Investment thesis

Our current investment thesis is:

- URBN is a quality business with several strong brands, which have all grown well and allowed the business to offset any individual weaknesses.

- In order to remain competitive, the company has compromised margins, which now leaves the business with unattractive returns.

- Despite the margin slippage, URBN is still valued in line with its historical average, leaving little upside.

Company description

Urban Outfitters, Inc. (NASDAQ:URBN) is a company that retails and wholesales general consumer products. Its three segments include Retail, Wholesale, and Nuuly.

The company’s Urban Outfitters stores sell apparel, footwear, home goods, electronics, and beauty products for young adults aged 18 to 28, while Anthropologie stores offer women’s apparel, accessories, home furnishings, and beauty and wellness products for women aged 28 to 45.

It also operates Terrain stores that provide lifestyle home products, as well as Free People retail stores that sell casual women’s apparel. The company also has a women’s apparel subscription rental service called Nuuly.

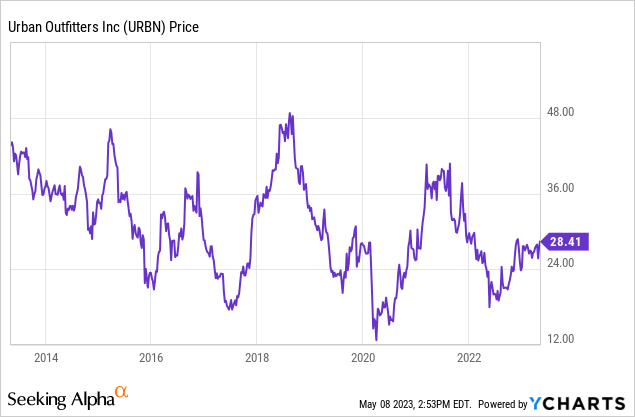

Share price

URBN’s share price has trended down in the last decade, experiencing periods of strong breakouts and declines as the company’s financial performance leaves investor sentiment swinging.

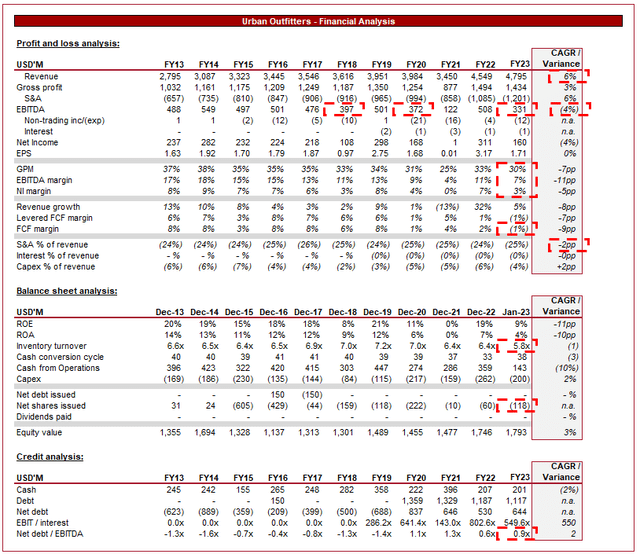

Financial analysis

URBN Financial performance (Tikr Terminal)

Presented above is URBN’s financial performance for the last decade.

Revenue

URBN has grown its revenue at a CAGR of 6%, which is quite strong relative to other brick-and-mortar (BAM) retailers we have considered in the past (See our analysis on V.F. Corp. (VFC), American Eagle (AEO), Dillard’s (DDS), Fossil (FOSL), Canada Goose (GOOS), Guess (GES), and Nordstrom (JWN). The industry has shifted away from BAM retailers as e-commerce brands can offer a wide variety of products at lower costs, lacking the cost of a physical footprint. Further, this has increased the number of choices and improved convenience, forcing these retailers to adjust their value proposition as a means of maintaining growth.

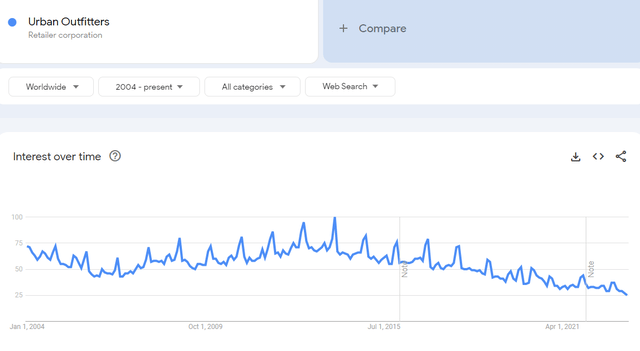

This e-commerce trend is driven by the widespread use of the Internet and social media. This has fundamentally changed the industry and should be considered a “shift” rather than a “trend”. UBRN has invested heavily in e-commerce, with a particular focus on social media.

URBN (Google Trends)

Despite the focus, the company has seen a declining trend in interest, which is a primary reason why growth has slowed as the decade has developed. This said, the company has over 9m Instagram followers and regularly interacts with customers as a means of driving impressions and creating trends. This has allowed the business to remain relevant, even if its relevancy is softening. This point should not be neglected as consumers are driving trends to a greater degree than brands, especially in the affordable segment.

URBN has sought to increase the value of its proposition relative to e-commerce by developing an omnichannel approach. Omni-channel retailing involves integrating various channels such as physical stores and online marketplaces to offer a seamless shopping experience. Consumers can easily purchase a product online and pick it up in person, or equally the opposite, and see a product in person before purchasing it online. This reduces the time-consuming act of waiting for delivery and potentially returning a product due to issues. This allows URBN to fight back against the convenience argument for e-commerce.

Finally, we think URBN’s diversified product offering across its brands has supported growth. The URBN group owns several high-quality brands, including Free People and Anthropologie, alongside Urban Outfitters. Each brand targets different segments, as well as some offering non-apparel, such as furniture. This allows the business to utilize shared operational competencies and infrastructure while increasing its TAM.

Despite what we think is a strong top-line performance, URBN faces several key challenges. The primary one is a highly competitive retail landscape. Moving e-commerce to the side (although remains relevant to this point), we have seen the rise of fast fashion. Companies can develop and produce designs incredibly quickly, allowing them to respond to changing trends to keep their products relevant and culturally superior. This places significant pressure on URBN to continually innovate its product range and increases the risk of the business losing relevance if it cannot do so successfully. So far, the business has been highly successful in this regard and is reflected in growth.

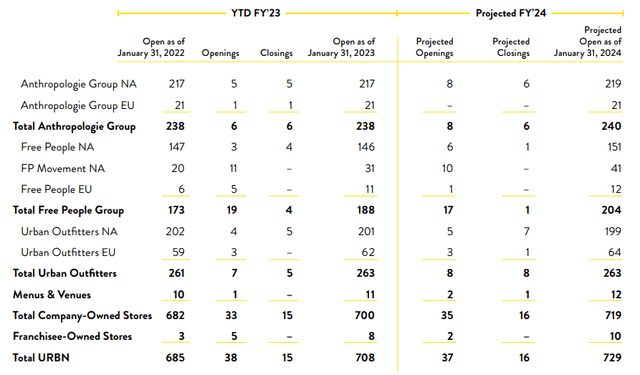

Further, as a BAM retailer, a key driver of revenue is also store openings. The company will continue to transition toward e-commerce, but supplementing this with store openings also is a reflection of a very healthy business. What we see is that URBN is growing on a total basis, with much of this coming from the Free People Group. Management’s intention is to focus on e-commerce, which we believe to be the key for growth.

Store openings (Urban Outfitters)

Economic considerations

Current economic conditions present a key short-term risk to URBN. Inflationary pressures and elevated rates are causing consumers to experience a squeeze on their finances, with many seeing their discretionary income decline. As a result, we are seeing a softening of demand across many industries, as consumers turn defensive. Retail is a sector that is generally hit hard, and our analysis of other retailers (see papers referenced above) has found that growth is rapidly grinding to a halt, if not already declining.

Margin

URBN’s margins have rapidly declined in the last decade, with EBITDA-M falling from 17% to 7%. The primary contributor to this is GPM, as S&A expenses have grown in line with revenue, remaining flat as a % of revenue.

This is likely an answer to how URBN has been able to support strong revenue growth, as its prices have declined in order to keep the company competitive. When factoring in the benefits of scale economies that were offsetting this, it is a remarkable strategic choice.

Further, the business is likely facing inflationary pressures, especially in the last few quarters, however, this is not the reason for the prolonged decline.

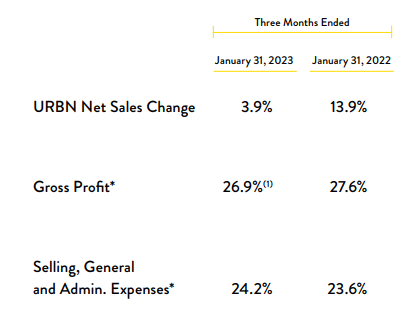

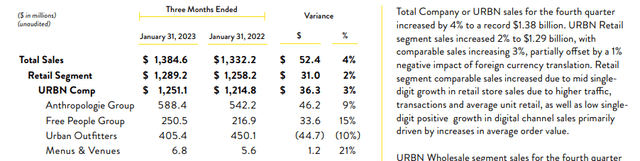

Q4 results

Q4 (URBN)

Presented above is URBN’s most recent quarterly results.

Revenue growth remains strong in our view, with many retailers we have looked at (see papers referenced above) experiencing a decline or flat growth. This is a reflection of a fundamentally strong cohort of brands.

This said, we continue to see margins slide, and in this case, S&A expenses have also increased. This leaves the business susceptible to becoming marginally profitable, as its FY23 NIM is only 3%. At these levels, investors are left with a sliver of returns.

Q4 results (URBN)

Looking specifically at URBN’s portfolio, the growth is shared among its brands, with weakness only in URBN. This reiterates our view that URBN has a fundamental superiority over other brand retailers who are reliant on growing a single brand Y/Y.

Balance sheet

URBN’s balance sheet is in a relatively strong position.

The company has a ND/EBITDA ratio of 0.9x, which is a comfortable level and gives the business the flexibility to raise debt if required for strategic initiatives.

Further, its inventory turnover is very high at 5.8x, maximizing its cash investment. We have seen a dip in the most recent year which suggests growth is slowing to a degree not expected by Management.

As mentioned previously, due to poor profitability, which translates into FCF, the company can only offer small distributions. Management’s choice has been buybacks.

Valuation

Valuation (TIkr Terminal)

URBN is currently trading at 10x LTM EBITDA, 8x NTM EBITDA and, 11x NTM earnings.

Our view is that the company’s commercial profile remains strong, with no material deviation from the company’s position in the last decade. This is likely the reason the company is trading in line with its historical average multiples.

The problem we see is that URBN’s margins are continuing to slip, which could contribute to a further decline in NIM if the company is unable to recover. We currently see little scope for improving this, with Management committed to maintaining growth.

Final thoughts

URBN is an outlier when we compare it to other brand-led BAM retailers. The company has strong growth and remains relevant, weathering (to an extent) the pressures faced by new entrants. In order to combat this shift, however, margins have been compromised, leaving little for investors.

Given the company is trading in line with its historical average, we struggle to see upside given the situation around margins.

Read the full article here