Since our publication called ‘Heineken Might Benefit From This Difficult Momentum‘ released in November 2022, the company’s stock price appreciation reached a plus 34.73%, this was also supported by Bill & Melinda Gates Foundation’ recent investment that we nicely titled with ‘Bill Loves Beer And Heineken Is Still A Buy‘.

Mare Evidence Lab’s previous analysis

In Q1, Heineken (OTCQX:HEINY) closed its account with a slight decrease in net profit (-3%), to €403 million, while decided to maintain its 2023 targets unchanged. Despite a drop in volumes, group revenues before non-recurring items grew by 8.9% to €6.38 billion. Heineken estimates that operating profit will increase by 5-8% at year-end.

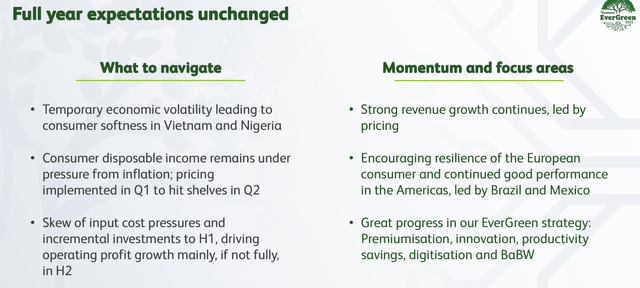

In detail, the 2023 Heineken outlook still aims for stable to modest volume growth, despite incremental negative development in Nigeria and Vietnam. However, this was offset by better-than-expected output in the EU and solid performance in Mexico and Brazil. Heineken country MIX performance might be slightly different than originally forecasted and looking at the GEO area, it is important to provide the following takeaways:

- The Europe region was resilient and pricing is coming ahead. However, price increases have not been fully performed yet. In detail, beer volume decreased organically by 2.3% while price mix was up by 13.6% on a constant geographic basis;

- In Brazil, Heineken brand momentum is still solid and Amstel is nicely growing. The competitive Brazilian environment is strong and the company has been taking significantly higher pricing without compromising volume growth pace. In Brazil, premiumization (one of Mare Evidence Lab’s key investment takeaways) is going well;

- On a negative note, total Nigeria volume was down mid-20s. The local economy was impacted by the lack of local currency and this hurts the clientele’s ability to purchase goods. However, the overall situation is improving and Heineken is focusing on profitability;

- In Vietnam, the economy was heavily impacted by exports and the real estate sector. The company misread clientele demand and overstocked in Q4. Despite that Vietnam sell-out was positive in Q1. The beer industry read the B2C signals in the same way and Heineken’s performances were in line. According to the Vietnamese government, the economy should recover starting in 2023 second half, so we decided to left unchanged our internal assumptions.

The company’s Q1 volume looks transitory and here at the Lab, we still expect a minus 1.5% in Q2. There will be a sequential improvement in markets but we still expect more challenges in Europe. As the European market leader, Heineken was able to anticipate peers on pricing, but we should carefully monitor commodities prices, volume elasticities, and competition maneuvers. Going deeper into our price increase analysis, Heineken implemented further price hikes in Q1 and will see the first benefit in Q2. The currency development is guided to be an €85 million headwind on the core operating profit and Heineken re-iterated its fiscal year outlook.

Heineken 2023 outlook

Our upside

Given marketing expenditure and inflationary cost pressures, net profit growth is now more skewed to H2. 2023 spot input commodities are below-average rates and beers have a strong record of holding within the category. In our last analysis, we emphasized how: “in a period of inflation, consumers are looking for cheaper alternatives within the same categories”.

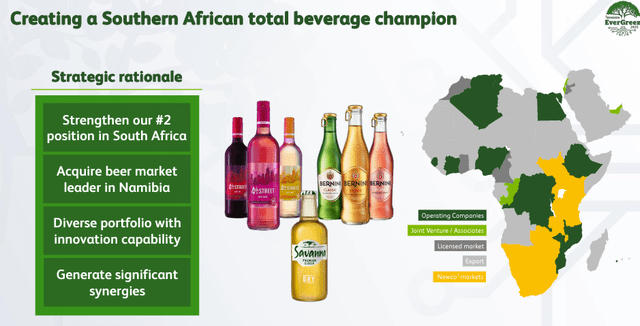

Aside from this, we are confident that Heineken was behind on back-office efficiency implementation. The company operates a 45 ERP system with significant inefficiency in its logistics. These benefits should be realized in a medium-term horizon period, and Heineken will have more operating leverage flexibility going forward. Q1 marketing investments were in line with the revenue trajectory and skewed toward premium brands across the growth key markets. The Distell transaction was completed on the 26th of April and Heineken expected synergies for €75 million which is 2% of the group’s total EBIT profit.

Distell transaction overview

Conclusion and valuation

Last time, we increased our organic growth estimates to 12.5% from 11% with volume growth of 0.5% thanks to a positive price mix evolution of 12%. Excluding the Russian impact, we are above Wall Street forecasted estimates, but we are confident that analysts are not giving Heineken enough credit for its cost-saving initiatives and strong pricing power. These characteristics have made the company a good inflation hedge, with EBIT growth on track to offset raw material inflationary pressure. This is a margin recovery narrative with a two-year forward-looking after a 500 basis point margin headwind in COVID-19 times. Therefore Mare Evidence Lab’s EPS estimates are unchanged. On a valuation side, the company is still trading at an 18x 12-month forward price/earnings with a 15% discount to European staples. In line with our previous valuation, we decided to reiterate a target price of €120 per share ($63 in ADR), maintaining a buy rating. Key risks in our overweight include higher input costs and a deeper-than-expected slowdown in Europe.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here