Investment Thesis

Since Affirm Holdings, Inc. (NASDAQ:AFRM) put out its fiscal Q3 2023 results, the stock has jumped higher as a combination of the upwards revision of the low-end of its guidance combined with the general return of animal spirits to the stock market.

However, I make the case that even if Affirm declares that it’s on the path to profitability, Affirm’s version of profitability is far from ”actual” profitability.

Affir-Magination, Now Commoditized

Affir-magination pertains to the creativity that’s required to believe that Affirm will in time resume its climb higher. Even if animal spirits are now back in charge of the market, I simply don’t believe that Affirm has enough of a moat to become a compelling and profitable business.

Here’s the best way to think about it. I’m absolutely convinced that Buy Now, Pay Later (“BNPL”) is extremely attractive for consumers and has the potential to be highly lucrative for the fintech companies that reach both the required consumer distribution and have control over their cost basis.

The best way to explain my thesis is with a parallel example. Streaming is extremely expensive with questionable economics. And for a while, everyone was embracing the streaming wars. Why? Because companies believe that streaming, with their recurring revenues, could be a profitable venture.

However, more recently, companies discovered that streaming is only profitable either at scale, for instance, with Netflix, Inc. (NFLX) or as a value-add, for example, Amazon (AMZN) Video.

I believe the same dynamics will take place with BNPL. That’s why we see the likes of Apple Inc. (AAPL) embracing this endeavor, too. Because Apple has the reach and can provide BNPL as a value add to its ecosystem.

To repeat, it’s not that BNPL won’t continue to rapidly grow. It’s instead that Affirm will not be the vehicle that will benefit from this rapidly growing sector.

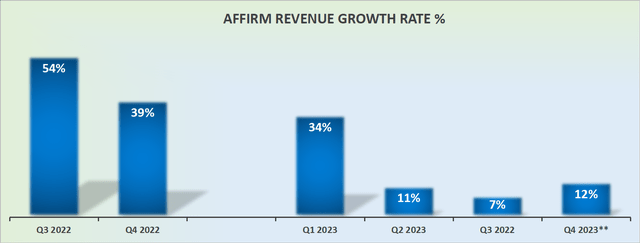

Revenue Growth Rates Fizzling

AFRM revenue growth rates

Affirm slightly raised its guidance for Q4 by approximately $100 million at the low end, and investors were quick to welcome this upward revised guidance.

However, I believe that in the best case, in fiscal 2024, Affirm’s growth rates are likely to be less than 20% CAGR and not much higher. More specifically, the days when ”growth investors” could count on Affirm as a high-growth business are now in the rearview mirror.

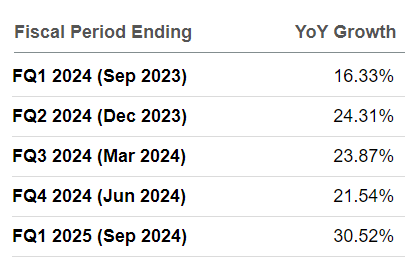

Note, my point of view is contrary to what analysts following the stock expect:

SA Premium

For analysts, the general consensus is that fiscal 2024 will see a significant increase in revenue growth rates.

However, I strongly believe that in the coming few months, we’ll see analysts downwards revising these assumptions on the back of a broad macroeconomic weakness.

The Bear Case is Found in the Profitability Profile

In this section, I’m going to highlight 3 different reasons why Affirm’s business model is far from being sustainably profitable.

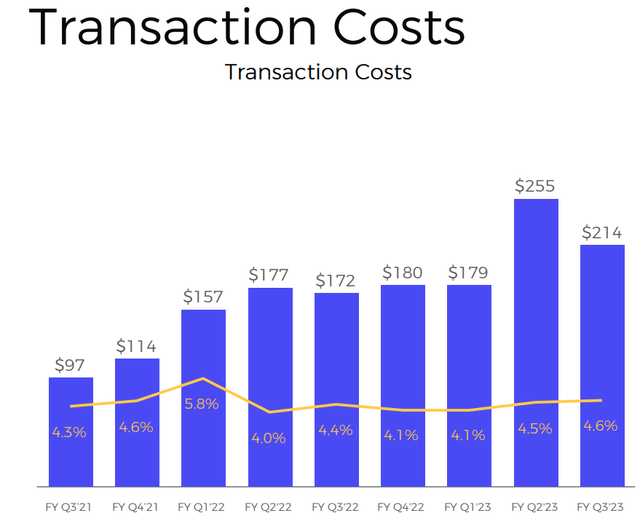

Consider Affirm’s transaction costs.

AFRM Q3 2022

Transaction costs in Q3 2023 were up 24% y/y. For me, there’s no cleaner metric to see that Affirm’s business model does not work. While revenues were up 7% y/y, Affirm’s transaction costs were up significantly more.

This means that Affirm is not benefitting from economies of scale. In short, there’s no positive operating leverage to Affirm.

Further, note Affirm’s guidance for Q4:

AFRM Q3 2023

At the low end, transaction costs are expected to increase by 36% y/y, while revenues are only expected to be up around 12% y/y.

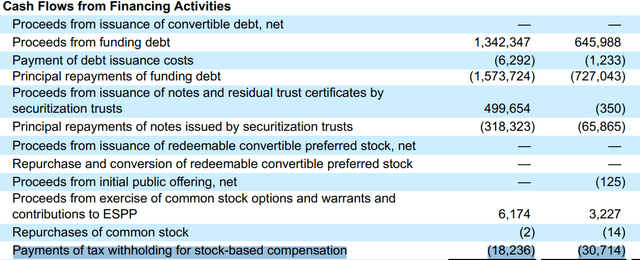

Next, Affirm’s Q3 2023 cash flows from operations were negative $11 million. This compares with $18 million in tax paid for Affirm’s SBC.

AFRM Q3 2023

Meaning that Affirm spends more in taxes for management’s stock-based compensation (“SBC”) than it brings in terms of cash flows from operations.

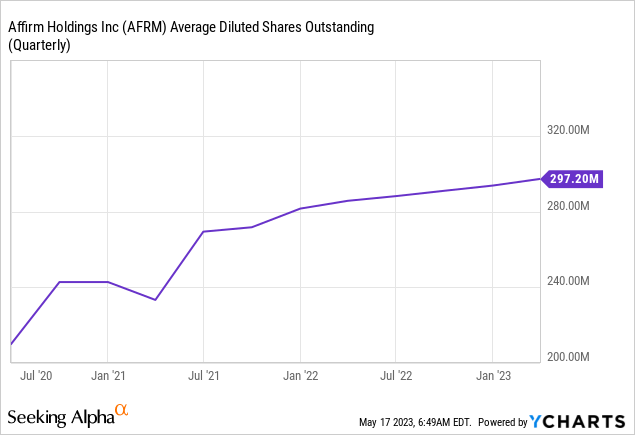

Finally, consider Affirm’s increasing shares outstanding count.

As an investor, you’d like to see the share outstanding remain relatively flat. Nobody wants to see their equity holdings diluted. Furthermore, as we look to fiscal Q4 2023, Affirm’s total share outstanding count is guided to increase by a further 4% y/y.

Now, one may declare that 4% y/y dilution isn’t such a big deal. However, I believe this is significant, particularly when the revenue growth rate is expected to be less than 15% y/y growth.

The Bottom Line

There was a time when it made sense to believe that Affirm Holdings, Inc., with its U.S.-based lead, could dominate the BNPL sector. But that insight is no longer accurate.

Meanwhile, I make the argument that once we take a more sober view of Affirm’s financials, there are more questions than answers. I continue to be bearish on Affirm Holdings, Inc.

Read the full article here