Investment Summary

Investors will find merit in dredging the rivers of healthcare service providers listed on the NYSE and NASDAQ. The waters are filled with long-term capital appreciators that offer rewarding economic characteristics to investors. In that vein, the investment case for Haemonetics Corporation (NYSE:HAE) continues its appeal to fundamental equity managers based on findings presented in this report. Notably, the company has revalued 42% higher since the original buy thesis presented in June last year.

The firm’s FY’23 numbers revealed there’s plenty of ammunition in the chamber to fuel economic earnings for shareholders this year. It booked organic revenue growth of 21% in FY’23 and nudged above the $1Bn annual revenue mark for the first time. It pulled this to 166% earnings growth and 8% growth in company FCF. Investors recognized 151% growth ROE last year, thus offering equity holders a sharp recovery from the pandemic era.

Not only that, as mentioned, expectations are tremendously high for the company. Investors are screaming into HAE’s equity, paying $42 for every $1 in future earnings at the time of writing, whilst the stock price is 12% above its 200DMA (and above all other moving averages as well). To me, this suggests there’s something here. HAE continues to rate higher, backed by:

- It’s exceptional plasma business that has demonstrated a remarkable turnaround from 2020

- Rewarding economic business characteristics that display high capital productivity and ongoing profit growth for investors

- These factors have rotated into additional market valuation over time

- Insulated offering in plasma that is fortified with the CSL relationship

HAE could do $1.27-$1.3Bn in revenues on my numbers and pull this to $160mm in post-tax earnings, and $3.20-$3.30 in EPS. Combined, there’s abundant data to suggest HAE is a buy for long-term capital appreciation. Value-orientated investors may scoff at the 42x multiple (that adjusts to 30x non-GAAP earnings, by the way) but this report demonstrates there is plenty of reason to be happy with that multiple. Net-net, I reiterate that HAE is a buy. This report will further illustrate the broad factors underlining the buy thesis.

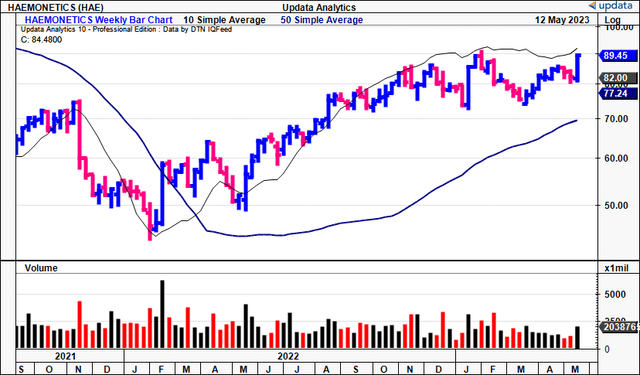

Fig. 1 – HAE Recovery off double-bottom, Jan 2022-date

Data: Updata

HAE driving value through plasma, hospital segments

Findings demonstrate that HAE’s plasma and hospital segments are key to attracting further investment. There are several catalytic factors underpinning each division. For one, the underlying markets in each corporate arm are both strong, more so now the pandemic has subsided. Further, idiosyncrasies between the portfolio add to the alpha opportunity.

Key facts

The key facts underpinning the reiterated buy thesis include the following:

1. The major driver underlining plasma top-line growth is exquisitely high demand in collections recovery, versus pricing. In Q4, plasma volumes expanded 43% YoY, driving plasma revenues up 43% in FY’23 illustrating this point. This is a testament to investments made in collections technology. Further growth in collections demand can be expected thanks to:

- Plasma fractionators were shrunk to record lows thanks to the Coronavirus, supply chain, etc.

- They are now replenishing inventories at accelerated pace now the bulk of issues have been resolved.

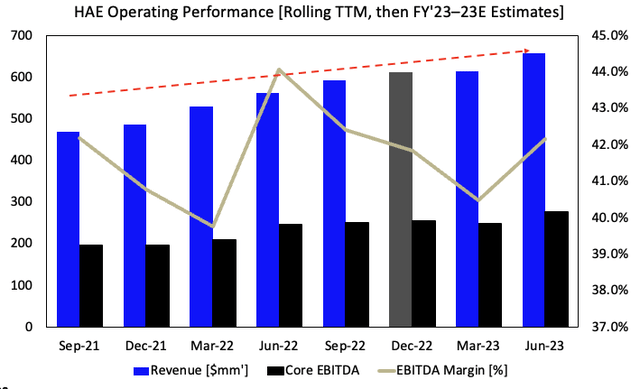

This should keep the cadence of collection volumes high over the coming years, in my opinion. If so, there’s scope to expect revenue and core EBITDA trends to ramp in-line with historical range [Figure 2].

Fig. 2

Data: Author, HAE 10-K’s

2. The firm retained the majority of its disposables business with CSL. This is another key point on the plasma front. CSL revenues contributed 14% to turnover in FY’23 and the Australian biotech giant remains a key customer for HAE into perpetuity. Importantly, regarding the CSL relationship going forward:

- Management expects the share of CSL’s plasma business to contract slightly in H2 FY’24.

- Nevertheless, this is still a minimum purchase commitment of $100mm onto HAE’s books, an amount that will eventually pull through to cash flow once collected.

As such, the CSL contributions remain a meaningful contributor to HAE’s top-line growth going forward. The pair’s lengthy relationship shouldn’t be discounted, especially given CSL’s market standing as a global leader across several markets.

3. Hospital revenue grew 18% YoY in FY’23 and was in line with guidance of 19%. Growth was underscored by upsides in vascular closure and haemostasis management. Q4 hospital turnover was $100mm and would represent $400-$450mm annualized if these trends continue. In my opinion, the firm’s hospital segment could be a meaningful tailwind going forward. It includes haeomstasis management, vascular closure, transfusion management and cell salvage. It is wise to be bullish for several reasons:

- One, the macro-level headwinds plaguing hospital margins have just about settled as of 2023. Labour markets, capital budgeting and patient turnover have all been major tension points for hospitals these past 2-3 years. Labour in particular was the focus in 2022 and looks to have resolved given HAE’s language on the Q4 call. This, coupled with normalized patient trends (revenue per day, patient days, revenue per capita, etc.) are driving hospital income back to pre-pandemic range.

- Two, management project 16-18% YoY growth in hospital revenue by FY’24, a mammoth effort that would reflect positively on the bottom-line. Hospital has a higher gross margin in the portfolio, so this is welcomed. Given HAE management’s insights, I believe we should expect a big 1-2 years for the hospital segment, even if actual results are a couple points off to the downside.

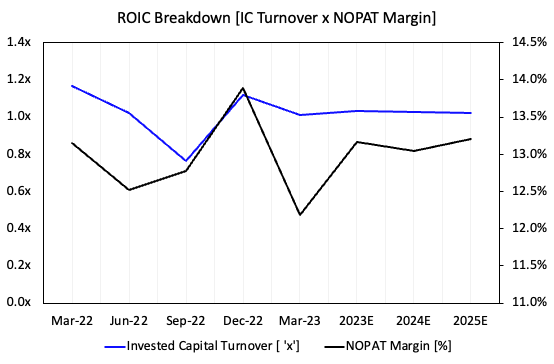

4. A bulk of HAE’s future intrinsic valuation hinges on capital productivity going forward. There are numerous reasons for this, namely, the nature of its products/services, and the drivers of its forward earnings growth. If anything, HAE will compound post-tax earnings over time as it ramps up capital investments into future growth initiatives. The profits (“ROIC”) it generates from these incremental capital charges are a function of the post-tax margin (“NOPAT margin”), and capital intensity (invested capital turnover). Figure 3 illustrates HAE’s ROIC drivers. Your chart starts at the far left and tracks rolling TTM performance from 2022-2023, with forward estimates. Invested capital turnover is calculated as the TTM revenue divided by capital at risk (invested capital). NOPAT margin is derived by the TTM NOPAT over TTM revenue. Key points to note:

- The firm routinely prints 13-15% trailing return on capital, a few points above the hurdle rate.

- This strength is majorly driven by capital productivity versus efficiency, as noted in the c.1.1x invested capital turnover vs. 12-13% NOPAT margin.

- These findings illustrate HAE’s strength on the production side, perfect seeing it is a B2B enterprise, and doesn’t rely on the consumer side.

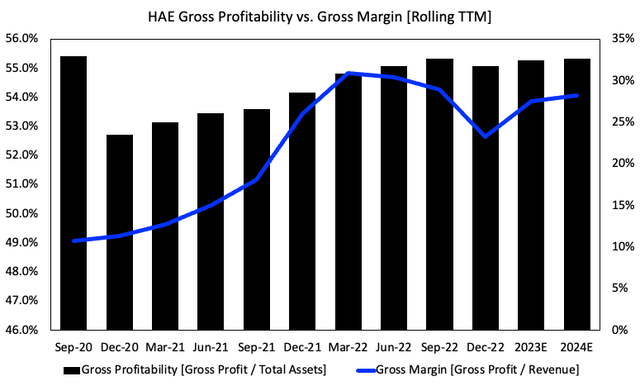

Meanwhile, gross profitability as a function of total assets is seen in Figure 5. Here, TTM gross profit is the numerator with the asset base comprising the denominator. You can see the lift in gross profitability over time, along with the shift from $0.24 to $0.32 in gross profit per $1 in assets. As a result, further investments into the capital producing HAE’s profits is likely to yield incremental growth in earnings in my opinion. This is critical in sealing the positive feedback loop going forward.

Fig. 3

Data: Author, HAE 10-K’s

Fig. 4

Note: Gross Profitability is a function of total assets, versus gross profit margin with revenue. (Data: Author, HAE 10-K’s)

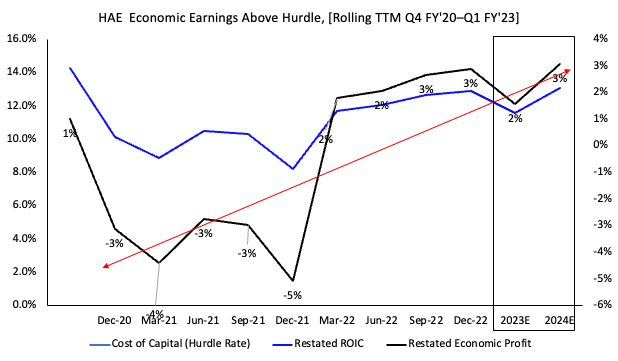

5. Related to the above, if capital productivity is so important to valuation upside going forward, it is essential to provide a demonstrated measure of success on HAE’s capital allocation decisions. Earnings growth does little to address this. instead, we need two primary measures:

- Economic earnings, the profit or loss above/below a hurdle rate produced by a firm’s new and existing operating assets.

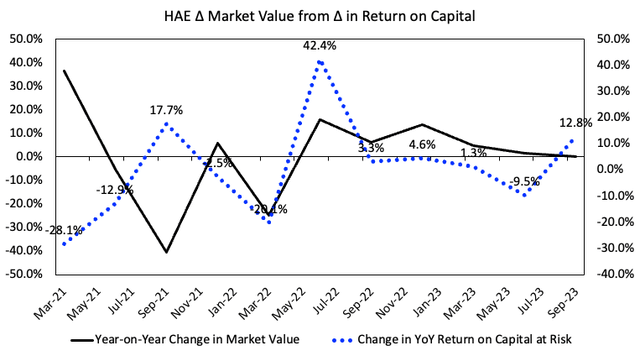

- The change in market valuation with respect to the change in HAE’s incremental investments. A high change in market value for each $1 HAE puts to work, would suggest high returns on capital, and a high reward from the market over time.

The latter will typically occur if HAE can demonstrate capital is more valuable in its hands than in the hands of an investor. Here, we’d look at its returns on capital. Presuming a 10-12% long-term hurdle rate, should HAE generate >12% economic profits on capital it puts at risk into productive assets, it will attract investment in my opinion. Investors will pay higher multiples if it compounds each $1 at superior rates.

Looking at Figure 5 and Figure 6, the potential for valuation upside this year is on show. First, the turnaround in economic earnings is observed in Figure 6 from December 2021, corresponding with the growth in market valuation. Further, the relationship between the change in HAE’s quarterly market cap is plotted against the change in ROIC, using TTM figures. There is causality in this pairing, as noted. The firm’s return on invested capital is a substantial driver of market value based on these findings.

Fig. 5

Data: Author,, Market Data, HAE 10-K’s

Fig. 6

Data: Author, HAE 10-K’s

Valuation and conclusion

Despite the substantial premium rating to peers across key multiples, the company still only trades at a c.$4.5Bn market valuation at the time of writing.

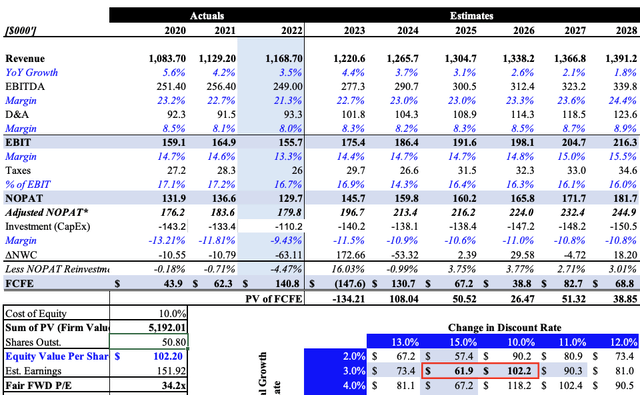

The question is, what are we privileged to in buying HAE at 29x forward earnings today. My numbers have HAE to print $1.2-$1.3Bn in top-line revenues this year and potentially through off $100-$130mm in cash to shareholders. I’d see this after at $135-$140mm CapEx and further $170mm in NWC requirements over the next 12 months. Discounting these projected cash flows at a 10% hurdle gets me to a market valuation of $5.2Bn or $102 per share, 34x my FY’23 earnings estimates.

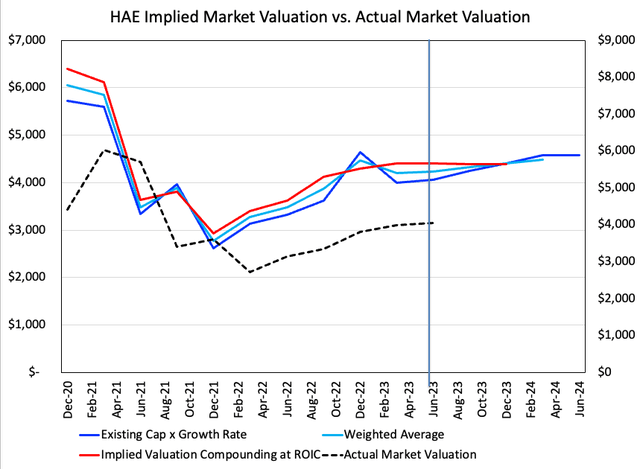

Further, the market implied valuation model shown in Figure 7 supports a repricing to the $5.5-$6Bn range by FY’24. Here, the firm’s market capitalization is projected across 3 measures that measure returns on capital and earnings reinvestment. Findings are then rolled forward 1-year to project the current period’s ROIC/growth onto the next. I get to the $5-$6Bn range with 12-13% forward returns on capital each quarter into FY’24. Hence, there is some confidence around the $5.5Bn/$83 per share mark from my estimates.

Fig. 7

Data: Author

Fig. 8

Data: Author

In summary, HAE is generating future shareholder value by recycling capital into the business, then growing profits at above-market rates. Key points driving the buy thesis include:

- Supportive valuations up to $5.5Bn-$6Bn of $102 per share, built with projected economic earnings growth into FY’25.

- HAE investing wisely into high-margin hospital segment and looks to emphasize this further looking ahead.

- Strengths in HAE’s capital productivity flat capital intensity on revenue, earnings growth.

- The market continues rewarding HAE with higher valuations each time it generates economic earnings above the hurdle rate.

Looking forward, I believe HAE will continue generating above-market profits on the capital invests to future growth. In that vein, I am happy to park capital to investing in the company. It has proven to produce favourable economic business characteristics and this warrants a buy rating. Net-net, rate buy at $102 per share target.

Read the full article here