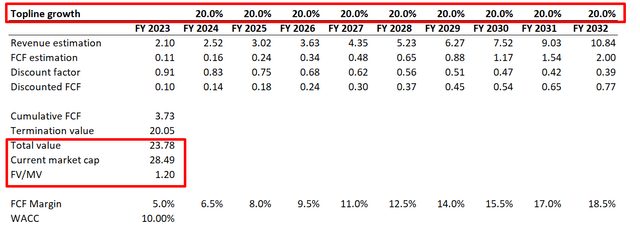

The calculations above show the CAGR is projected to be about 23% over the next decade. Let me look at the fair value if we decrease CAGR to 20% with other assumptions remaining the same.

Author’s calculations

As you can see, the model is susceptible to the topline growth rate. A 20% CAGR over the decade is also very aggressive, and under this assumption, the DCF suggests that the stock is 20% overvalued. There is also vast uncertainty regarding the pace of EPS expansion, therefore, I believe that valuation does not look favorable at current levels.

Risks to consider

Datadog is an aggressive growth company with many positive expectations incorporated into the stock price. Delivering aggressive growth over the long run is a big challenge, and history shows that sustaining high double-digit growth over decades is a rare phenomenon. Therefore, there is a very high risk that the company might fail to support the growth trajectory which is priced at the moment. Any downgrades in future earnings will hit the stock price, of which I am highly confident.

The company also faces fierce competition from Splunk (SPLK) in full-stack monitoring & analytics [FSMA], where Splunk is considered the leader. I believe both companies’ total addressable market is by far higher than last year’s revenue of $5 billion combined. Still, competition brings additional uncertainties regarding the pace of sales growth for DDOG. For me, this is a significant risk as well.

Also, as for all software companies, DDOG faces numerous technology obsolescence and cybersecurity risks. Any data leaks of successful external cyberattacks will severely hit the company’s reputation and lead to unexpected costs. It will also likely lead customers to look for alternative service providers, which can be perceived as more attractive and safe if DDOG fails to innovate and protect data.

Bottom line

Datadog demonstrated impressive revenue growth in recent years and positive cashflows, which is rare for a young company like DDOG. I believe that the company will continue to grow, but the level of uncertainty regarding the extent and pace of the growth is vast. I would have invested if my valuation indicated a more considerable upside potential, but I give the stock my neutral opinion at the current level. I have high conviction that there will be more favorable entry points in the nearest future given overall risks for the stock market due to the looming recession and credit crunch.

Read the full article here