Investment thesis

Kennametal (NYSE:KMT) is currently facing a series of headwinds that are impacting its operations, including inflationary pressures, higher labor costs, supply chain issues, negative foreign exchange impacts, and lingering effects of COVID disruptions in China. In recent years, the company has not been able to grow, but rather its sales have been reduced as a result of divestments and lack of growth opportunities and M&A initiatives. For this reason, investors are currently only benefiting from the dividend and share repurchases, whereby expectations of low growth and potentially lower margins have caused investor annoyance.

Even so, I consider that Kennametal is a company that is worthwhile owning at current prices due to the following factors that I will explain throughout this article: the company has been successfully operating for many years and delivering ever-growing dividends (although they have grown at very conservative rates), its profit margins are quite high, the current P/S ratio is below the average of the past decade, its debt levels are very manageable, and it has a strong cyclical component, so high capital gains can be obtained by selling when optimism arises again as current headwinds fade.

A brief overview of the company

Kennametal is a global provider of tungsten carbides, ceramics, super-hard materials, and solutions used in metal cutting and extreme wear applications to keep customers up and running longer against conditions such as corrosion and high temperatures. The company operates for key industries, including aerospace, earthworks, energy, general engineering, and transportation end markets. It was founded in 1938 and its market cap currently stands at ~$2.16 billion, employing over 8,000 workers.

Kennametal operates under two main segments: Metal Cutting and Infrastructure. Under the Metal Cutting segment, which provided 61% of the company’s total sales in fiscal 2022, the company develops and manufactures high-performance tooling and metal-cutting products and services, including “milling, hole making, turning, threading and toolmaking systems used in the manufacture of airframes, aero engines, trucks and automobiles, ships, and various types of industrial equipment”. And under the Infrastructure segment, which provided 39% of the company’s total sales in fiscal 2022, the company “produces engineered tungsten carbide and ceramic components, earth-cutting tools, and advanced metallurgical powders, primarily for the energy, earthworks, and general engineering end markets”.

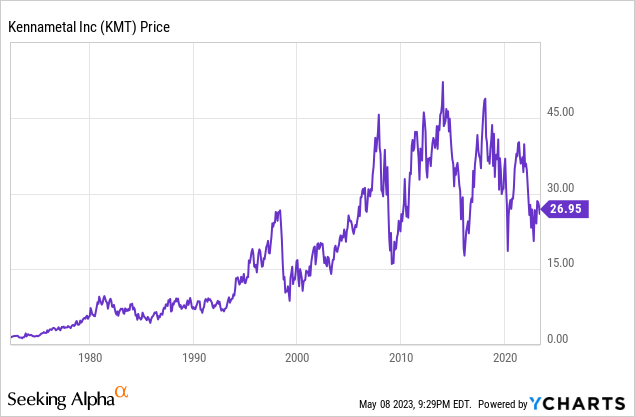

Currently, shares are trading at $26.95, which represents a 48.69% decline from all-time highs of $52.52 in January 2018. This decline has been caused by current macroeconomic headwinds as the company’s operations have historically been subject to high volatility, which opens up great opportunities for profiting from higher dividend (and buyback) yields on cost or potential capital gains once current headwinds fade.

Sales are slowly recovering boosted by price increases

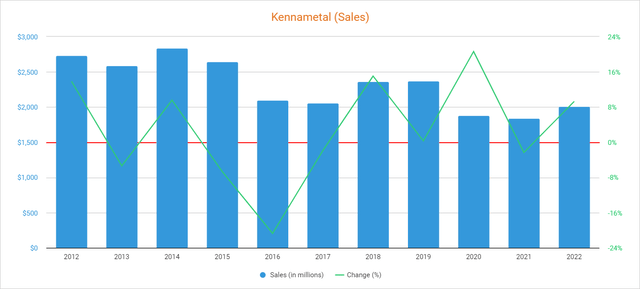

The last 10 years have been a period that invites pessimism since sales have diminished over the years. The biggest decline took place in fiscal 2016 as the company divested some non-core businesses, and after some recovery, they significantly declined again as a consequence of impacts related to the coronavirus pandemic crisis. In this regard, sales declined by 20.63% in fiscal 2020, and by a further 2.33% in fiscal 2021, but partially recovered in fiscal 2022 as they increased by 9.29%. Using 2022 as a reference, 39.64% of the company’s sales are generated within the United States, whereas the rest is generated internationally, with a strong presence in Germany, China, and India.

Kennametal Sales (10-K filings)

As for fiscal 2023, sales increased by 2.33% year over year during the first quarter, 2.15% during the second quarter, and 4.64% during the third quarter as the company is raising the price of its products in order to offset inflation. In this regard, fiscal 2023 is expected to close with a 3.98% increase in sales (1% to 2% volume increase, around 7% of price realization, and a negative impact of $100 million due to foreign exchange headwinds), and sales are expected to grow by a further 3.35% in 2024, which are actually pessimistic figures considering current high inflation rates (and thus ongoing price raises). Furthermore, foreign exchange rates negatively impacted sales by 4% during the third quarter of fiscal 2023, and although this headwind is expected to partially fade in the fourth quarter of fiscal 2023, it will likely remain for a few more quarters.

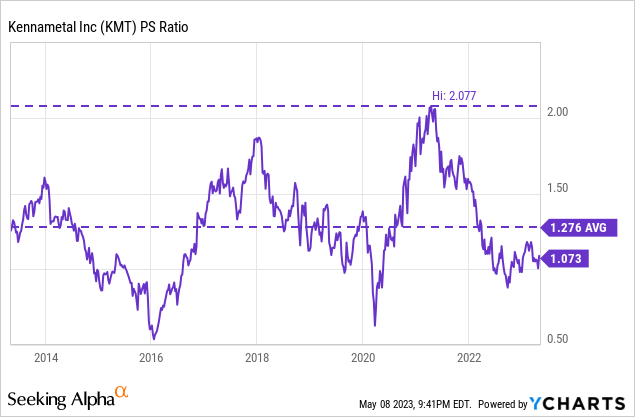

The recent surge in sales, coupled with a sharp decline in the share price, has caused a steep decline in the P/S ratio to 1.073, which means the company currently generates sales of $0.93 for each dollar held in shares by investors, annually.

This ratio is 15.91% lower than the average of the past decade and represents a 48.34% decline from decade-highs of 2.077, which shows significant pessimism among investors as the company’s margins are slightly contracted due to current headwinds while growth expectations are rather low amidst a potential recession. Still, EBITDA margins are showing strong signs of recovery.

EBITDA margins are showing strong signs of recovery

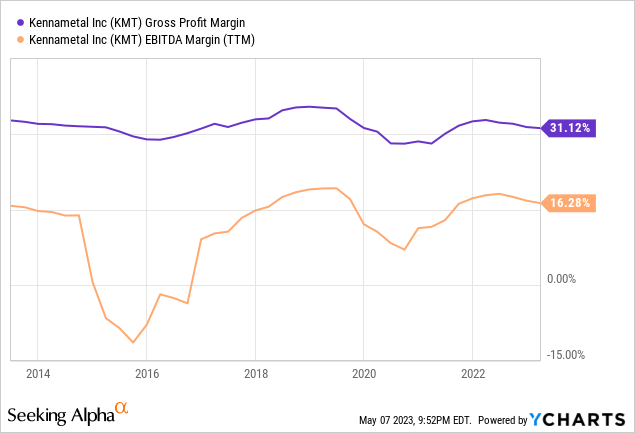

In July 2019, the company initiated a restructuring plan for simplifying its operating structure by closing two manufacturing plants and a distribution center after announcing the sale of several non-core businesses in 2015 in order to focus on long-term growth. So far, profit margins remain very healthy, which suggests the restructuring plan was somewhat successful, but sales suffered as a consequence of divestments. In June 2020, the management announced the acceleration of its structural cost reduction plans, which included a restructuring of around 10% of salaried employees, manufacturing equipment and process modernization, as well as temporary cost reductions due to the coronavirus pandemic crisis. In this regard, the trailing twelve months’ gross profit and EBITDA margins remain at very healthy levels of 31.12% and 16.28%, respectively.

Although the gross profit margin improved to 31.33% during the third quarter of 2023, the EBITDA margin, although high at 15.94%, remains at levels lower than trailing twelve months’ margins as the company’s operations are currently enduring inflationary pressures, supply chain headwinds, higher labor costs, and lingering effects of COVID disruptions in China. In this regard, the company is currently raising the price of its products to offset high inflation rates. Still, I strongly believe that these headwinds are temporary due to their direct link to the current macroeconomic context. Furthermore, supply chain issues have significantly improved in the past few months, but a potential recession due to recent raises in interest expenses to offset high inflation rates could cause a strong impact on demand, which would likely cause a decline in volumes and thus in profit margins due to unabsorbed labor. Luckily, the company has a lot of margin to maneuver thanks to a very robust balance sheet.

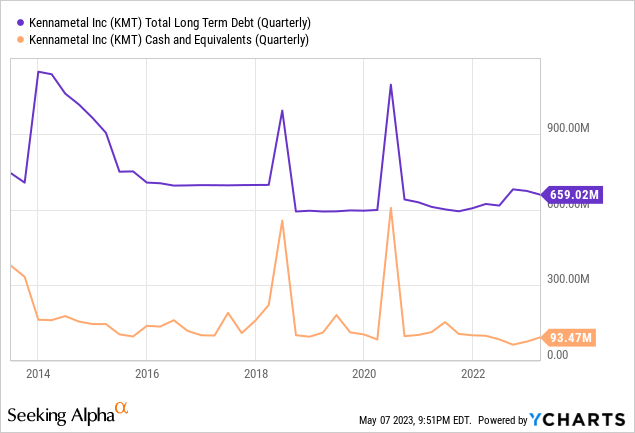

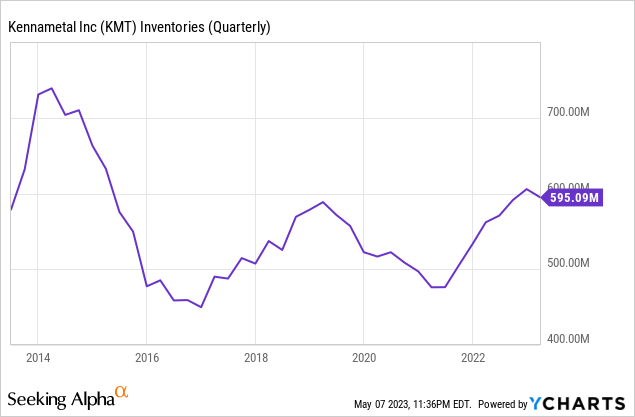

Debt is very manageable as the company recently raised inventories

The company’s long-term debt has remained fairly stable over the past few years and currently stands at $659.02 million, which is significantly higher than cash and equivalents of $93.47 million.

Still, the company’s long-term debt does not pose a significant risk thanks to high inventories of $595 million as the company has recently raised inventories and the price of its products.

These inventories will be essential to reduce current debt levels or, failing that, invest cash into acquisitions in order to grow the business and thus make the current debt load less significant in comparison to the company’s size. Still, the company could struggle to partially empty its inventories as demand could weaken in the event of a potential recession. But despite this, a low dividend (and interest) cash payout ratio greatly reduces the risk of balance sheet deterioration even if headwinds intensify.

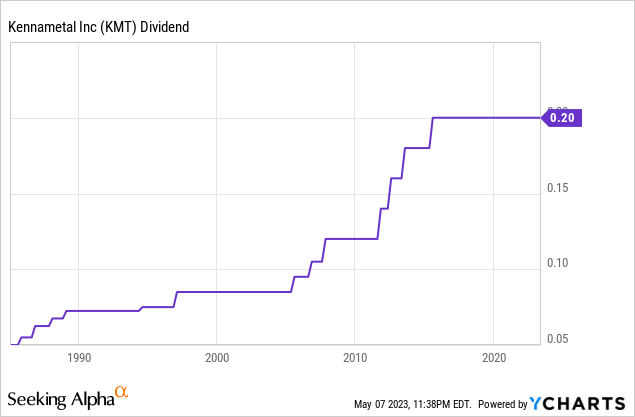

The dividend is safe as the cash payout ratio is low

The company has a long tradition of increasing its dividend whenever operations allow, although these have remained frozen at $0.20 per share since July 2015 when the company announced the last raise of 11.1%. Indeed, dividend growth has been very weak as can be seen in the chart below.

Still, the recent share price decline has caused a spike in the dividend yield to 2.97%, which is, in my opinion, generous as the management has historically allocated a relatively small fraction of cash from operations for the dividend payout. In the table below, I have calculated which percentage of the cash from operations has been used to cover both dividend and interest expenses since 2014.

| Year | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Cash from operations (in millions) | $271.87 | $351.44 | $219.32 | $195.34 | $277.30 | $300.52 | $223.74 | $235.68 | $181.44 |

| Dividends paid (in millions) | $56.44 | $56.98 | $63.72 | $64.13 | $65.10 | $65.75 | $66.30 | $66.74 | $66.57 |

| Interest expenses (in millions) | $32.45 | $31.47 | $27.75 | $28.84 | $30.08 | $32.99 | $35.15 | $46.38 | $25.91 |

| Cash payout ratio | 32.69% | 26.02% | 41.71% | 47.59% | 34.33% | 32.86% | 45.35% | 47.99% | 50.97% |

As one can see, the company has historically used less than 50% of the cash from operations for dividend payments and interest expenses. During the past quarter, the company reported high cash from operations of $73.7 million, and although inventories decreased by $9.98 million quarter over quarter, accounts receivable increased by $22.9 million and accounts payable declined by $9.5 million, which reflects high profitability. Despite this, capital expenditures for the full fiscal 2023 are expected to stand at around $100 million, which can be covered with cash from operations after covering the dividend and interest expenses, and the company’s capex declined to $18 million during the third quarter of fiscal 2023 (from $22 million during the same quarter of fiscal 2022). In this regard, the company is capital-intensive, which significantly limits opportunities to invest cash for growth initiatives, making the stock worth considering, in my opinion, only at unusually low prices like the current ones. Still, the company managed to perform buybacks since 2021, which will eventually improve per-share metrics as the holdings of investors are poised to keep increasing passively by just holding the company’s shares.

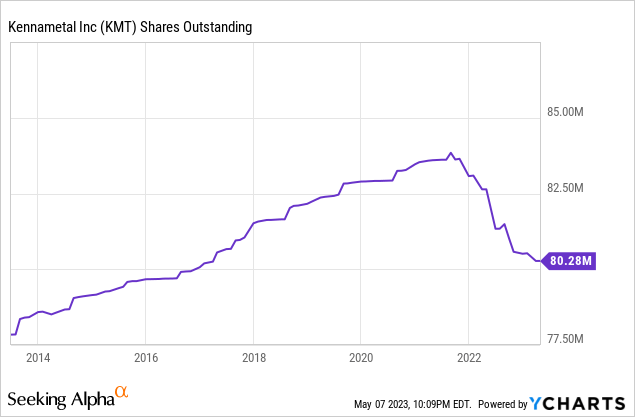

Share buybacks are reverting past share dilution

Until 2021, the number of outstanding shares increased steadily as can be seen in the chart below, but in August 2021, the management announced a share repurchase program of up to $200 million over a period of three years in order to undo past share dilution, and $123 million (or around 5% of the total number of shares outstanding) has been already bought back since the announcement. During the past quarter, $7 million worth of shares were bought back, which means share buybacks remain in force despite current headwinds and risks.

The question that now remains is whether once the current share buyback program ends, another will be announced so that share buybacks represent a way to return cash to investors sustained over time. In this sense, it will largely depend on whether a recession finally materializes in the medium term and whether operations remain as profitable as now in the long run. For buybacks to keep on, not only must margins be maintained at current levels, but investments in machinery and process modernization should allow CapEX to remain below $100 million per year. Furthermore, the management should use cash from inventories to deleverage the balance sheet (and thus reduce interest expenses) or make a significant acquisition to allow for more cash from operations in the long term.

Risks worth mentioning

Personally, I think that Kennametal presents a very low-risk profile thanks to its high-profit margins and a long-term debt slightly higher than its large inventories, but still, there are certain risks that I would like to highlight for the short and medium term.

- Sales growth expected for 2024 is very low considering that the company continues to increase the price of its products. In this sense, the materialization of a recession could result in a significant drop in the company’s sales, which would drag down profit margins as a result of declining volumes and an unabsorbed workforce.

- If high inflation rates continue to impact the company’s operations, margins could fall below current levels if the company fails to offset increased production costs with further pricing actions, which would put the current dividend and share buyback program at risk.

- High capital expenditures could limit future dividend growth despite low cash payout ratios.

- If demand remains weak, the company could have trouble emptying its inventories successfully as it would lead to unabsorbed labor, and thus declining profit margins.

- Although the share price has fallen significantly, the company’s operations are cyclical in nature, so further share price declines could happen in the short and medium term. This risk can only be cushioned by averaging down from current share prices.

Conclusion

The recent share price decline reflects a lot of pessimism among shareholders, but the company’s outlook is not that bad and it seems that what is keeping investors on the sidelines is more related to (likely temporarily) weak demand as a result of declining consumer’s purchasing power due to inflation and a potential recession as a consequence of the recent interest rate hikes aimed at reducing high inflation rates.

Even so, the company’s operations remain robust, as well as its balance sheet as inventories are very high, so I believe that the recent share price decline represents a great opportunity for long-term dividend investors interested in a high dividend yield (and buyback) yield on cost or in high capital gains once current and potential headwinds fade and optimism reigns again among investors. Still, high volatility due to the company’s cyclical nature suggests that averaging down from current share prices could be a wise strategy.

Read the full article here