Overview

Dollar General Corporation (DG) and Dollar Tree Inc. (NASDAQ:DLTR) are two leading operators of discount variety retail stores in North America.

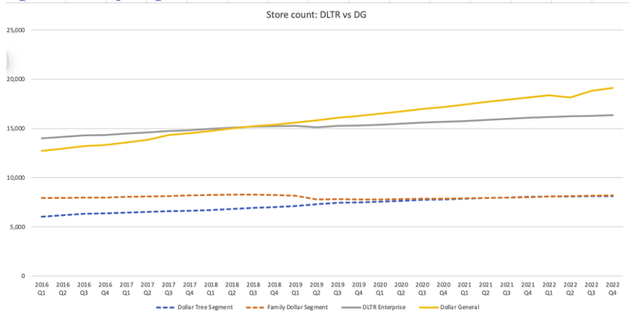

Dollar Tree Inc. operated over 16,340 stores in two segments, Dollar Tree and Family Dollar. The Dollar Tree segment (which I will refer to as the “Dollar Tree segment” to differentiate it from Dollar Tree Inc.) offers merchandise at a fixed price of $1.25 in both the US and Canada, while its Family Dollar segment, like Dollar General, offers a broader variety of general merchandise across a wider range of price points. Dollar General operated 19,104 stores as of Q4 2022.

Over the last 5 years, Dollar General has outperformed Dollar Tree on its stock return, operating, and financial metrics, but both companies trade at similar valuations.

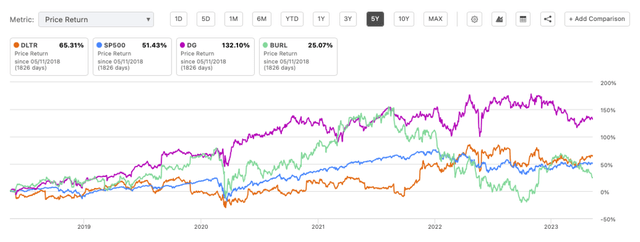

While both companies outperformed the S&P500 over since 2018, Dollar General has delivered twice the return (Figure 1, purple line) compared to Dollar Tree (orange line).

Figure 1: Stock price comparison

Seeking Alpha Charts

Operating performance at Dollar Tree has been lackluster at best, particularly at its Family Dollar segment, which has hobbled the company since it was acquired in 2015. In contrast, Dollar General executed well, going from strength to strength in same store sales, store openings, and operating margins, and delivered solid return on tangible capital

Store openings: Since 2016, Dollar General has expanded its store count by over 50% to nearly 20,000 stores (Figure 2,yellow solid line). Dollar Tree, which operated more stores in 2016, was only able to grow stores by 17% (grey solid line) as management was distracted by difficulties at the Family Dollar stores it acquired in 2015 and was forced to close under-performing Family Dollar stores or convert them into Dollar Tree bannered stores (dashed orange line).

Figure 2: Store openings

Created by author using public financial information

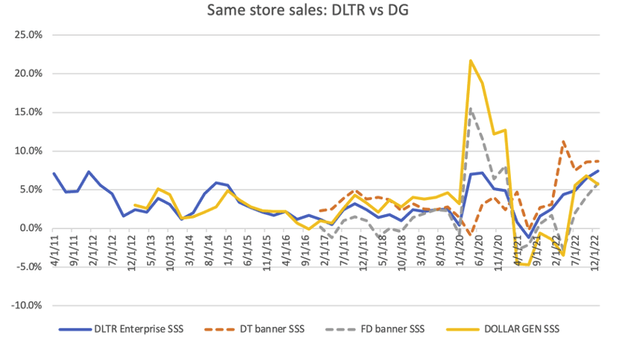

Same store sales growth: Since Dollar Tree acquired Family Dollar in 2015, its enterprise same-store sales growth (Figure 3, solid blue line) has languished in the low single digits and underperformed Dollar General (solid yellow line) as its Family Dollar segment underperformed the Dollar Tree segment (dashed gray vs dashed orange lines). Same-store sales numbers for both companies spiked during the COVID-19 pandemic when the stores were deemed essential but have regressed to their longer-term levels.

Figure 3: Same store sales growth

Created by author using public financial information

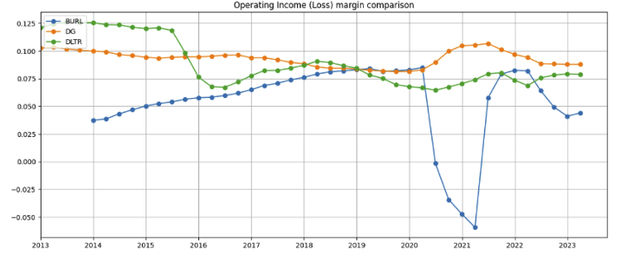

Operating margins: Dollar Tree’s enterprise operating income margins contracted in 2015 following the acquisition of Family Dollar (Figure 4, green line), while Dollar General’s operating margins have held up well (orange line).

Figure 4: Operating margins

Created by author using public financial information

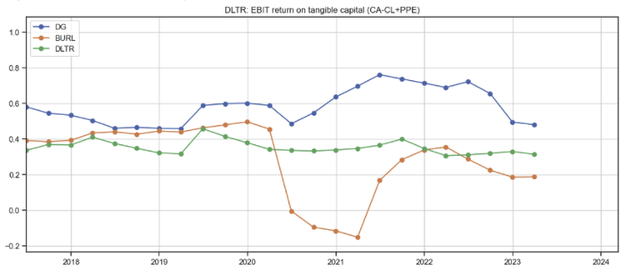

Return on tangible capital (defined as current assets + net plant, property, and equipment – current liabilities) of both companies have been strong, but Dollar General’s is higher than Dollar Tree’s by about 900 basis points (Figure 5, blue line vs green line).

Figure 5: Return on tangible capital

Created by author using public financial information

Dollar General’s stronger operating performance is clearly reflected in its per-share financials

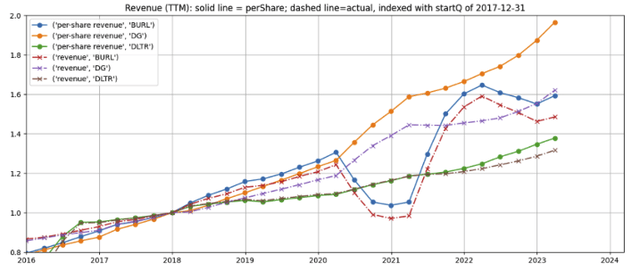

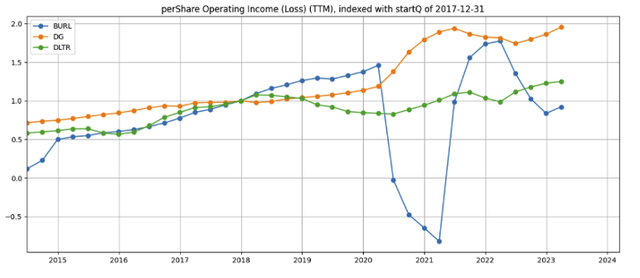

Dollar General’s per-share revenue and per-share operating income have almost doubled since 2018 (Figure 6 and Figure 7, orange line), while Dollar Tree’s per-share revenue has grown by just about 40%, with its per-share operating income growing even less (Figure 6 and Figure 7, green line)

Figure 6: Revenue and per-share revenue

Created by author using public financial information

Figure 7: Operating income (per-share)

Created by author using public financial information

Dollar Tree’s problems come mainly from its Family Dollar segment

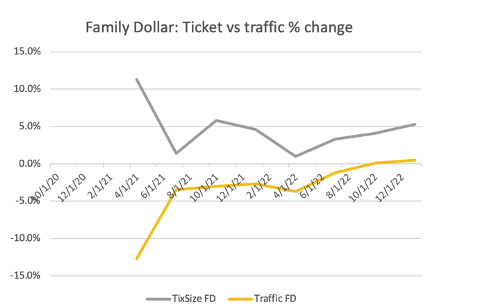

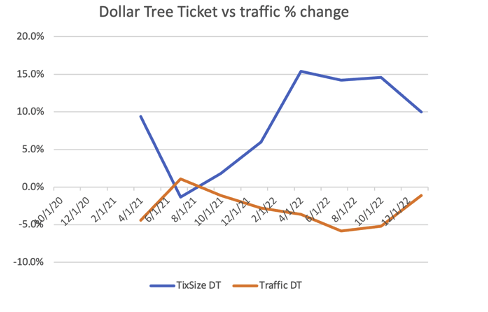

Apart from weaker store openings (Figure 2 above) and same-store sales growth (Figure 3 above), Family Dollar’s traffic and ticket sizes (Figure 8) have also significantly underperformed stores in the Dollar Tree segment (Figure 9).

Traffic at both segments remained weak even as the COVID-19 pandemic receded because consumers continued to make fewer store visits, but they purchased more items per visit.

In early 2022, Dollar Tree management decided to “break the buck”, raising its Dollar Tree segment’s price point to $1.25 as high inflation made it impossible to provide certain popular consumable items (particularly food) at the $1 price point. This boosted the average ticket size by 10-15% year-over-year, more than offsetting the traffic decline that may have resulted from the price increase.

As of Q4 2022, management reported that substantially all its stores have been converted to $1.25. As such, ticket sizes and traffic levels at the Dollar Tree segment are likely to revert to historical levels.

Figure 8: Family Dollar % change in ticket and traffic

Company Q4 2022 presentation

Figure 9: Dollar Tree segment % change in ticket and traffic

Company Q4 2022 presentation

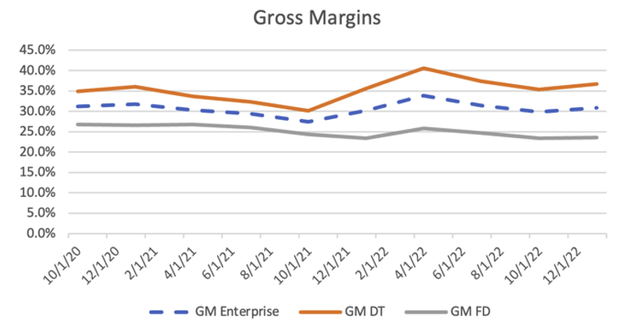

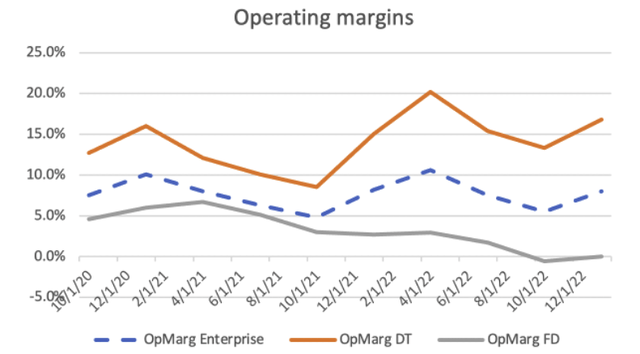

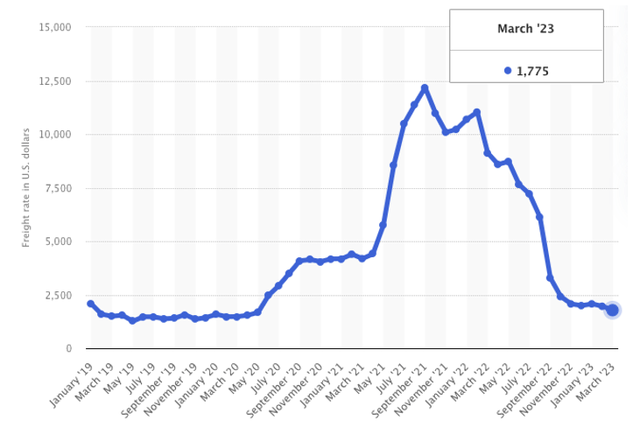

Family Dollar’s gross and operating margins (Figure 10 and Figure 11, grey lines) are substantially lower than the Dollar Tree segment’s (orange line) and have declined over the last 2 years while the Dollar Tree segment’s margins have expanded. As Dollar Tree imports more of its products than Family Dollar and should have been more heavily impacted more by high ocean container shipping costs (Figure 12), the negative trend raises further concerns about the extent of issues at Family Dollar.

Figure 10: Gross margins

Created by author using public financial information

Figure 11: Operating margins

Created by author using public financial information

Figure 12: Container freight rate: Shanghai to Los Angeles (Statista)

Statista

As ocean container shipping costs have pulled back to near pre-COVID levels, I expect gross margins at both segments to increase going forward, but the company will not see the full benefit of these lower rates until Q1 2024 when the higher cost, long-term contracts with its shippers expire.

Dollar Tree segment margins are decent (Figure 13) and likely to expand as the impact of declining ocean shipping rates works its way into the financials and inflation moderates.

Figure 13: Dollar Tree segment margins

Company Q4 2022 presentatation

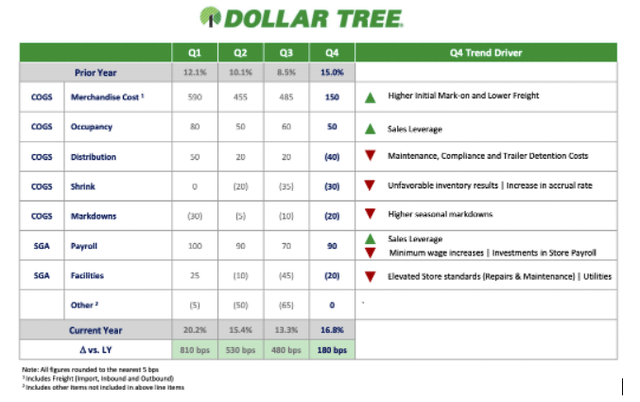

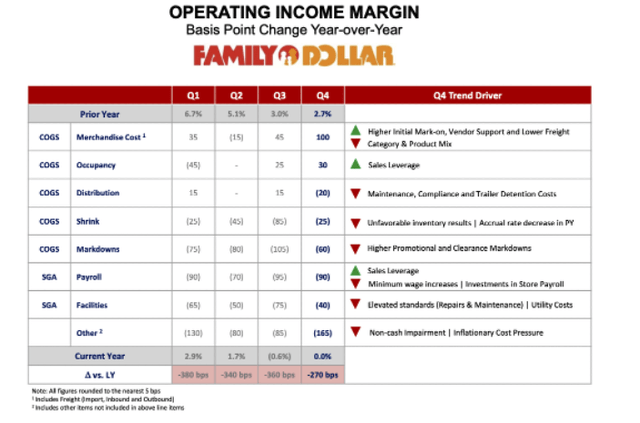

Family Dollar’s operating margins dropped to 0% in Q4 2023 (Figure 14). The margin compression includes the impact of “one-time” items such as the costs and write-downs related to rodent infestation of its West Memphis-Arkansas distribution center and inflation-related inventory markdowns. However, I am particularly concerned with the impact of the company’s “price-investment strategy” that was needed to bring Family Dollar’s prices down to be more in-line with its competitors, which indicates that Family Dollar’s will continue to struggle to remain profitable unless it improves its operational efficiency.

Figure 14: Family Dollar margins

Company Q4 2022 presentation

Valuations are similar even though Dollar General is clearly better run

Between the two, Dollar General is clearly the better run company. Even though the Dollar Tree segment appears to be doing well, Dollar Tree’s performance has been hampered by the sub-par performance of its Family Dollar segment, which previous management teams have failed to fix or realize integration synergies between the two segments.

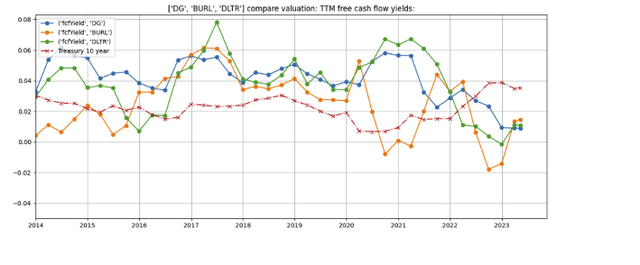

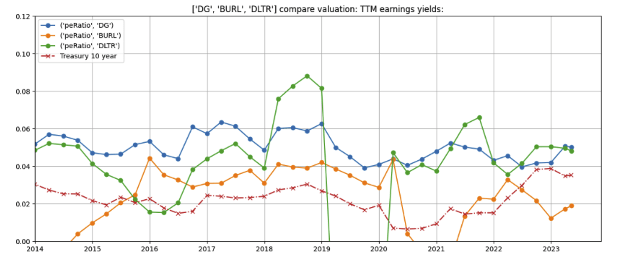

Interestingly, both trade at very similar valuations on both free cash flow yield and earnings yield metrics (Figure 15 and Figure 16, blue and green lines). Under most circumstances, a rational investor should choose to invest in Dollar General over Dollar Tree. However, the new management team and strategies implemented by Mantle Ridge LP, an activist hedge fund headed by Paul Hilal, changes the risk-return characteristics and increases the likelihood that the issues that plagued Dollar Tree will be resolved. (Mantle Ridge filed its beneficial interest through a Schedule 13D filing, signaling its intent to influence control over the company).

Figure 15: Free cash flow yield

Created by author using public financial and stock price information

Figure 16: Earnings yield

Created by author using public financial and stock price information

The entry of activist investor Mantle Ridge LP improves Dollar Tree’s risk-return characteristics

I would be inclined to exchange my position in Dollar Tree Inc with Dollar General shares if not for the fact that Dollar Tree is in an intensive turnaround orchestrated by Mantle Ridge, whose interest is well-aligned with public shareholders through its large shareholding, which has dedicated significant resources to the turnaround and has rebuilt the top team with experience and well-qualified executives, many of whom were previously key executives at Dollar General.

Mantle Ridge is well-aligned with public shareholders

Since March 31, 2022, Mantle Ridge has reported a beneficial interest of 11,365,531 shares in the company with a value of USD1.764 billion based on the May 11, 2023, stock price. The position represents more than 5% of the 224 million fully diluted shares outstanding and is one of only 2 positions Mantle Ridge holds. Dollar Tree constitutes 95% of Mantle Ridge’s net asset value, while its other position—a 2.7 million share position in Aramark valued at USD111M, makes up just 5% of total NAV.

It is illuminating when Mantle Ridge head Paul Hilal remarked in an April 2021 interview with the Harvard Crimson that to “help the system work more efficiency and productively through innovation, provide some service to people reliability is massively value creating and honorable”. This may shed some light on his underlying motivation in addition to making money.

Top team replaced with experienced and well-qualified executives

Chairman and CEO: Richard Dreiling, who served as Chairman and CEO of Dollar General from 2008 after it was taken private by Kohlberg Kravis & Roberts & Co. (KKR) till 2016, delivered a strong return for KKR and public investors.

Richard Dreiling was elected Chairman of Dollar Tree in March 2022, replacing former Chairman Bob Sasser, who was also previously CEO of Dollar Tree. Richard Dreiling took over the addition role of CEO from Mike Witynski in January 2023.

Over the last 15 months, Mantle Ridge has replaced 12 of the 14 officers listed on the leadership page of Dollar Tree’s website. The only two members who have not been replaced are Neil Curran, who heads Dollar Tree Canada, and Rick McNeely, the Chief Merchandising Officer for the Dollar Tree segment (though I note that Rick McNeely’s responsibilities for Family Dollar have been taken over by a new hire).

Under Mantle Ridge’s leadership, the company has hired several former senior members at Dollar General to head key areas that are in dire need of fixing.

Chief Supply Chain Officer: Mike Kindy, who joined Dollar Tree in May 2023, was previously Executive Vice President at Dollar General, accountable for supply chain strategy, including transportation, distribution, demand chain, allocations, procurement, and master data management. He is well-credentialed to revamp the Family Dollar segment’s under-developed supply chain—this is one of two areas—the other being Family Dollar Merchandising—that are in dire need of fixing.

As Richard Dreiling noted on the Q2 2022 earnings call:

In terms of the supply chain side, we’re looking at everything in the supply chain. We are assembling, I think Mike would agree, probably one of the best supply chain teams in the country. We have a lot of distribution centers that need to be updated and modernized.

I believe that a successful update and modernization of Dollar Tree’s enterprise supply chain is essential to drive efficiency and profitability for both the Family Dollar and Dollar Tree segments.

Mike Kindy appears to have replaced John Flanigan, who joined Dollar Tree as Chief Supply Chain Officer in May 2022 after retiring from a similar role at Dollar General in 2016, but I was not able to find any information on this change in appointment.

Chief Merchandising Officer, Family Dollar: Larry Gatta, previously served as Senior Vice President and General Merchandise for consumables at Dollar General. (As I noted above, the Chief Merchandising Officer for the Dollar Tree Segment, Rick McNeely, had previously served as Enterprise Chief Merchandising Officer responsible for both Dollar Tree and Family Dollar. Richard Dreiling noted:

Larry will be focused on improving Family Dollar’s operating performance and productivity through sales driving initiatives that provide great value for our shoppers. [He has been tasked to] improve store productivity, customer satisfaction, and to better support store associates through efficiencies. Changes include adding linear footage; developing seasonal assortments as a focal point; utilizing deeper shelving on key consumable categories to enhance store efficiencies and improve in-stocks; expanding the direct-to-store delivery offering; enhancing space dedicated to snacks and increasing the beverage offering; and optimizing the frozen food assortments.

Chief Information Officer: Bobby Aflatooni joined Dollar Tree from Howard Hughes, but he worked at Dollar General from 2011 through 2018. He too has his work cut out for him. According to Richard Dreiling:

The IT side — information technology, I might classify as a little bit bigger surprise, in that there are a lot of basic things that the operators and the merchants need and the supply chain needs.

We are simply not where we need to be from a systems perspective to reach our potential. We have recently begun a comprehensive review of all of our systems and infrastructure to make the right decisions and investments to take Dollar Tree and Family Dollar to the next level.

Other key senior positions were similarly replaced with well-qualified managers bringing very relevant experiences, including:

Chief Financial Officer: Jeff Davis, previously Treasurer for Walmart Stores, CFO for Walmart US, CFO at JC Penney, and CFO at Darden Restaurants,

Chief Operating Officer: Mike Creedon, previously COO at Advanced Auto Parts, and

Chief People Officer: Jenn Hulett, previously Chief Human Resources Officer of Core-Mark.

The company is still searching for a general counsel.

Every officer has their work cut out for them. In a high-stakes turnaround situation as this, time is of the essence and there is little room for error or underperformance, which may explain why former CEO Mike Witynski and for Chief Supply Chain Officer John Flanigan have been replaced.

Impact of macroeconomic and one-time factors on margins

Inflation and recessionary environments

Core customers of discount stores typically have lower incomes and are disproportionately impacted by inflation, as higher prices on non-discretionary items and consumables reduces the money they have for discretionary spending. In response, the company has focused on increasing the proportion of consumables at both Family Dollar (which represents 76.6% of sales, up 120 basis points from a year ago) and its Dollar Tree segment (42.5% of sales, flat from a year-ago). However, persistent inflation has caused some customers with higher income (>$80,000 p.a.) to turn to discount retailer with lower price points such as Dollar Tree’s, potentially offsetting core customers’ loss of buying power.

In a recessionary environment, customers are likely to turn to discount retailers to stretch their dollars, providing discount stores with some degree of stability in recessionary environments.

Shipping and freight costs

Over the last two years, Dollar Tree’s gross margins were heavily pressured by escalating ocean container shipping (Figure 12) and domestic freight costs. As ocean container shipping costs have receded to near pre-COVID levels and domestic freight costs have moderated, I expect pressure on gross margins to recede. However, as approximately 60% of Dollar Tree’s ocean shipping contracts are still at locked at higher rates through the end of 2023, the full benefit of reduced shipping costs will not be felt till 2024.

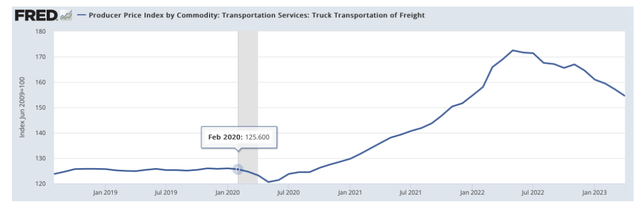

Domestic freight transportation costs have similarly receded from post-COVID highs (Figure 17) but remain about 25% above peak levels and it may take time before it returns on pre-COVID levels.

Figure 17: Truck freight transportation producer price index

FRED, St. Louis Federal Reserve

One-time factors

Markdowns

Markdown costs increased 45 basis points primarily due to: (1) higher promotional and clearance markdowns on the Family Dollar segment, and (2) higher clearance sales at the Dollar Tree segment as it unloaded $1 inventory to move to its $1.25 product offerings.

Unanticipated warehouse expenses

As mentioned above, Dollar Tree’s West Memphis Arkansas distribution center due to the identification of rodent infestation by the US Food & Drug Administration and US Dept of Agriculture inspection. It took a one-time charge in 2022 for the temporary shutdown of the distribution center as well as the recall and disposal of affected products.

My Assessment Of Management’s Value Drivers

In his calls with investors, Richard Dreiling articulated the following key initiatives:

Investments in people and firm culture

Better hires and training should lead to improved execution, customer satisfaction, and efficiency; however, it is difficult for a public shareholder to measure the progress beyond anecdotal evidence gleaned from store visits. On my Wednesday, May 10 mid-afternoon Dollar Tree store visit, I observed long lines at the check-out counters serviced by upbeat and polite checkout staff. However, the store was quite untidy, items were mis-shelved, and empty carton boxes were strewn around the shop floor. I just hope it’s not more of the same in other stores.

Update and modernize its supply chain

As Richard Dreiling observed, “We have a lot of distribution centers that need to be updated and modernized”. It is my hope and expectation that under Mike Kindy’s leadership, the company will use this opportunity to incorporate the some of the state of the art, highly automated robotic technology utilized by Amazon and Walmart into its warehouses. If successfully, the efficiency of both its Family and Dollar Tree segments will leapfrog the competition.

Better information technology systems

Richard Dreiling expressed surprised the IT systems lack a lot of basic things that the operators, merchants need, and supply chain need. He further noted that the company is “simply not where we need to be from a systems perspective to reach our potential”, and that “we have recently begun a comprehensive review of all of our systems and infrastructure to make the right decisions and investments to take Dollar Tree and Family Dollar to the next level.”

I am hopeful that under Bobby Aflatooni’s leadership, the company will take the opportunity to build an IT platform that too will leapfrog the competition and lay the foundation to establish and maintain its lead over the competition for the coming years.

“Investment” in pricing

Management has completed the roll-out of the new $1.25 price point at all Dollar Tree segment stores throughout the country, and it has begun introducing $3 and $5 items in select stores.

At the Family Dollar segment, the company has made “investment in pricing”, i.e., reduced product prices down to a level that is on parity with competitors’ pricing, which contributed to bringing Q4 2022 operating margins to zero. This strategy is not sustainable beyond the short term, proves that Family Dollar still lacks the scale advantages over smaller competitors despite its hefty scale of 8,000 stores, and highlights the need for a fundamental overhaul in its operations.

Mantle Ridge has assembled a top-notch team of well-qualified and experienced discount retail executives at Dollar Tree. The team needs to invest wisely in its people, and it needs to successfully upgrade, modernize, and execute on its supply chain, distribution, information technology, and merchandising capabilities. If successful, the company will pull ahead of its competition and become far more valuable than it is today. If it fails to get all cylinders firing, I believe management should unload or shutdown the Family Dollar stores that deliver no value to focus on the Dollar Tree segment. Otherwise, there is a very real risk that the company hobbles along until it eventually ends up in the graveyard of former retail giants that failed to adapt to the changing times.

Dollar Tree’s investor day, which was originally planned for October 2022 and then Spring 2023, has finally been scheduled for June 21. As current leadership team has been on-board for over a year, it is reasonable to expect a clear articulation of strategy and tangible evidence of value created. While I plan to hold onto most of my shares for the time being, I am prepared to trim my position if the update disappoints.

Concerns

My main concerns are:

- People risk, whether the new leadership team can work well together, and

- Execution risk, whether key members, particularly in merchandising, supply chain, distribution, and technology, can deliver on their key objectives. If not, Dollar Tree’s long-term future could be grim.

In summary

- Dollar Tree has underperformed Dollar General and disappointed investors since it acquired but repeatedly failed to integrate Family Dollar Stores

- Mantle Ridge LP, an activist hedge fund, has installed at Dollar Tree a new, top-notch management team with highly relevant skills and experiences, and appears well-qualified to unlock the company’s full potential

- The management team can create substantial value if it can invest wisely in its people, and successfully upgrades, modernizes, and executes on its supply chain, distribution, information technology, and merchandising functions

- If it does not succeed, there is a non-zero risk that the company hobbles along until it eventually ends up in the graveyard of former retail giants that failed to adapt to the changing times.

- The company has scheduled its next investor day for June 21. I plan to hold onto most of my shares but eagerly look forward to clearly articulated strategies and tangible evidence that things are starting to turn around.

Read the full article here