Article Thesis

Blackstone Inc. (NYSE:BX) is one of the largest alternative asset managers in the world. Despite its compelling long-term outlook, strong market position, and steady AuM growth, the company’s shares are down quite a lot over the last year. I believe this makes BX look attractive as a long-term investment today.

Blackstone’s Leadership Position

Blackstone Inc. is an alternative asset manager, where it competes with companies such as KKR & Co. (KKR), Brookfield Corporation (BN), Apollo Global Management (APO), and so on. Blackstone is one of the largest players in this field, with $990 billion of assets under management at the end of the most recent quarter. On top of that, Blackstone also partially owns some publicly-listed daughter entities, such as Blackstone Secured Lending Fund (BXSL) and Blackstone Mortgage Trust (BXMT).

Blackstone’s well-recognized brand name and its large size should be advantageous in the future. Investors have a tendency to flock to the largest asset managers in a specific space, e.g. going with BlackRock’s (BLK) ETFs instead of those of smaller, less well-known competitors.

In the alternative asset management space, where constructs can be more complicated than the ETFs that BlackRock offers, and where reporting may be more opaque, trust is even more important. I thus believe that Blackstone’s leadership position could be an even larger advantage for the company relative to the size and scale advantages that other (non-alternative) asset managers have as well.

It looks like these (presumed) advantages are working well for Blackstone, as the company continued to raise funds at a hefty pace in the recent past. During the most recent quarterly earnings presentation, the company’s Chairman and CEO Stephen A. Schwarzman said (emphasis by author): “Our successful fundraising initiatives position us with nearly $200B of dry powder capital, an industry record, ahead of what we believe will be an attractive environment for deployment.”

The “attractive environment for deployment” could materialize as financial conditions are tightening – some companies could come under pressure and would then potentially become attractive takeover targets for a deep-pocket player such as Blackstone. Alternatively, BX could acquire assets (e.g., real estate portfolios or single properties) from sellers that are forced to monetize assets to raise cash. In other words, those with financial flexibility and dry powder should be advantaged during times when financial conditions are getting harsher, as weaker players could be forced sellers. That’s also an argument for why Warren Buffett keeps a hefty cash position at Berkshire Hathaway (BRK.A) (BRK.B).

During the first quarter alone, Blackstone attracted inflows of a little more than $40 billion, or more than $160 billion annualized. That’s highly attractive, both in absolute terms and also relative to the company’s current assets under management base. A high relative growth rate bodes well for Blackstone’s fee-based earnings in the long run.

Alternative asset managers have a significant market opportunity in the coming years and beyond, I believe. While the argument for allocating capital to alternative assets has changed to some degree, investors still have good reasons to up their alternative asset allocation. Prior to the inflation we are witnessing right now, interest rates were close to zero – investors that wanted better returns were attracted to alternative assets. While interest rates have risen considerably and are now not close to zero any longer, alternative assets are still attractive. Unlike fixed-income assets such as treasuries, alternative assets promise a better return profile that has a good chance of beating inflation. For those that are buying treasuries right now, that’s less likely, with core CPI inflation still running at a 5.5% rate.

At least some of the assets that are managed by alternative asset managers such as Blackstone, e.g. real estate, the “real asset” nature of these assets has sort of a built-in inflation protection mechanism. Since institutional investors don’t have high alternative asset allocations for now, and since the asset class is both attractive from a return potential perspective and from an inflation protection perspective, it seems likely that the alternative asset management industry will show compelling growth in the long run. With market growth potential and a leadership position for Blackstone, I believe the company has an encouraging long-term growth outlook.

Blackstone: Ups And Downs In Profits

While Blackstone has a compelling long-term outlook and a positive track record, some investors still avoid it due to the fact that Blackstone’s earnings can be opaque – due to the ups and downs in (equity) markets, there can be sizeable ups and downs in Blackstone’s profits. We see this in the company’s most recent quarterly results, for example:

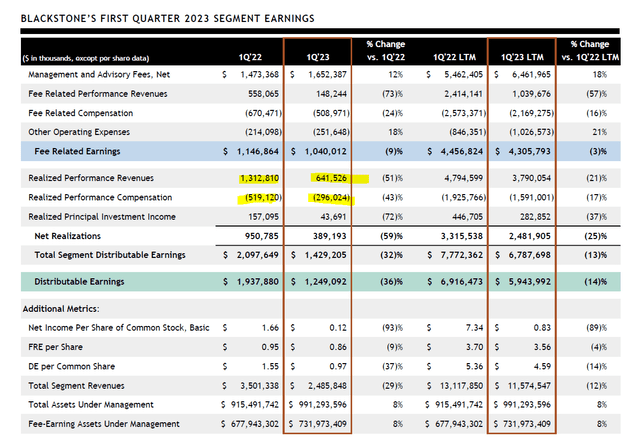

Blackstone presentation

Blackstone’s realized performance revenues and its realized performance compensation are dependent on the performance of the assets the company manages. During times when the broad market is doing well, realized performance revenues and compensation are higher, while they are lower (or even negative) during times when markets aren’t firm. The company has thus seen its realized performance revenues and compensation decline over the last year, as equity markets, debt markets, and also real estate markets were weak. As a result, Blackstone’s distributable earnings took a major hit, dropping by more than one-third between Q1 of 2022 and Q1 of 2023.

This is not the result of underlying problems at Blackstone, however – the company’s assets under management are up, there are no major outflows on a net basis, the brand name has not been tarnished, and so on. Instead, market conditions were very unfavorable, and as a result of that, profitability declined. But as long as markets recover and get stronger eventually, Blackstone’s profits should rise again. Fee-related earnings were down only marginally, as those depend less on the performance of the assets that Blackstone manages – but even there, performance revenues had a negative impact.

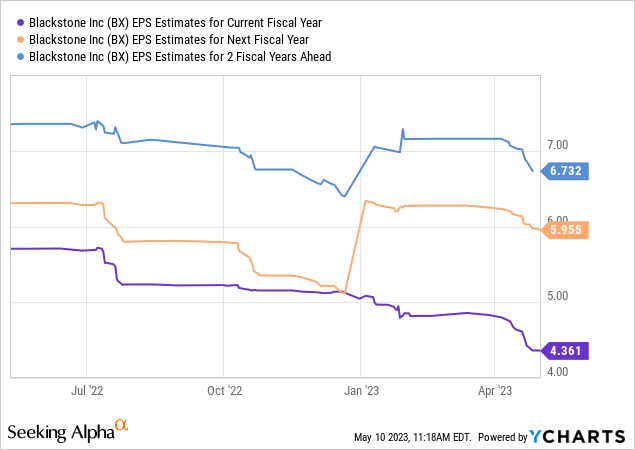

Potentially the least cyclical and most important metric for the long run is Blackstone’s net management and advisory fee. This is largely driven by the company’s assets under management, and since those were up, Blackstone’s net management and advisory fees were up as well, climbing by an attractive 12% year over year. I expect this metric to grow in the coming years as well, as Blackstone’s fundraising remains successful and as inflows remain strong. With performance revenues and compensation most likely recovering at some point, there is a good chance that Blackstone will grow its profits meaningfully in the long run, I believe. Wall Street analysts see things similarly, as they are forecasting a huge profit increase in the coming years:

While Blackstone is expected to earn $4.36 this year, this number is forecasted to rise by 37% next year and by another 13% in 2025, which makes for an overall 54% jump in per-share profits. Blackstone has beaten earnings per share estimates in each of the last 10 quarters, thus there is a clear track record of outperforming expectations. We can also say that there is a clear track record for Wall Street to underestimate Blackstone’s profitability. While history does not necessarily repeat, I believe that the very clear track record of beating expectations suggests that Blackstone will be more profitable in the coming years (and potentially also in 2023) relative to what is forecasted today.

While Blackstone does not look especially cheap based on forecasted profits for 2023, at around 18x net profits, it also does not look very expensive, considering growth tailwinds and its strong market position. When we look at Blackstone’s earnings multiples for 2024 and 2025, we see that the valuation drops to 14x and 12x net profits, respectively. If Blackstone were to beat these estimates, the valuation would be even lower, of course.

Due to the headwinds from lower performance revenues and compensation, Blackstone’s profits are down this year, and that has made the company lower its dividend. Nevertheless, the dividend yield is still pretty solid, at 4.0% – that’s more than twice the broad market’s dividend yield. With earnings most likely recovering in 2024 and beyond, the dividend will likely rise as well, and those that buy today could be looking at a pretty nice dividend yield on cost not too far from now.

Takeaway

Blackstone is one of the largest alternative asset managers and should thus be able to capitalize on the growth in this industry. AuM is growing nicely, which drives BX’s management and advisory fees. While lower performance revenues have overshadowed that in the near term, I believe that there is a good chance that BX will get back to growth next year and beyond.

The valuation is not demanding, and the dividend yield is nice despite the recent reduction. Overall, I believe that Blackstone is looking good for a long-term-oriented investor at current prices.

Read the full article here