WPP (NYSE:WPP) is global communication, advertising, and public relations company based in London, England. Though the company engages with digital services, it primarily serves large-account consumers through mass media campaigns such as Nike’s ‘Never Done Evolving’ or Ford’s ‘Very Gay Raptor’ campaigns.

These activities have enabled $17.77bn in TTM revenues, alongside a same-period EBITDA of $2.68bn.

Introduction

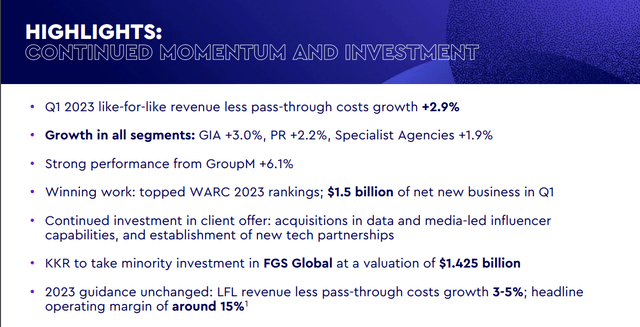

The financial and operational highlights of WPP through Q1 2023 centre around the company’s ability to reduce costs while scaling, the firm’s continuous growth in the face of macro headwinds, higher quality work, KKR’s minority investment into subsidiary company FGS Global, and overall improvements to operational margins.

WPP Q1’23 Investor Presentation

The general theme of the previous quarter has thus been one of resurgent demand, adaptation to rising capital costs, and noteworthy component value of WPP’s subsidiaries across all verticals.

Valuation & Financials

General Overview

In the TTM period, WPP, down 4.72%, has experienced poorer price action to both the general market, represented by the S&P 500 (SPY)- up 4.91%- and the SPDR Communications Index (XLC), up 3.56%.

WPP (Dark Blue) vs Market & Industry (TradingView)

Likely a product of reduced demand for advertising and communications services, WPP, as a pure-play, has experienced the brunt of macro headwinds and reductions in client cash flows.

On the flip side, the likes of Alphabet (GOOG) (GOOGL) and Meta Platforms (META) are the largest components of the XLC index, with the two leading the index’s growth.

Comparable Companies

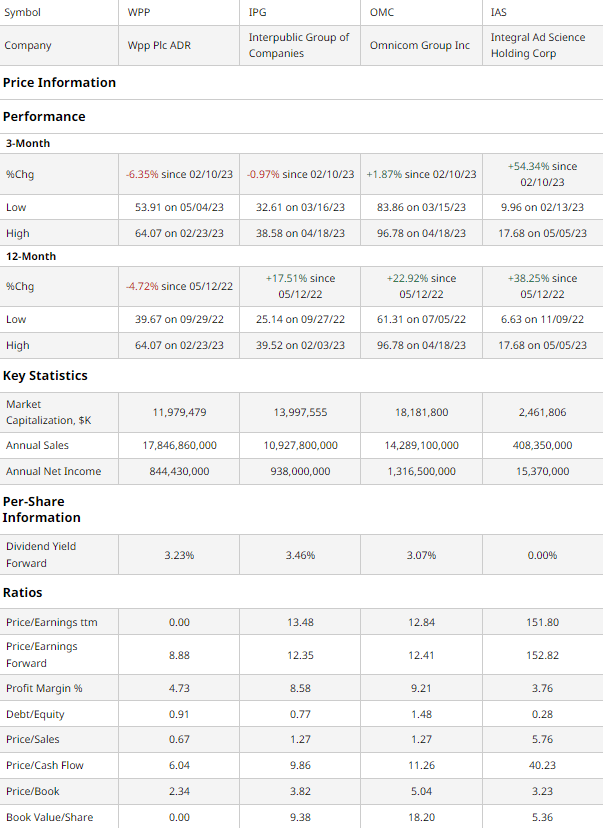

While the advertising industry is now dominated by tech industry leaders, mid-cap companies, with focuses on advertising campaigns and large accounts akin to WPP include the Interpublic Group of Companies (IPG), Omnicom Group (OMC), and Integral Ad Science (IAS).

barchart.com

As demonstrated above, WPP has experienced the poorest price action both over the past quarter and year. This comes in spite of strong multiples-based valuation metrics across the board.

For instance, WPP sustains the lowest forward P/E ratio at 8.88, contrary to the median figure of 13.16. Additionally, assessing P/CF and P/B, WPP sustains superior value to all peers.

Justifying this undervaluation, however, may be the company’s second-lowest profitability and a higher-than-median Debt/Equity ratio. That said, I do not believe these factors necessitate lower forward valuations, as WPP is experiencing a reversion to higher margins and its capital deployment does put a premium on debt reduction. Moreover, with higher valuations of its subsidiary companies, debt becomes a lesser concern.

Valuation

According to my discounted cash flow analysis, at its base case, WPP is undervalued by 48%, with a fair value of $107.25, up from its current price of $55.89.

My DCF model assumes a benchmark 10% discount rate, both in line with the interest-induced increased cost of capital and WPP’s relatively higher debt/equity ratio versus peers. I estimate net margin growth similar to pre-2022 levels as we are already seeing a reversion alongside revenue growth of 4-5%, but still lower than the 14.1% projected advertising industry CAGR due to potential recessionary impact.

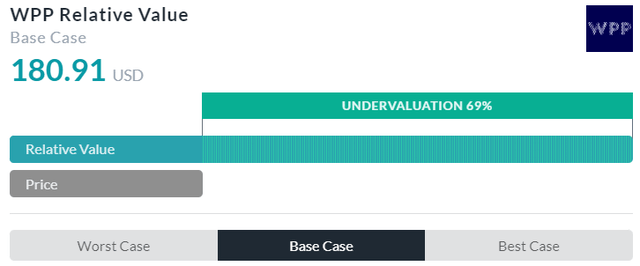

AlphaSpread

AlphaSpread’s multiples-based relative valuation tool more than verifies my thesis on the undervaluation of WPP, calculating, at its base case, an undervaluation of 69%, with a fair price of $180.91.

In my opinion, AlphaSpread actually overvalues the firm, since it does not assess the value given a relatively higher debt/equity ratio, for example.

Therefore, using a weighted average skewed toward my DCF, the fair value of WPP is ~$111.78, with the stock currently undervalued by 50%.

Synergistic M&A Supports Whole Business Integration

The organizational structure of WPP can be segmented into three primary focuses; Global Integrated Agencies – the largest segment, Public Relations, and Specialist Agencies. These segments can then be further divided into WPP subsidiary entities, such as Ogilvy and FGS Global. Such subsidiaries enable a greater degree of specialization for clients, the development of a more nimble organization, and the ability to independently manage and evaluate the financial strength of each business. For instance, FGS Global recently received a 29% minority investment from KKR, boosting the firm’s implied EV to $1.425bn.

WPP Q1’23 Investor Presentation

Identifying modular scale and value growth as a winning strategy while sustaining a forward-looking strategy, WPP has focused on inorganic growth via a series of acquisitions. Said acquisitions include the likes of Goat- a global influencer agency, 3K Communications- a healthcare specialist PR agency, and amp- a sonic branding agency. And to further accelerate technology deployment and access to its product mix, WPP has partnered with firms like KDDI, providing Web3 content capabilities and Stripe, for commerce and payments solutions.

WPP Q1’23 Investor Presentation

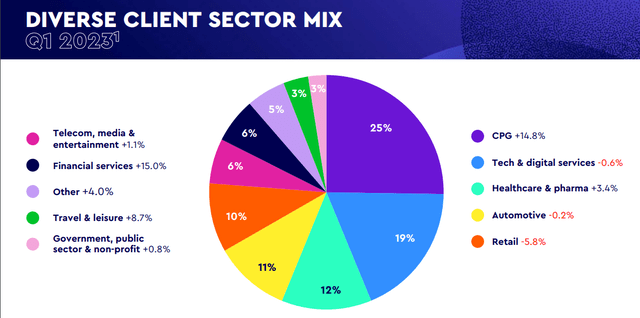

The confluence between these strategies has ultimately led to a level of revenue diversity and an ability to upsell products throughout the advertising life cycle. The company sees geographic diversification, end-industry diversification, and segment diversification as key to facing macro headwinds and competing in an increasingly digitally dominated market. For instance, while the US (37% revenues) and Europe (>20% revenues) dominate WPP revenues, China (5% revenues) and India (3%) have led growth, with 12% and 25% respective growth levels.

WPP Q1’23 Investor Presentation

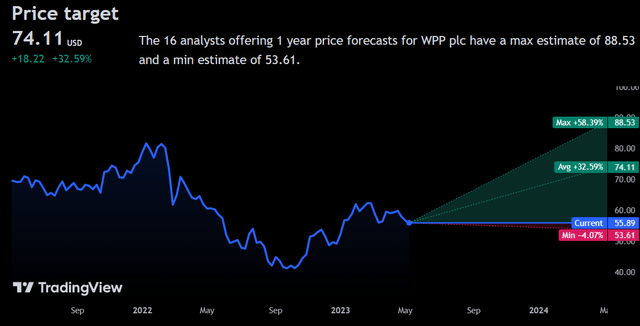

Wall Street Consensus

Analysts affirm my positive view of the company, projecting an average single-year price increase of 32.59% to a price of $74.11.

TradingView

Even at the minimum projected price of $53.61, down 4.07% from today, would mostly be recovered through dividend income and operates in a scenario of continuously compressed demand, an unlikely proposition considering the demand reversion- as evidenced by increased advertising revenues in the first quarter of this year.

Risks & Challenges

Continued Demand Compression Due to Recessionary Pressures

Although we have seen a return to regular demand levels, there is a risk, with the higher wage growth experienced over the past year, of continued inflationary pressure supporting interest rate hikes and leading to perpetual reductions in cash flows for WPP. This may also lead to a larger debt load being realized.

Client Loss to Tech Firms

The lower cost, greater flexibility, and specialization offered by Alphabet, Amazon (AMZN), and Meta have led to a need for reorganization among traditional advertisers such as WPP. While the firm has pivoted towards the organization of mass media campaigns which cannot be replicated by big tech, there is a risk of higher costs of these campaigns driving clients to spend less on such mass market media campaigns, especially with the prevalence of many adverts declining with the popularity of cable.

Concentrated Client Structure

As WPP and the like have pivoted toward larger accounts, they have increasingly become dependent on larger firms for demand and revenues. Though WPP seeks to mitigate this by geographic and end-market diversification, most of its clients remain larger corporations, thus meaning increased vulnerability to the whims of any such companies.

Conclusion

In the short term, I expect WPP to revert to fair value and continue to capture the demand reversion in the advertising arena.

In the long term, I project WPP’s disciplined M&A strategy will re-position the company for sustainable returns and a reduced large account concentration.

Read the full article here