Company description:

Whirlpool Corporation (NYSE:WHR) is a multinational company that produces and sells home appliances and related products and services worldwide. The company’s product range includes refrigerators, freezers, ice makers, water filters, laundry appliances, cooking appliances, small domestic appliances, and dishwasher appliances, among others.

Whirlpool markets its products under a variety of brands, including Whirlpool, Maytag, KitchenAid, Hotpoint, and Indesit. The company sells its products through a variety of channels, from retailers to DTC.

Investment thesis:

Theoretically, WHR should be a fantastic defensive stock pick. The global population is growing, which is contributing to greater demand for housing. This should mean sustainable growth in the sale of home appliances. WHR is a leading business in this space and so is positioned perfectly to benefit from this. Unfortunately, the theory does not always play out and we have not seen this occur. The company has had a tough decade with little improvement. Our objective is to assess if the company is on the right track to kickstart healthy growth, as a means of being this theoretical defensive stock for investors.

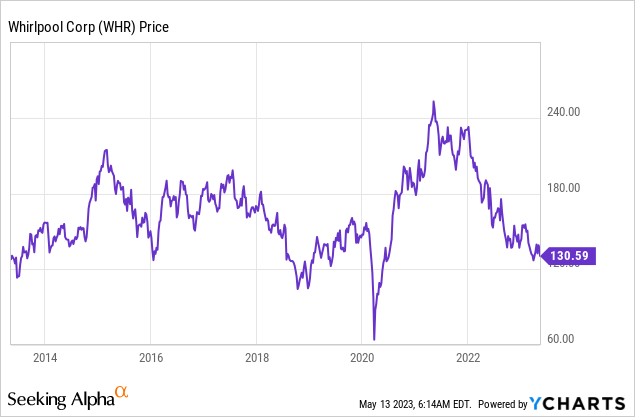

Share price:

As we have mentioned, the company has had a tough decade. The share price is c.10% from its price level 10 years. This stagnation has been driven by poor financial performance and a lack of growth. WHR has struggled with improving volume sales and underperforming segments.

Economic conditions:

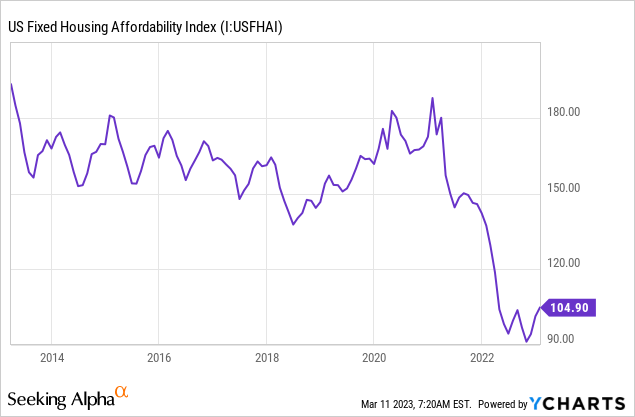

We are currently experiencing heightened inflationary pressures as a result of supply chain issues and an initial demand spike following the ending of Western lockdowns. This has contributed to a decline in consumers’ finances as their cost of living increases at a greater rate than wages. Naturally, consumers have been cutting back on expenditures that can be foregone, as they look to shore up finances. As the following graph illustrates, consumers find themselves at a decade low for home affordability.

The impact on home appliances is an interesting one. Consumers clearly cannot go without a fridge or freezer, but can certainly avoid discretionary purchases or other less important appliances, such as water filters. On a net basis, our view would be that demand for home appliances will decline. WHR experienced a 10.3% decline in net sales during FY23, largely driven by this factor. This is the largest decline the company has experienced in 10 years.

Looking ahead, our view is that conditions will continue to deteriorate as inflation is not falling substantially M/M. Not only this but the risk of a recession in 2023 remains heightened, which will only compound the impact on WHR further. Management is guiding a 1-2% decline in sales, which looks optimistic when compared to FY22.

Home data:

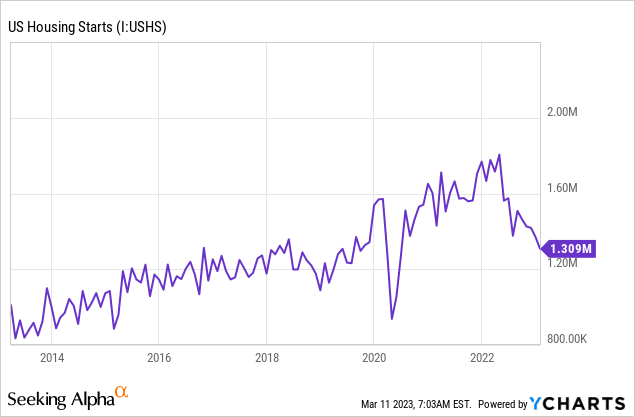

A significant amount of demand for appliances is derived from new home purchases, as consumers generally furnish new homes with purchased appliances. This is because in many cases, it can be difficult or unattractive to move key appliances when moving home, with the preference being to replace the items. As a result of this, new home builds, home prices, and home purchases are great forward indicators for appliance demand.

Home builds

As the above graph illustrates, the number of housing starts has declined to levels not seen since before the pandemic. This suggests home builders do not see the profitability required to undertake builds, implying home prices are unattractive. As a result of this, fewer appliances will be in demand once these properties are completed. The degree of impact depends on how long housing starts remain at lower levels. The impact of prior declines in housing starts can be seen below.

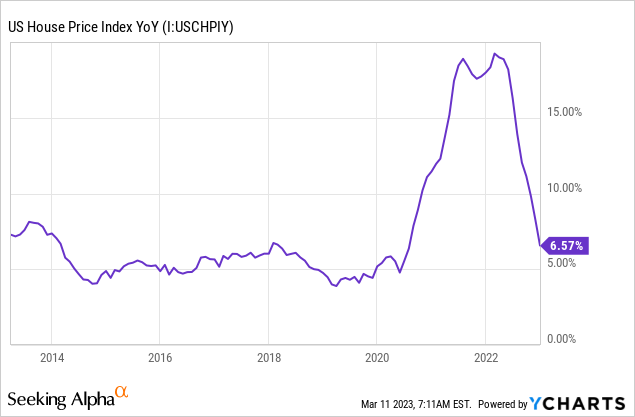

Home prices

As the above chart illustrates, US house prices have seen a sharp correction following the post-pandemic boom. The impact of this is a reduction in equity for many consumers who have seen their house prices decline. Due to this, consumers are far less likely to invest in improvements, as they have a smaller “buffer” to their realizable value.

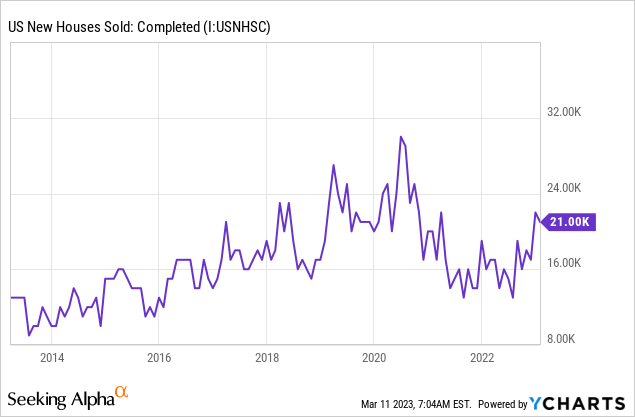

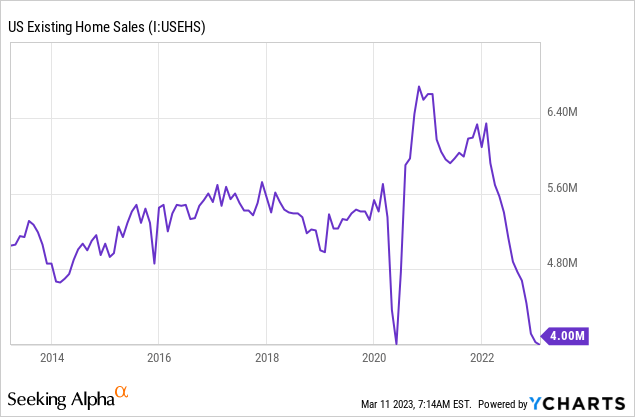

Home sales

As illustrated above, the culmination of the many factors we have described has contributed to a noticeable deterioration in the number of homes sold. With fewer consumers moving, there is a reduction in the need to purchase new appliances. This is a less forward-looking indicator but helps to explain why demand has declined.

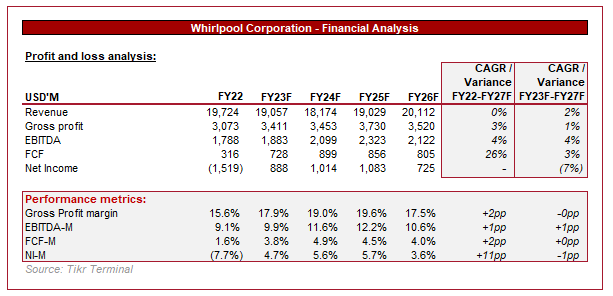

Financial performance

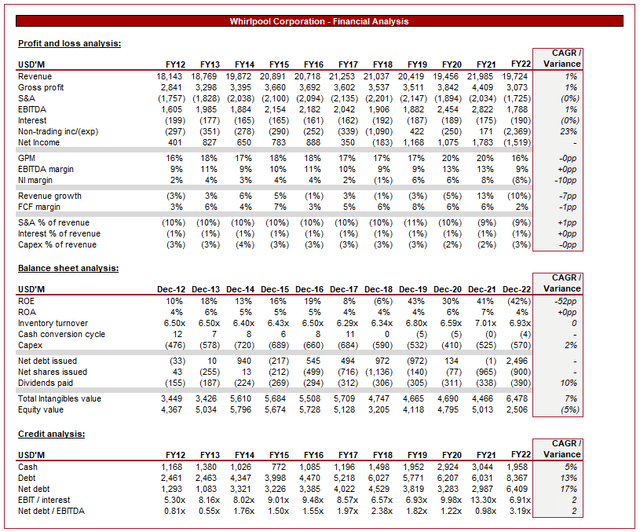

Whirlpool Financials (Tikr Terminal)

Presented above is Whirlpool’s financial performance for the last decade, which can be summarized as highly disappointing.

Revenue has grown at a CAGR of 1%, which somewhat hides the revenue struggles the company has had. Growth in many periods has been strong but WHR has been unable to sustainably grow the business. FY21 likely contained deferred demand from FY20, which is why the decline in FY22 was overly pronounced. One of the reasons WHR has struggled is the level of competition from other brands. The industry contains many low-cost Asian producers, as well as leading brands such as LG and Samsung. Although WHR has many highly regarded brands, they cannot stand up to the pricing power of the lower-cost producers or the quality of LG/Samsung.

Gross profits had been on an upward trend until FY22 when the company experienced a 4% decline. This has been driven by inflationary pressures and supply chain issues, with greater energy and logistics costs. Our wider market research suggests these are beginning to ease, with the potential for GPM to tick up in the coming 24 months.

The development of S&A is interesting. The company has maintained seemingly good cost controls, with S&A expenses gradually declining. Management attributes this to effective cost management but we are less sold. Marketing and operational expenditure have been ineffective in growing revenue and we do not see investment to correct this. Management looks to be cutting costs where possible to maintain short-term margins.

The net profitability profile from these factors is an EBITDA margin in the region of 9-11%, with an FCF conversion of 2-6%. These metrics can be attractive if there is healthy growth, which we cannot see.

Moving onto the balance sheet, the company’s inventory controls have been good, with WHR not seeing a material change in turnover despite the slowing demand. This has allowed WHR to improve short-term liquidity as evidenced by its CCC.

Further, the company’s solvency position is quite unattractive. In the most recent year, the company has raised a substantial amount of debt to shore up its balance sheet as it financed its acquisition of InSinkErator for $3BN. This has led to ND/EBITDA ratio ballooning to 3.2x, far above its prior levels. Further, interest coverage has already fallen to 7x, before the impact of the most recent raise. Management could have chosen to reduce buybacks and dividends, which it will likely need to in the coming year, but did not and we think this is a mistake. Fitch concurs with this view, downgrading the company to a negative outlook.

Regarding the acquisition, InSinkErator has over 70% market share in the food waste disposal industry, giving the business a dominant position in the market. The company does have opportunities to grow, with its developing world market share far below its share in the West. WHR estimates that the company will add $1.25 EPS from FY23 onward. There is definitely scope for accretion here but the valuation looks high. InSink generated $595M in revenue at Mar-22 year-end, which implies a valuation of c.5x revenue.

Q1 results:

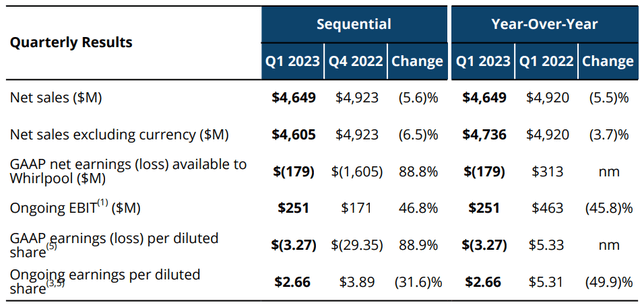

Q1 results (WHR)

WHR recently posted its Q1 results, with sales continuing to slide M/M and Y/Y. This is a reflection of what continues to be difficult trading conditions, with the company swinging to a GAAP loss. Management are continuing to pivot toward better margin products, and has seen some benefit in their North American operations, but any material value has yet to be realized.

Outlook:

Analyst outlook (Tikr Terminal)

Presented above are analysts’ forecast numbers for the coming 5 years.

Revenue is expected to grow at a CAGR of 0%, with a decline in both FY23 and FY24. Although we do not have a strong opinion on FY24, FY23 looks far more reasonable than Management’s forecast decline of 1-2%.

FCF and EBITDA are expected to normalize slightly higher into the range we expected.

Valuation:

Valuation (Whirlpool)

WHR is currently trading at 9x EV/EBITDA, which looks quite attractive relative to its current profitability. Investors are pricing in deteriorating performance in the coming two years, which we see as highly likely. Dividends and BBs are unlikely to be sustainable, which will only compound the impact of this.

Final thoughts:

WHR is facing an extended period of softening demand as macroeconomic factors compound a decline in sales over the coming 12-24 months. Consumers are struggling with everyday expenses, let alone in a position to be purchasing home appliances. If required, they can BE purchased second-hand or from cheaper producers. Home data suggests this soft demand could go beyond the inflationary period, which possibly could come to an end in the next 12 months. Beyond these headwinds, however, you find yourself with a fundamentally underwhelming business, which leads us to the question of, what is the point?

With headwinds ahead, we rate WHR stock a sell.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here