Recent news has provided several reasons for investors to become jittery. From inflation that’s higher than it’s been in decades to bank failures to fears of stagflation, there is plenty to concern people. Some pundits view a recession as a foregone conclusion.

However, just because there is reason for concern in the short term, it’s still important to invest now for the long term. Indeed, missing out on just the best 50 days over the past 30 years when investing in the S&P 500 (VOO) would have led to a negative annual return. Just sticking with the S&P for the whole 30 years would have led to an average annual return that’s nearly 10%.

Investing in individual stocks is a different game than investing in a broader index, but sticking with a solid, profitable company is a good idea because missing out on just a few big up days or weeks can really hamper overall returns.

Recession Resistance

As noted in the first sentence above, economic concerns abound. The next recession is always closer than it was yesterday, but just because some companies will perform poorly or go belly-up during a recession does not mean that all companies will. That’s why it’s a good idea to maintain an investment in some companies that can keep up their business in all economic decisions.

When it comes to recession-resistant companies, few are going to exceed the necessity of waste removal. Sure, there are companies that produce consumer staples or utilities like water or electricity that will be more important than waste removal services, but few other businesses will exceed the business that a garbage disposal company can maintain during all economic conditions.

There are state and federal regulations that require homeowners and businesses to properly dispose of solid and hazardous waste. Few municipalities will allow you to keep piling up garbage in your home or yard before taking steps to force you to do so. The old A&E show “Hoarders” provides a case in point.

Therefore, regardless of whether the economy is up or down, it’s imperative for most homeowners (or landlords) to contract with a waste disposal company. This is where Waste Management, Inc. (NYSE:WM) comes into play.

Waste Management Financials

Waste Management is “North America’s leading provider of environmental solutions,” serving “to manage and reduce waste at each stage from collection to disposal.” The company works through locally managed subsidiaries to remove waste and recover useful resources, some of which can provide renewable and clean energy.

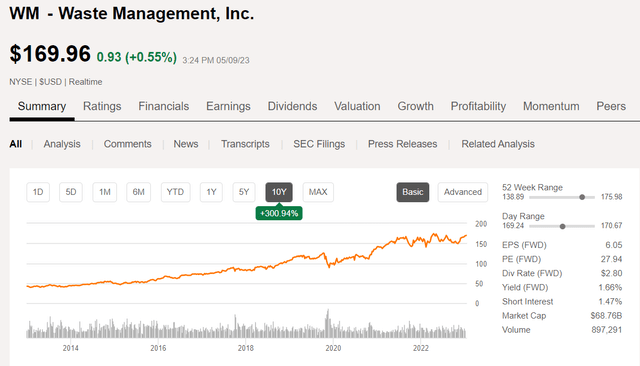

The past 10 years have seen a massive increase in the price of Waste Management shares. The price of one share today is nearly four times what it was as recently as 2013.

Waste Management 10-year share price (Seeking Alpha)

The company is currently near its 10-year high. Over that same period, revenues have grown about $6 billion, or about 30% over a $13.983 billion base in December 2013. Net income has grown by a little more than $1.4 billion over the same period, from $2.055 billion in 2013 to $3.468 billion in December 2022. That is a 69% increase in net income, which is not shabby, although it’s not earth-shattering. When looking at this from an EPS standpoint, the earnings per share has basically doubled since 2014 ($0.21 in 2013 appears to be an anomaly), going from $2.79 to $5.39.

Volumes in the last quarterly report showed a growth of 1.2% on a year-over-year basis. Both revenue and net income were up over the previous year. Free cash flow was down, resulting from higher capital expenditures, which included vehicle deliveries that hit during the quarter. However, these are frequently periodic expenditures that will not hit every quarter equally.

Effectively, all things being equal, one might expect WM’s share price to perhaps double in price over the past decade, not quadruple. This has led to a current PE ratio of about 30. This is well above its more common PE that has run in the mid-teens to low twenties (with the exception of 2013, which, as noted above, was an anomaly). The increase in the PE ratio for Waste Management coincides with the rapid increase in share prices that hit around 2021, and it likely indicates that additional rapid price growth in the near term is not terribly likely.

The EPS number has been shored up by a reduction of nearly 12% of Waste Management’s shares on the market over the past 10 years. Fewer shares means that earnings are spread to a smaller number of owners and dividends are paid on fewer shares. While this is a decent buyback in terms of size, it is not as impressive some companies like Apple (AAPL), which has bought back nearly 40% of its shares over the same period.

WM’s long-term debt has grown by a little more than 50% over the past 10 years, from $9.5 billion to $14.33 billion. As interest rates rise, this could provide headwinds for future growth, as well. Again, the numbers might indicate a doubling of WM’s stock price over the past decade, not a quadrupling.

WM’s Dividend

As an investor who’s interested in income, I always investigate how a company’s income and balance sheets interact with its dividend.

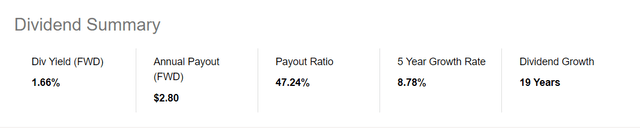

Waste Management currently pays out $2.80 per year in dividends with its latest raise, which was $0.05 per share or roughly 7.7% over its previous dividend payment. This is fairly close to its five-year dividend growth average of 8.78%. The current yield is 1.66%, which is very similar to the current yield of the S&P 500, and the dividend payout ratio is 47.24%. The 19-year record of growing the dividend is solid, and it appears that there is no real risk of a cut in the near term.

Waste Management Dividend Info (Seeking Alpha)

With a dividend growth average of between 8% and 9% over the long haul, investors could expect the dividend to double every eight or nine years. However, those looking for a yield that beats the broader market would do well to look elsewhere.

Conclusion

If I currently held WM stock, I would continue to hold it. However, I am very unlikely to start a position. The company has a solid record of strong financials, along with moderate growth over the past decade. The dividend has shown strong growth over the same period, although the most recent increase was a bit lower than the five-year average. The current payout ratio would make the dividend appear quite sustainable, while also allowing for some growth as long as the net income continues to grow. That said, the current dividend yield is below what I would like to see without accompanying double-digit annual dividend growth.

Waste Management is a necessary company for many people by the very nature of its business model. As such, the company should have the ability to pass cost increases on to its customers, which should provide steady revenue growth, provided it can maintain its customer base. However, WM stock has gotten progressively pricey over the past couple of years. The price is not attractive at a PE of 30, and this relatively high price is likely to hamper share price growth in the near term.

Read the full article here