The saddest aspect of life right now is that science gathers knowledge faster than society gathers wisdom.”― Isaac Asimov.

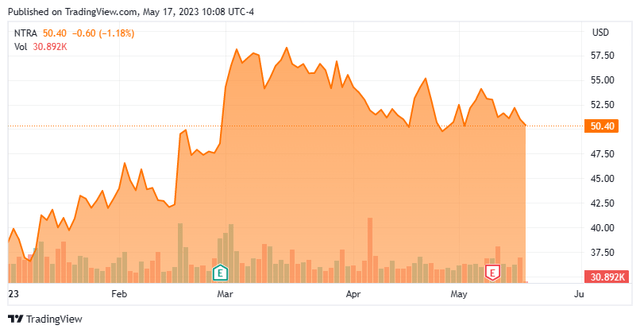

Today, we put Natera, Inc. (NASDAQ:NTRA) in the spotlight for the first time in nearly a year. The company continues to put up solid revenue growth. However, Natera seems far away from profitability, and its cash burn rate should continue to be a concern to investors.

Despite this, NTRA stock is up over 30% in 2023 year to date. Natera is currently universally loved in the analyst community. Are the shares overdue for some profit taking, or will they continue their rise? An analysis follows below.

Seeking Alpha

Company Overview:

Natera, Inc. is based in Austin, TX. This genetic testing concern has seven offerings in women’s health, two oncology tests, three organ health assays, and an out-licensed cloud-based platform to conduct the analysis. Natera leverages its molecular and bioinformatics technology to detect proclivity to a plethora of afflictions. The stock currently trades around $51.00 a share and sports an approximate market capitalization of $5.8 billion.

May Company Presentation

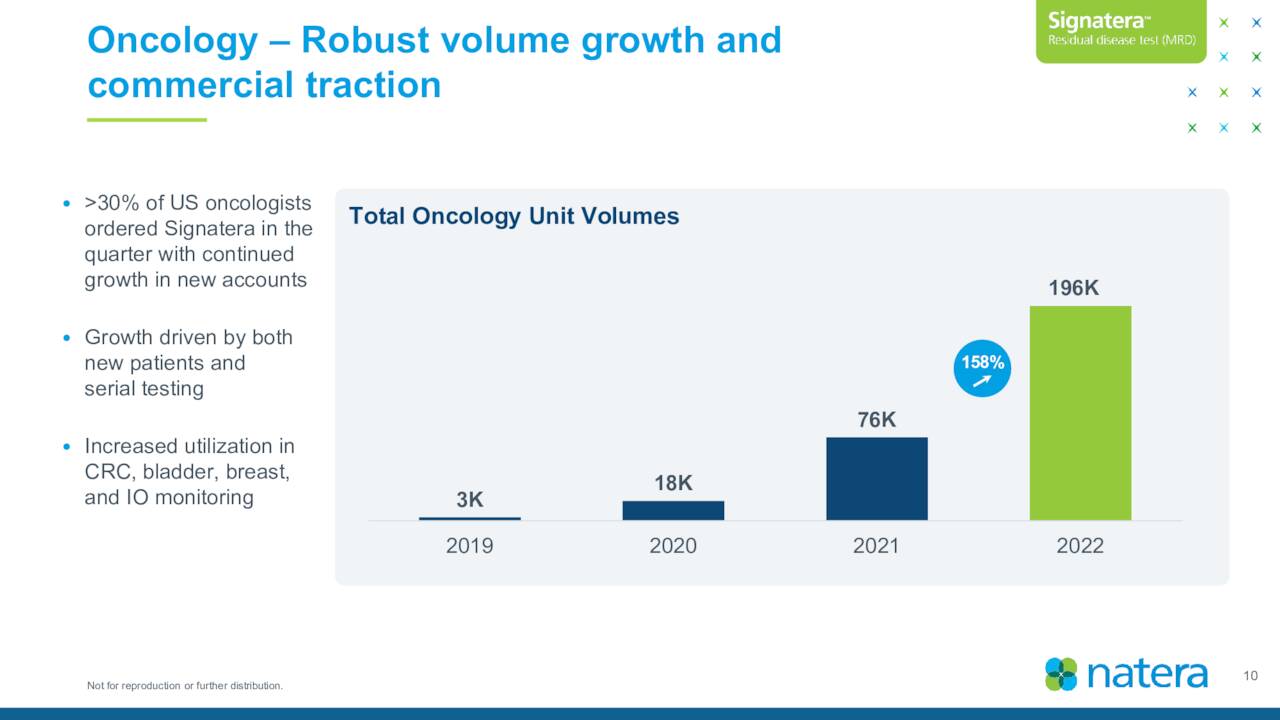

The company’s technology platform allows it to read DNA at a very granular level. The company started developing and commercializing various tests for women’s health. Natera also started to add new tests in the field of oncology, first introducing a molecular residual disease [MRD] in 2017. This was followed by a product called Altera in 2021. This is a genomic test that highlights alterations and biomarkers in a patient’s tumor that can be employed by oncologists to instruct treatment decisions.

May Company Presentation

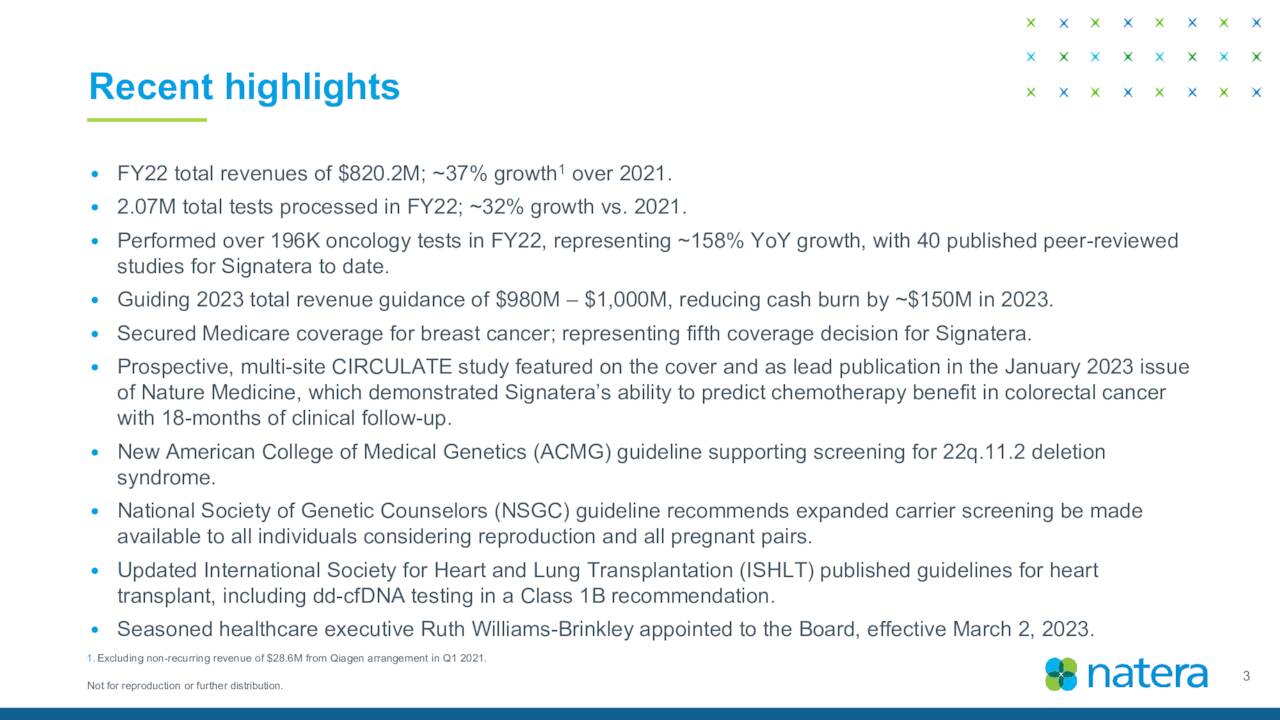

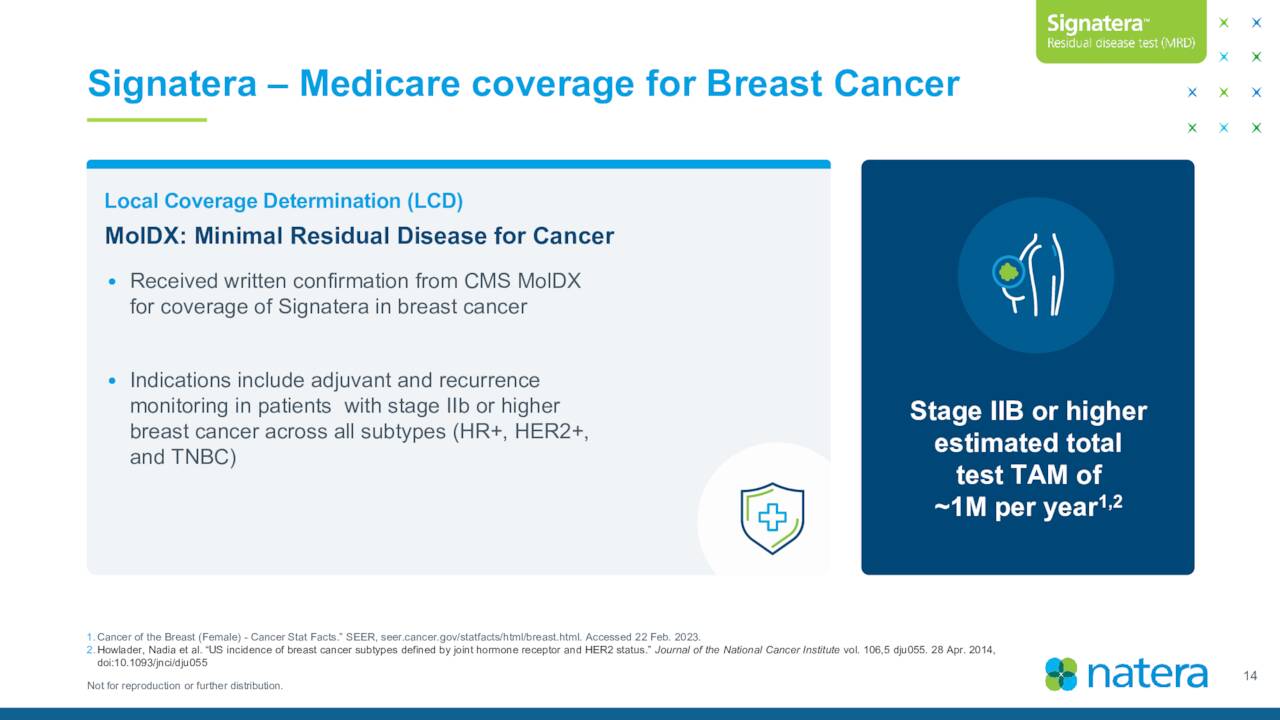

The company and stock got a nice boost in mid-February of this year after management announced that its Signatera cancer test had met Medicare coverage criteria for breast cancer screening.

May Company Presentation

The other high growth area the company has recently targeted is organ health. Natera launched its Prospera Kidney test in 2020, followed by the Prospera Heart and Lung assays in 2021.

First Quarter Results:

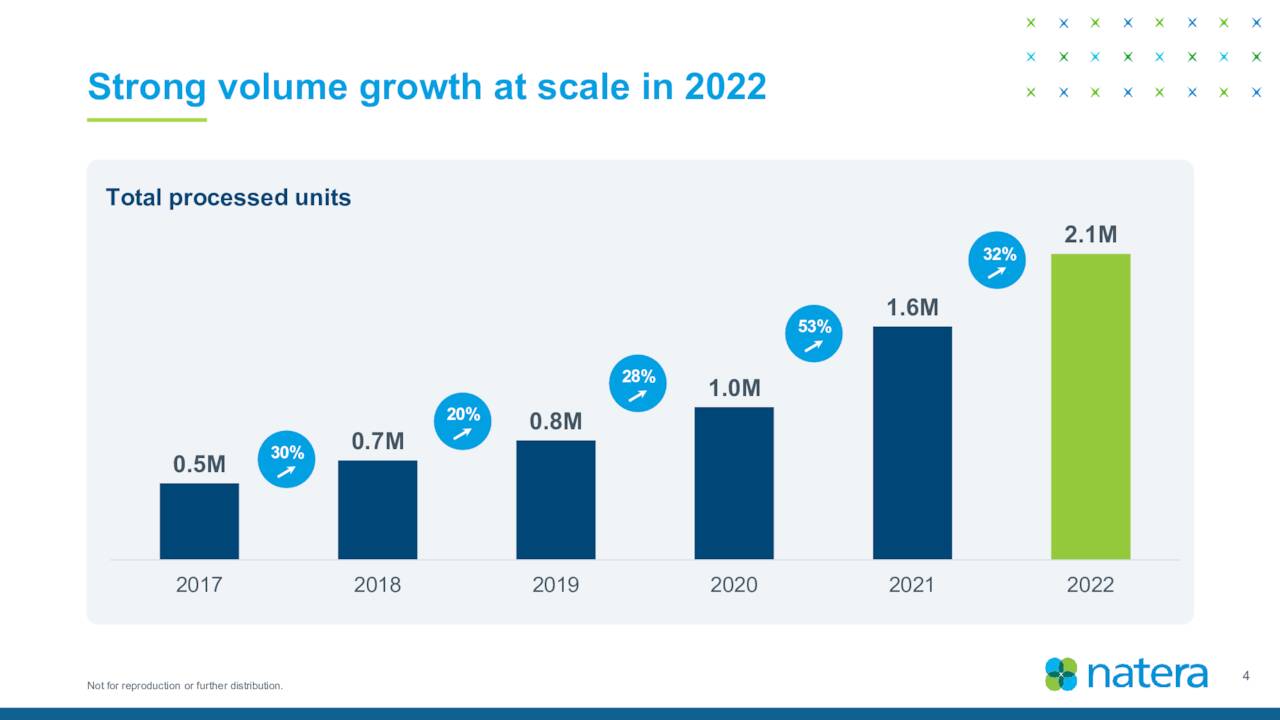

Natera reported its first quarter numbers on May 9th. The company had a GAAP loss of $1.23 a share, seven cents below the consensus. However, sales rose nearly 25% on a year-over-year basis to $241.8 million, some $14 million over expectations. Natera processed approximately 626,200 tests in the first quarter of 2023, up 28% from the same period in 2022. Oncology drove a good part of that growth as Natera saw 71,000 tests performed in this area, just over double the volume in 1Q2022.

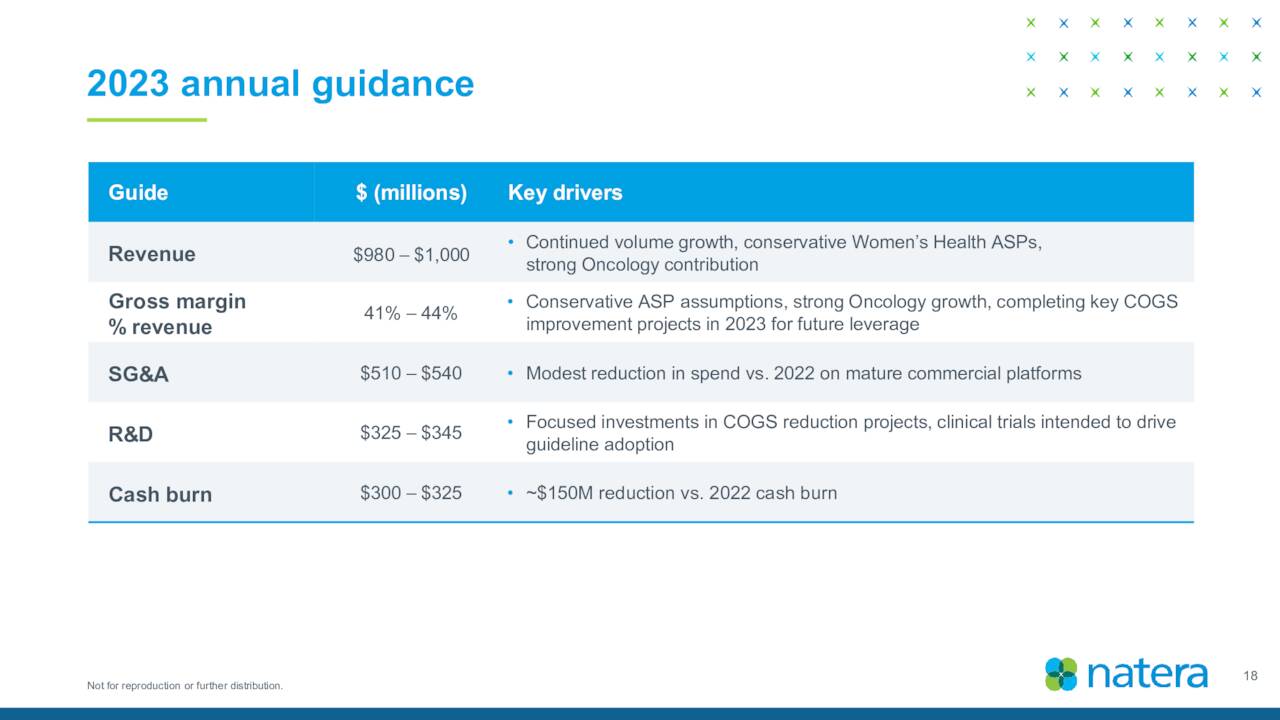

Management did bump up its revenue guidance slightly. Leadership now projects $995 million to $1.015 billion in total sales in FY2023, up from its previous range of $980 million to $1 billion.

May Company Presentation

Analyst Commentary & Balance Sheet:

Since first quarter results were posted, nine analyst firms including Goldman Sachs and Morgan Stanley have reissued Buy/Outperform ratings on the equity. Three of these ratings did contain slight downward price target revisions. Price targets proffered range from $66 to $85 a share.

Approximately five percent of the outstanding float in the shares is currently held short. Insiders continue to be consistent and frequent sellers of the equity. So far in 2023, they have sold just over $10 million worth of shares collectively. The last insider purchase in the stock was in May of last year in the high $20s.

May Company Presentation

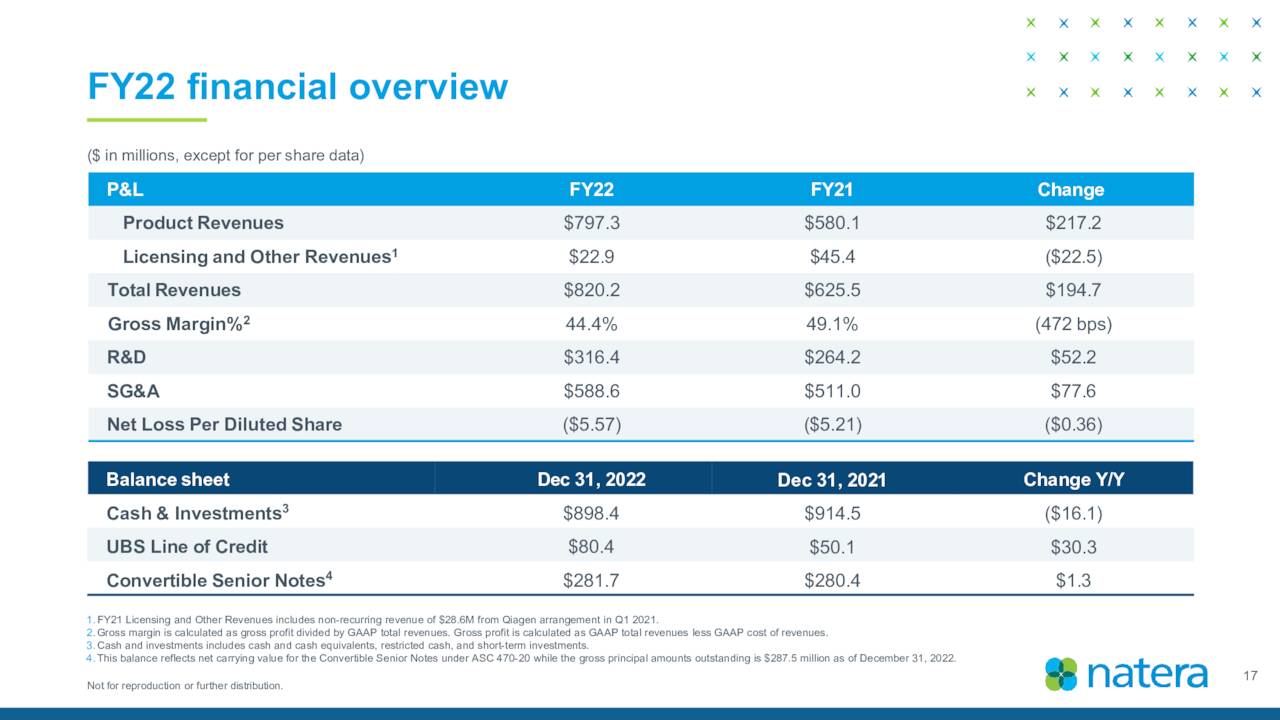

The company ended the first quarter of 2023 with just over $800 million in cash and marketable securities on its balance sheet against total outstanding debt of just north of $360 million. The company burned through just over $85 million worth of cash during the first quarter.

Verdict:

The current analyst firm consensus has Natera, Inc. losing $4.14 a share in FY2023 as sales rise in the low 20s to just over $1 billion. In FY2024, revenue is projected to increase by some 25% and losses cut to just over $2.60 a share.

Seeking Alpha

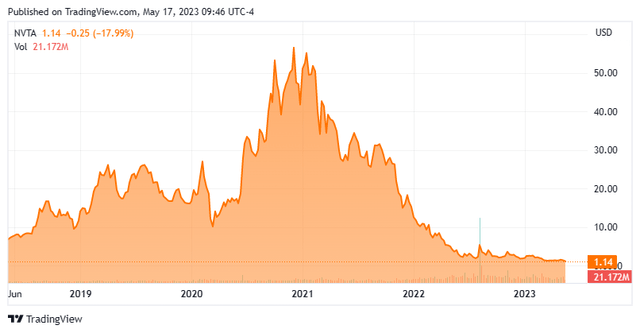

Natera reminds me somewhat of a genetic testing concern called Invitae Corporation (NVTA) which parlayed impressive sales growth to big stock market gains in 2020 and 2021. However, revenue growth unfortunately never resulted in profitability, and eventually the cash burn did in its shareholders as the company had to serially raise additional and dilutive funding. Invitae also had to eventually exit many “non-core” areas and engage in a major restructuring. The company’s ability to remain an ongoing concern is currently in doubt (as can be seen by the stock chart above). Granted, Natera’s management seems to have better focus on improving margins.

May Company Overview

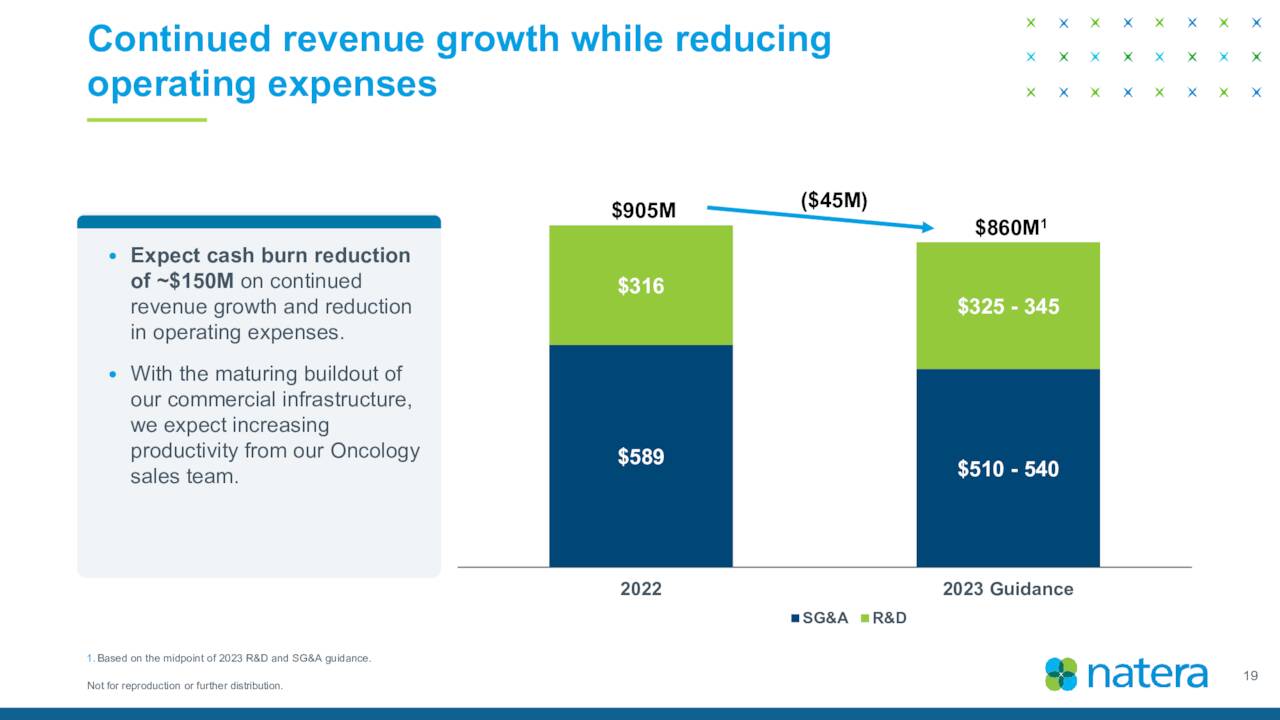

That said, management believes it will consume some $300 million to $325 million in cash overall in FY2023. This will bring down Natera’s net cash position by the of the year to approximately $225 million. This is an improvement in cash burn rate over FY2022, thanks to volume increases and projected expense reductions (see above). However, the company is likely to do another significant capital raise over the next year.

May Company Presentation

Therefore, until Natera, Inc. gets significantly closer to profitability, I will be avoiding the shares at these levels despite 20% plus sales growth and significant “love” from the analyst community.

If we knew what it was we were doing, it would not be called research, would it?”― Albert Einstein.

Read the full article here